We have always favored small cap and value stocks in our portfolios, overweighting these asset classes compared to the market. In my article earlier this month, I introduced "profitability" as another stock market segment that we should start emphasizing.

More specifically, this means adding a mutual fund or ETF (exchange-traded fund) that targets stocks of the companies with the highest overall profitability for our "core" large-cap asset class, the US High Profitability strategy. In some cases, this fund would replace a similar holding without as much emphasis on profitability; in other cases, it would make up for a portfolio’s lack of meaningful exposure to higher-profitability companies.

You'll remember that I had three reasons for the update.

First, we've known for some time that higher profitability stocks have higher expected returns compared to the stock market and lower profitability stocks (similar in magnitude to value stocks compared to the market or growth stocks)—and to state the obvious, higher potential returns may help you achieve more of your financial goals.

Second, higher-profitability stocks are fundamentally different from value stocks (and small stocks), and a large-cap high-profitability allocation is also a very good complement to a portfolio that already emphasizes smaller and lower-priced value stocks—a smoother ride in your portfolio reduces financial anxiety and makes it easier to stay the course.

Finally, our investment options have evolved sufficiently to where it makes sense and is economical for us to adjust our allocations—theory is great, but if we don't have a practical way to benefit, it's irrelevant.

In short, adding a high profitability allocation is about higher expected returns and better diversification, and is now sensible to do.

I also explained that the profitability upgrade isn't a paradigm shift in our investing process. It builds on what we've been doing all along. It's an evolution. First, there was broad market indexing. Then, the "asset class” breakthrough helped us target smaller and cheaper stocks. Adding high profitability to a small cap and value-tilted portfolio is the next step forward, a modern refinement to how we own large cap stocks and resulting in a more balanced asset class allocation with slightly higher expected returns.

What does this evolution look like compared to past upgrades?

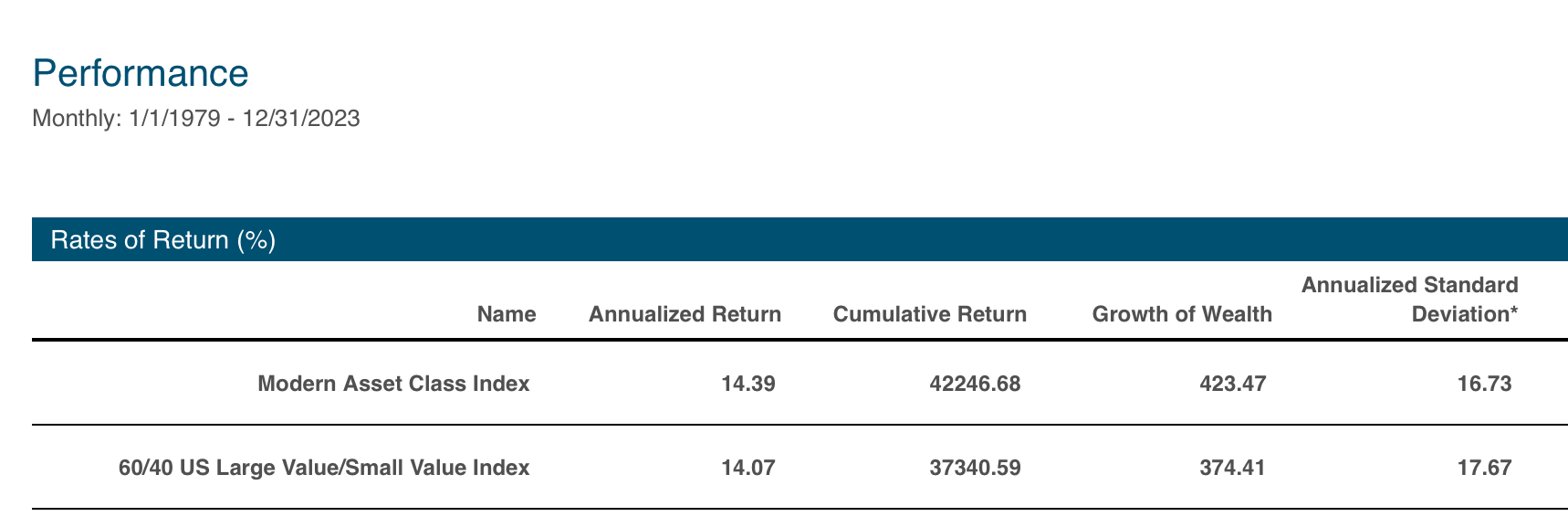

Let's roll up our sleeves and review some historical data starting in 1979 (the inception of Russell Indexes) through 2023, comparing different approaches to our new "US Modern Asset Class Index"—a blend of 30% Dimensional US Large Cap High Profitability, 30% Dimensional US Large Value, and 40% Dimensional US Small Value Indexes (I'm ignoring international stocks in this article).

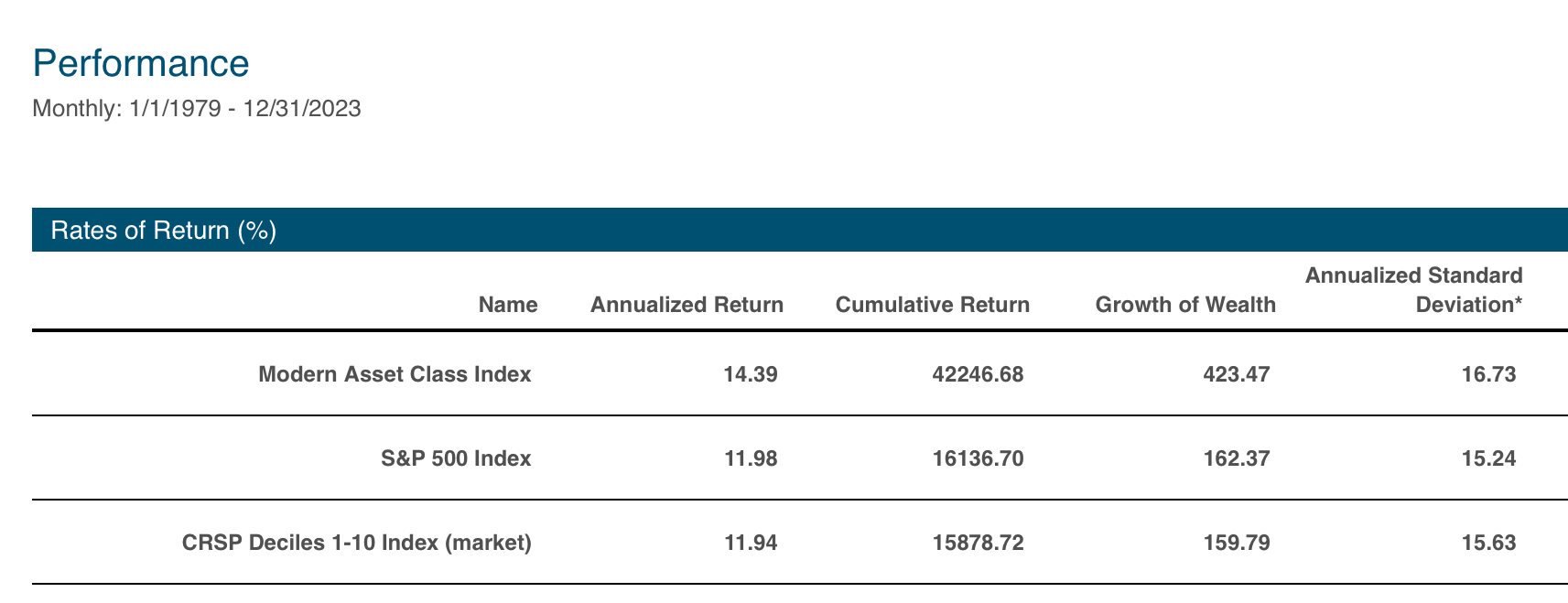

Compared to Traditional Indexing

It's hard to believe that anyone still owns traditional index funds, but they do. In fact, the largest investment funds in the world are S&P 500 Index and Vanguard "Total Market" Index products. The reason is simple—these require no thought; they're "one-decision" investments. Low cost and easy appeals to a lot of people. It’s herd behavior. Unfortunately, this comes at a price in terms of expected returns.

From 1979-2023, the S&P 500 Index gained +12.0% per year, the CRSP 1-10 Index (the index Vanguard uses for their US Total Stock Index fund and ETF) +11.9%. These are very good returns but are well below the +14.4% return for the "Modern Asset Class Index." 2.4% to 2.5% per year below, to be exact.

To put in perspective how big a difference this is, virtually the entire investing world has given up on traditional, stock-picking active management because studies show that active managers underperform market indexes by around 1% per year. The spread between indexing and the modern asset class index has been more than twice as large!

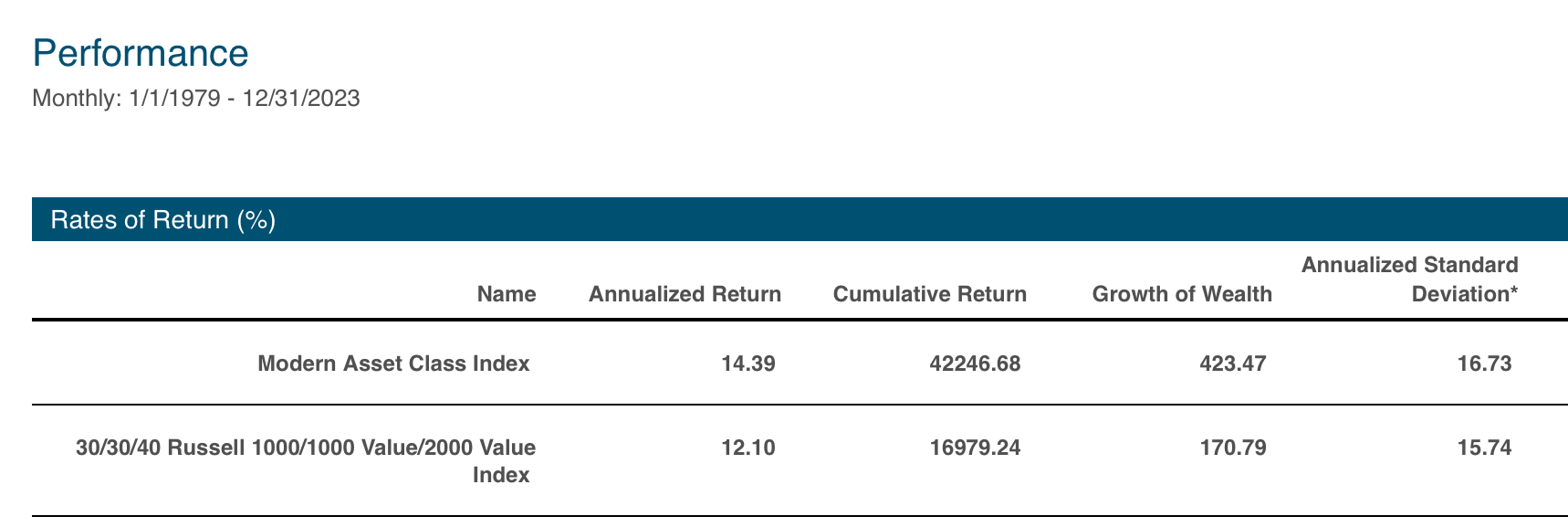

Compared to Style Indexing

Large-cap and broad-market indexes aren't the only index funds available. Many investors stick with traditional indexing but overweight smaller and cheaper value stocks using the index funds from Vanguard or the ETFs from iShares and State Street. Their goal is to maintain the low costs of traditional indexing but capture the higher expected returns from small-cap and value stocks. It hasn't worked out that way.

Index funds are inferior investment vehicles. The design of the portfolios to capture the small-cap, value, or even profitability or "quality" parts of the market is not ideal. The holdings are only updated once or a few times a year, so the portfolios become stale and out of touch with their mandates very quickly. These products are cheap for a reason—they're not good.

The result has been returns no better than buying basic index funds like the S&P 500. Over this period, a 30% Russell 1000, 30% Russell 1000 Value, and 40% Russell 2000 Value Index allocation returned only +12.1%—the same as the S&P 500 and well below the Modern Asset Class Index.

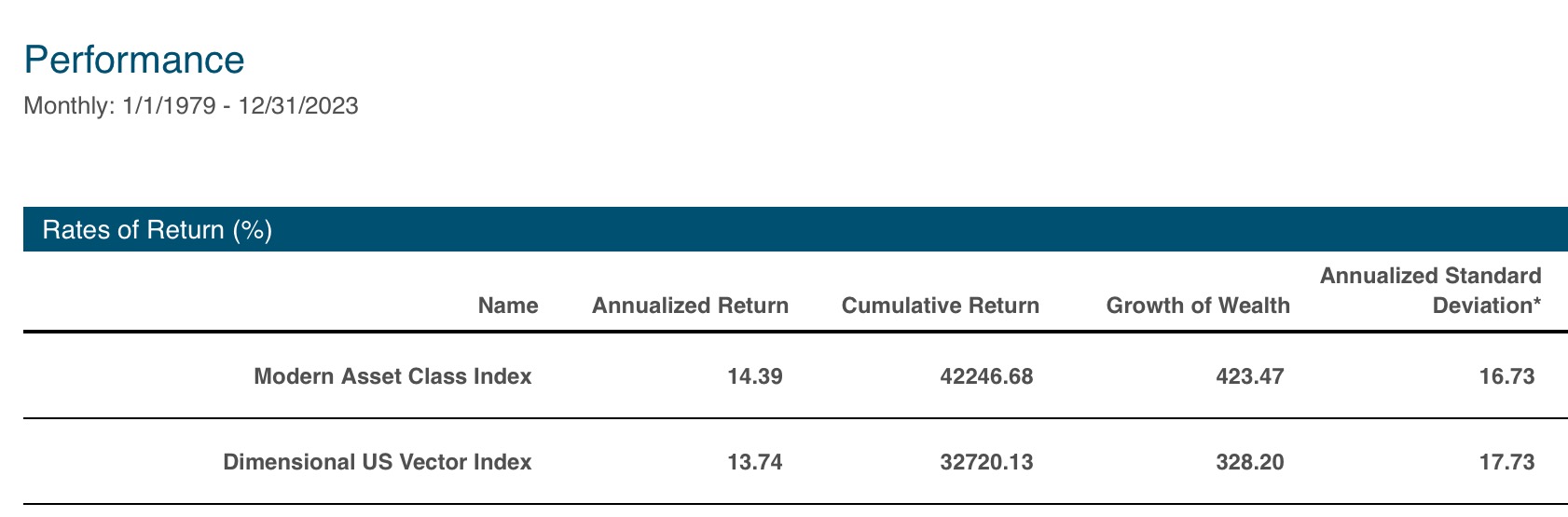

Compared to Vector

Many Servo clients have held Dimensional "Vector" funds (US, International, etc.) for years to target smaller, lower-priced value stocks across the market in a simple, single-fund structure. They've served us well.

My concern with the Vector funds is that they don't have the latitude to dive as far into the higher profitability side of the market as I would like; their small cap and value emphasis prohibit them from owning enough of the larger, more profitable companies for my taste.

The difference between the US Vector Index and the Modern Asset Class Index is smaller than our prior two examples, but it's still noticeable.The Vector Index returned +13.7% per year, 0.7% annually less than the Modern Asset Class Index, and had a bit more volatility (standard deviation).

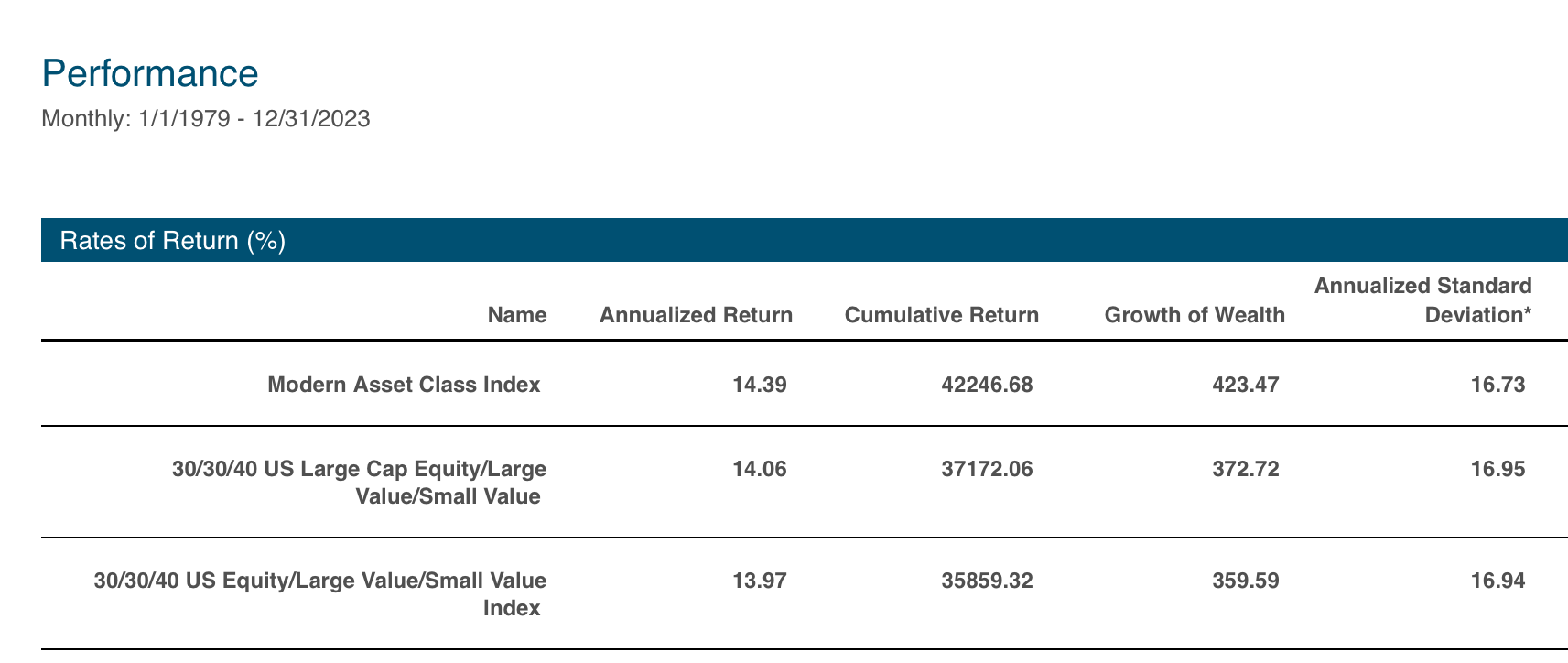

Compared to Our Prior Asset Class Indexes

For most clients, owning large and small value stocks has only made sense as a compliment to a core, large-cap fund we're all familiar with as investors. Years ago, I used the S&P 500 Index or a Total Market Index as this core holding, at 30% of the US allocation, with US large and small value at 30% and 40%, respectively. A decade ago, we swapped the S&P 500 for Dimensional's US Large Cap Equity strategy, which had a slight overweight to higher profitability and lower-priced value stocks. In taxable accounts, we stuck with the US Equity ETF, formerly the Tax-Managed US Equity fund.

These are great funds and have performed well, but replacing them with the High Profitability strategy should increase our expected returns while improving diversification because the profitability fund tends to hold stocks that typically don't show up in our value funds.

We can see the modest improvements in the data. The index allocation with 30% in the Large Cap Equity Index returned +14.1% per year, the version with 30% in the US Equity Index returned +14.0% per year (both similar to the US Vector Index); 0.3% to 0.4% per year less than the Modern Asset Class Index and still with comparable risk.

Compared to All-Value Allocations

Until recently, if you asked me what the best performing stock allocation was expected to be, I would have answered a 100% value stock allocation. To retain some measure of balance, I might have said 60% large (value) and 40% small (value). Not any more.

Splitting the large cap allocation between large value and high profitability stocks is likely to be better, and also much easier to hold during periods where value isn't working (more on this below). Over the 1979-2023 period, the Modern Asset Class Index returned 0.3% per year more than an all-value version and was less risky and less extreme. Going back to the Dimensional US Large Cap High Profitability inception in 1975, it still has the high profitability version ahead by 0.2% per year despite very strong years for value from 1975-1978.

Moreover, during some bear markets (2007-2009, 2011, 2018, 2020), value stocks declined much more than the market. During these same periods, high-profitability stocks declined far less than the market, leading to noticeably fewer portfolio losses. In the bear markets where value outperformed (2000-2002, 2022), high profitability didn't lose any more than the market. Even if you were buying stocks on the day of a crash, you’d probably be better off with the Modern Asset Class allocation.

What's Outperforming?

From a returns standpoint, especially after adjusting for risk, the case is clear for moving to a portfolio that targets US large high-profitability stocks, along with our US and international large and small-value stock asset classes.

In terms of understanding what you own, I also give the Modern Asset Class allocation the edge, as it holds both great companies with reasonable stock prices (high profitability) and good companies that have great prices (large and small value). Who doesn't think this makes sense?

But to me, and I think to you as well, the most significant benefit to profitability should be the psychological one. Something in the portfolio with higher expected long-term returns (like value and small-cap), but that could work in the short run when value and small-cap stocks are not. According to “Modern Portfolio Theory,” we shouldn’t look at the components of a portfolio—it’s the cake that matters, not the individual ingredients. But you and I both know that’s not how we think. We notice the components too, and having greater balance between them can be beneficial and may give us greater peace of mind.

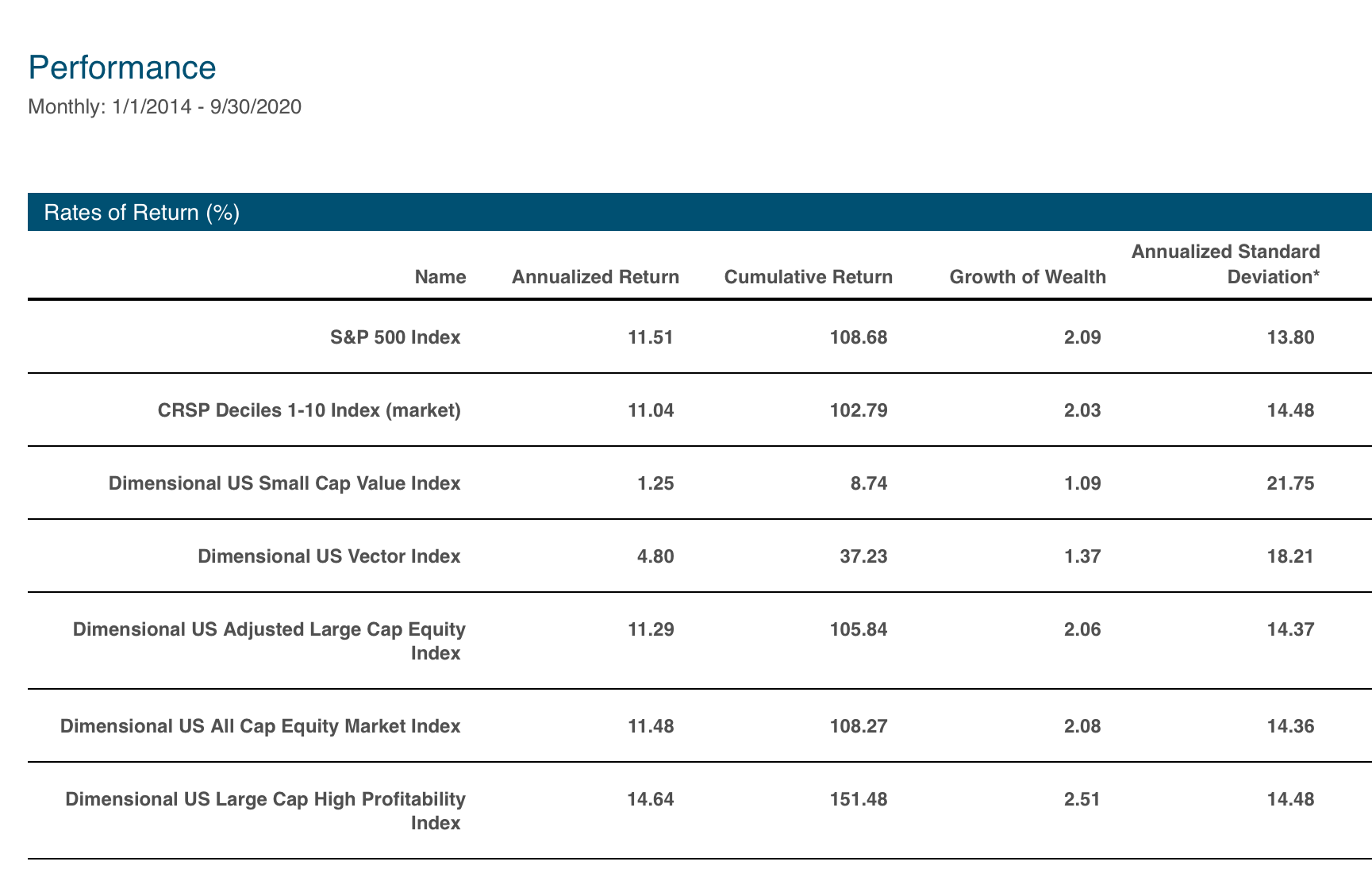

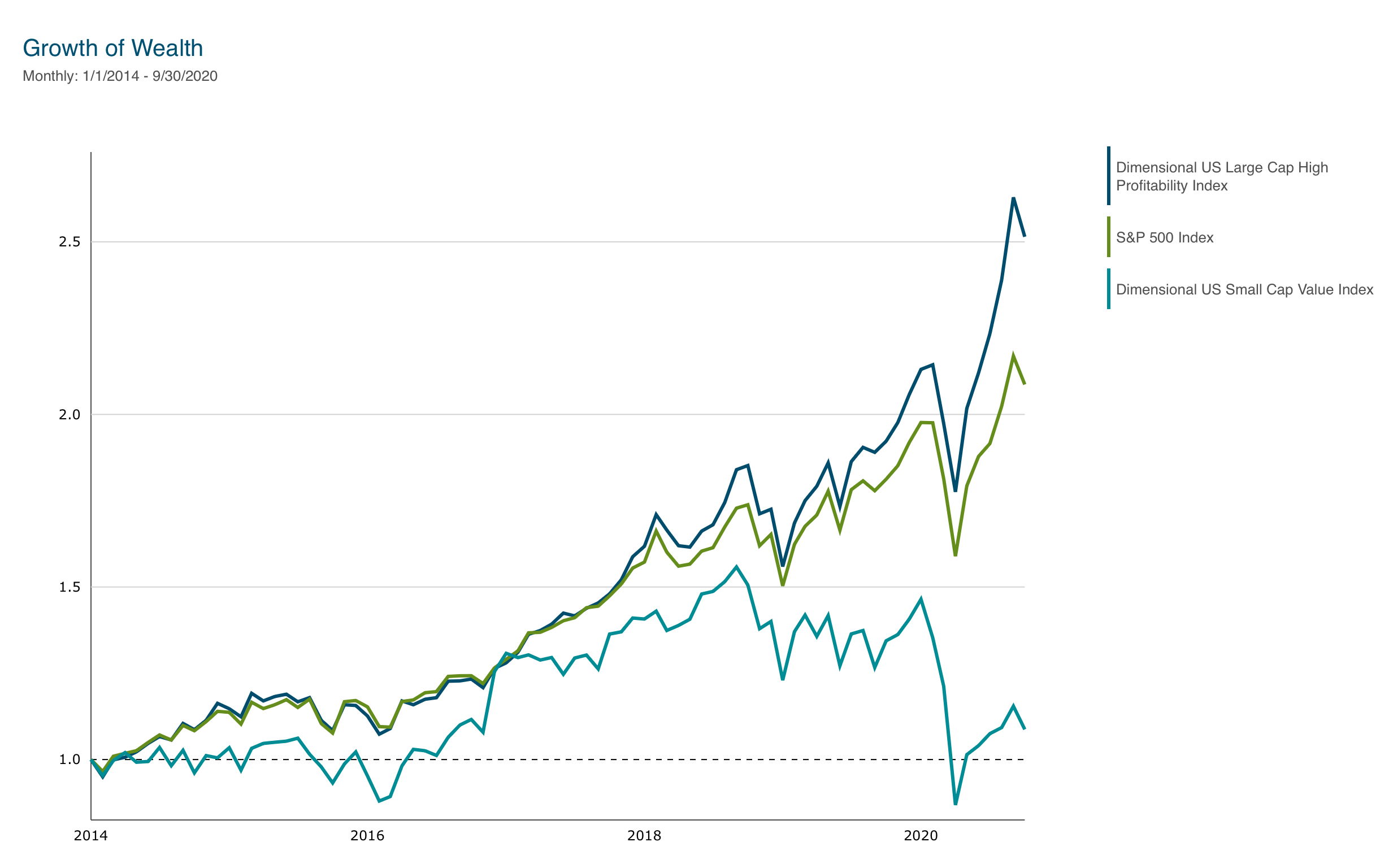

From 2014 through September 2020, small-value stocks had among their worst historical returns relative to the market. While the US market returned +11% and the S&P 500 Index gained +11.5 %, the Dimensional US Small Value Index returned just 1.3% yearly. In the 2018 and 2020 bear markets, small value also lost a lot more than the market. Adding profitability didn't result in a portfolio outperforming the market, but it helped.

Over this same period, having all your stocks in the US Vector Index meant a +4.8% per year return, better than the US Small Value Index but still way behind the market.

Having the US Large Cap Equity Index or US Equity Market Index as your "core" meant that some part of your allocation matched the market, but nothing did better.

Using the US Large Cap High Profitability Index as your core, on the other hand, you earned a +14.6% per year return, 3.1% to 3.6% higher annual returns than the S&P 500 Index and the US market, offsetting some of the significant value stock underperformance. Could some part of your portfolio still outperforming have made it easier for you psychologically to trust that eventually everything else would follow, and that your asset class approach hadn't become a permanent loser? It could not have hurt.

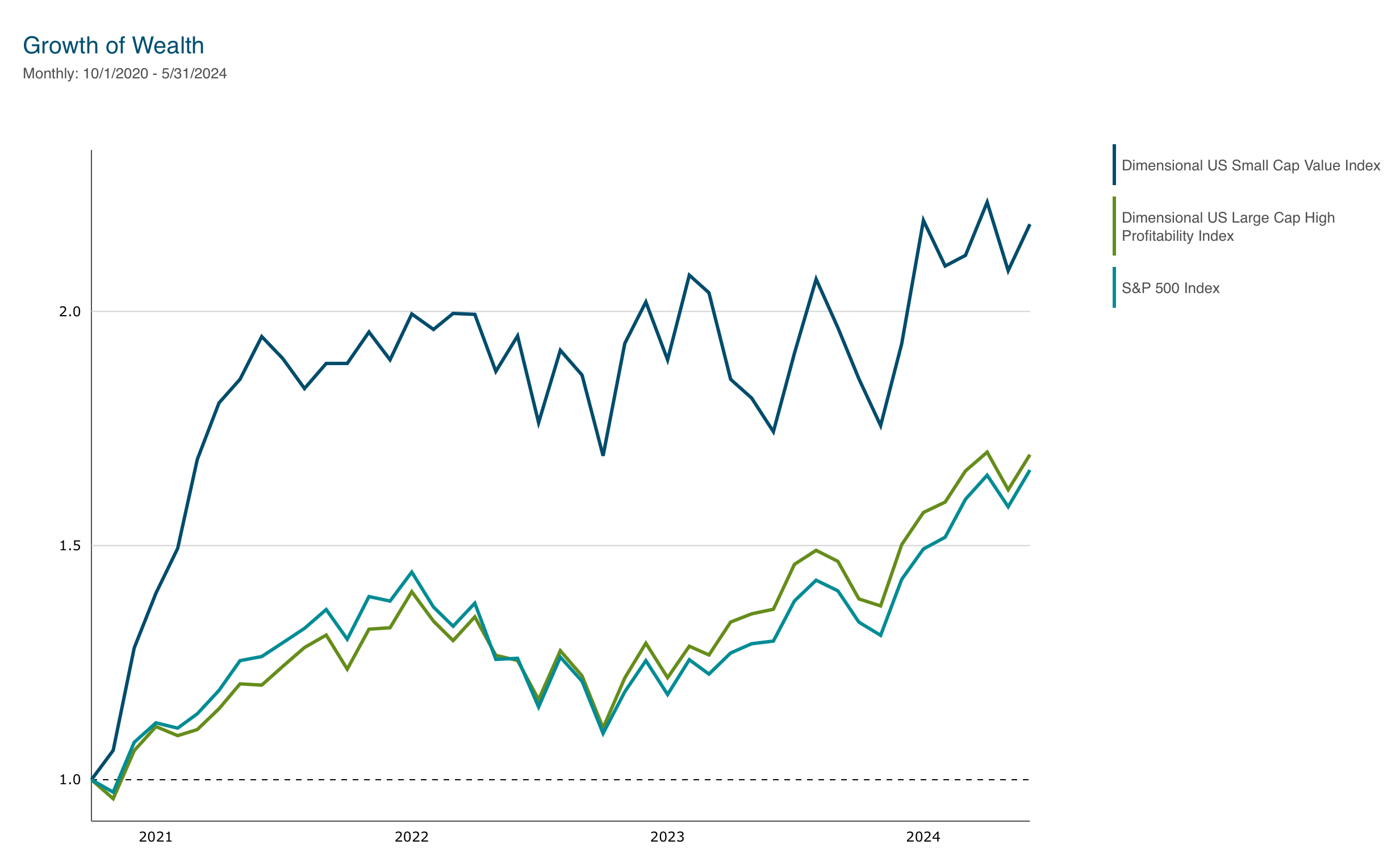

Everything else did follow, by the way; from October 2020 through May 2024 (the last month that index data is available), all stocks did well, but value came roaring back. The S&P 500 Index gained +14.9%, but the Dimensional US Small Value Index gained far more—+23.8% per year. If you're following along, you'll recognize this as a period where high profitability should not outperform significantly, and it hasn't—the Dimensional US Large Cap High Profitability Index gained +15.5%, in line with the market.

Which segment of the market will do the best for the rest of the year? Over the next couple of years? It's anyone's guess. It will probably be either good companies that trade for great prices or great companies that trade for reasonable prices. Going forward, I just want you to own some of both.

Do the evolution…c'mon, c'mon.

___________________________________

Past performance is not a guarantee of future results. Index and mutual fund performance includes reinvestment of dividends and other earnings but does not reflect the deduction of investment advisory fees or additional expenses except where noted. Indexes and mutual funds shown are for illustrative purposes only and may not be the only or any of the funds that Servo clients hold. Servo was not managing client portfolios over the entirety of the periods shown. This content is informational and should not be considered an offer, solicitation, recommendation, or endorsement of any particular security, product, or service.