I talk a lot about being disciplined in investing. You might be sick of hearing it. But I’ve learned from experience that most people don’t fail financially because their investments perform poorly. They often have less money than they should because they do the wrong things at the wrong time—they chase performance, panic and bail out of good investments, or just simply never get around to investing as they should.

But being disciplined doesn’t mean that you never make any investment changes. Of course we rebalance our portfolios—sell some of one asset class to buy another when a fund has gotten too big or too small relative to its original target. But that’s more of an adjustment. Actual changes are necessary when we learn more about investing, how investment markets work, and we can use these insights to improve our allocations and investing experiences.

However, knowing what insights matter and what changes to make is not easy. There is a lot of noise and most of the financial industry is trying to get you to trade and switch to their latest and greatest ideas. You don’t want to chase your tail, constantly adding and deleting funds, but you also don’t want your portfolio to become outdated.

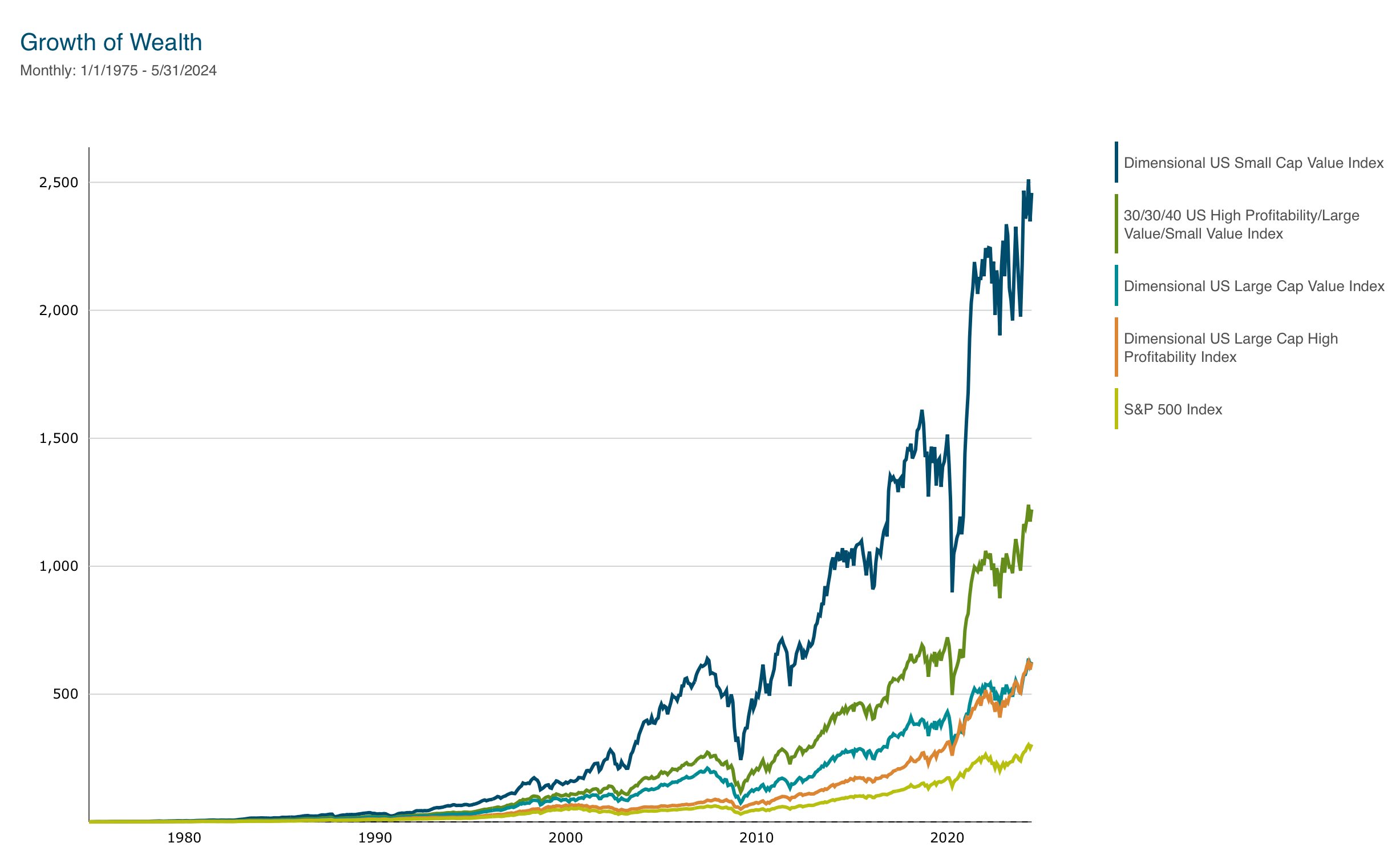

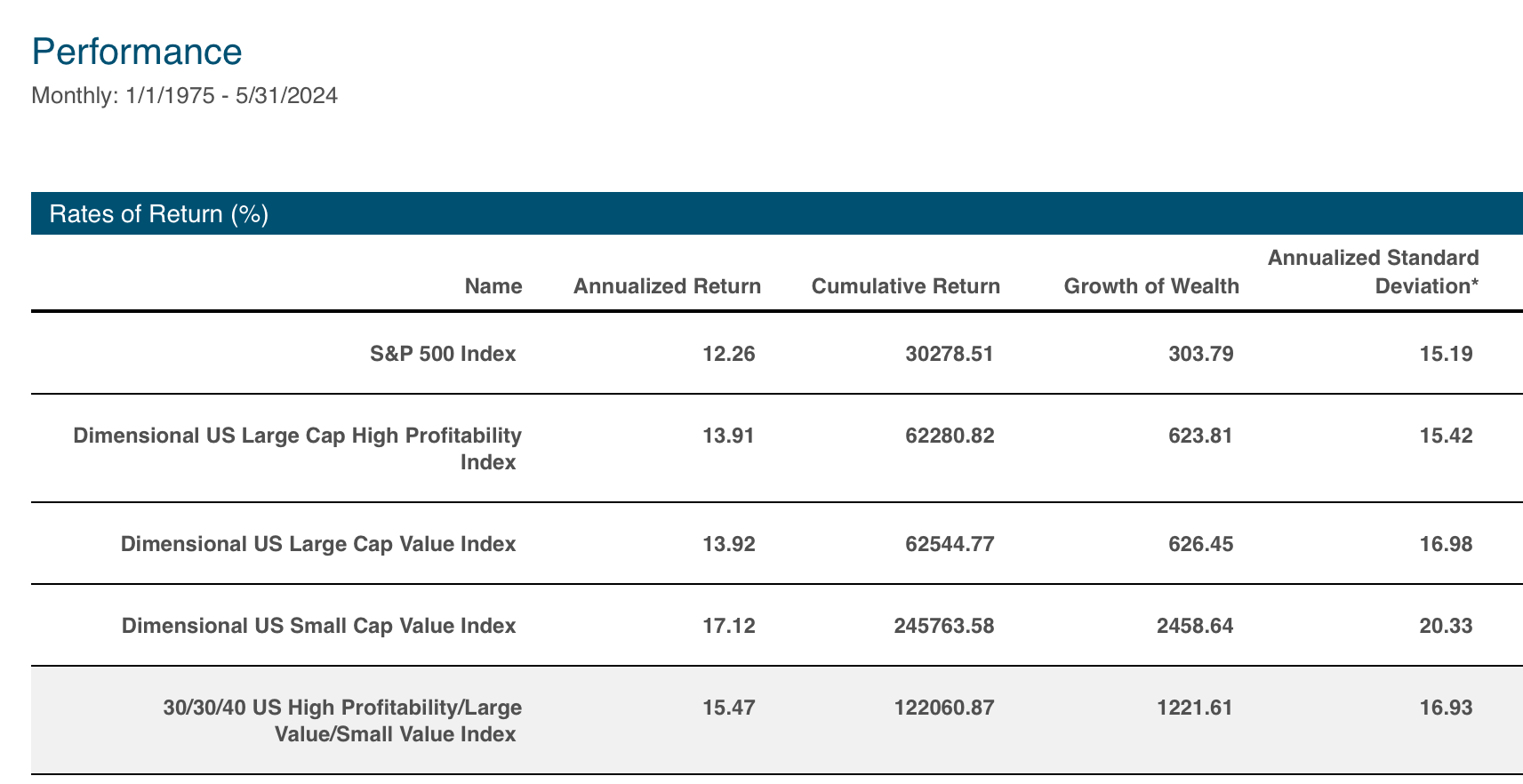

Once upon a time, we thought picking stocks and trying to time the market, buying actively managed mutual funds, was the best way to invest. But thanks to academic research from Eugene Fama that found markets were fairly “efficient” and hard to outguess consistently, we realized that professional managers don’t tend to beat the market. Instead, buying and holding a stock or a combination of stock and bond index funds, that owned all the stocks and bonds in the market, was a better approach. You wouldn’t have been undisciplined if you sold your stocks or active funds and bought a stock or stock and bond index funds. Active investing had become outdated. You were evolving with our knowledge about investing.

Almost two decades after the first index fund for retail investors from Vanguard arrived on the scene, additional research from Eugene Fama and his research partner, Ken French, identified two important considerations that drove long-term investment returns beyond the stock/bond split—the size of the stocks you owned and their relative prices (“value” vs. “growth”). Fama and French developed a simple model of expected investment returns that was remarkably all-encompassing, teaching us that you could earn higher long-term returns on your investments not just from holding more stocks than bonds (the original indexers knew this) but also from holding more small cap stocks and more lower-priced value stocks. You wouldn’t have been undisciplined if you sold some of your traditional S&P 500 stock index fund, which was chock full of large cap growth stocks, to buy US and international large cap value and small cap value funds. You would have been trying to increase your expected returns and improve your diversification. Simple indexing had become outdated. You would be continuing to evolve.

In the last decade, solid academic research, this time by Robert Novy-Marx, has been done on a different area of investing and returns: relative profitability. For those of us who for years thought about stocks in terms of large and small, growth and value, there wasn’t a lot of interest in company profitability because we assumed that profitable stocks had relatively high prices and low future-expected returns. That much is true. But a breakthrough in how we look at profitability and future potential profits, from the minutiae of erratic earnings to the stability of gross profitability, which excludes one-time and extraordinary corporate actions and items, has helped us better identify companies who are not just highly profitable today but expected to remain highly profitable. And stocks of companies with high future profits have higher expected returns. This has become another area of investing that is too significant to ignore. We need to evolve.

We’ve actually been including relative profitability in our investment portfolios for almost a decade but in a more understated way. In early 2013, Dimensional, working directly with Novy-Marx as they did with Fama and French when their research was published in the 1990s, began to reevaluate the stocks in their funds based on their relative profitability. In lower-priced value stock asset classes, there aren’t many companies with high profitability (or they wouldn’t be cheap!). But there were some really low and unprofitable companies. Novy-Marx’s research had shown that these companies had below-average returns; they weren’t very good long-term investments. So, Dimensional made a change to your portfolios. They evolved. Identifying value stocks based solely on their prices had become outdated; cheap stocks with some profits were good, but so too were more modestly-priced stocks with moderate profitability. Dimensional widened the price range of companies they bought to include slightly less value-oriented stocks so long as they were moderately profitable and kicked out the real unprofitable dogs regardless of how cheap they were. Dimensional wasn’t chasing performance nor were they undisciplined. The research said it was the right thing to do.

I’ve spent a lot of time looking at the higher profitability side of the market. The part of this research that appeals most to me isn’t that higher profitability stocks have higher expected returns. That’s fine, but we’ve already got that with our large and small value funds; by owning them our portfolios should have higher long-term returns than the market, even if that hasn’t been the case in the last decade. No, the appeal of high profitability is its diversification potential to a value stock-focused allocation. As I said above, stocks with high profitability tend to be larger companies with higher prices—they do their best when cheaper and smaller value stocks are doing their worst, and vice versa. Adding a fund that buys the most profitable companies in the US provides significant diversification to our portfolios with a foundation of US and international large and small value funds. We should use this fund instead of our existing large cap funds—US Large Cap Equity, US Equity ETF, etc., where making a change doesn’t prove prohibitive from a tax standpoint. It’s a better compliment to what we already own.

I’m excited about this change to our portfolios, to be honest. I’ve known about profitability for a while and have researched it extensively. I feel like this is a positive step forward without adding unnecessary portfolio complexity. I don’t ever want our portfolios or my investing process to become outdated, but I also want to be very careful and confident that a change is right for you and your family and mine as well.

Having discussed this update, I want to return to the topic of discipline that I started with. If our US High Profitability fund (or the ETF) doesn't perform “well” in the next few months or the next few years, we’re not going to abandon it; with any luck, it will do poorly because large and small value stocks finally return to their market-beating form. I have every reason to believe they will.

I’ll be in touch to discuss this change more in depth in the coming weeks. In the meantime, have a happy 4th!

___________________________________________________________

Past performance is not a guarantee of future results. Index and mutual fund performance includes reinvestment of dividends and other earnings but does not reflect the deduction of investment advisory fees or additional expenses except where noted. Indexes and mutual funds shown are for illustrative purposes only and may not be the only or any of the funds that Servo clients hold. Servo was not managing client portfolios over the entirety of the periods shown. This content is informational and should not be considered an offer, solicitation, recommendation, or endorsement of any particular security, product, or service.