Stocks have historically been the best investment for long-term investors to combat the costs of higher inflation. Small cap and value stocks tend to perform particularly well when inflation rises (I’ve written about this before, see here and here). So what’s going on with 2022?

Let me clarify my point and how we should think about stocks and inflation.

In the short run, higher inflation and rising interest rates pose challenges to businesses that affect their near-term earnings and profitability. A higher cost of capital and higher borrowing can set companies back, forcing them to make adjustments or change course. When this happens, we should expect their share prices to decline temporarily, only to resume their upward trajectory in the intermediate to long run as their proactive changes take effect.

How might this cycle impact investment portfolios? Let’s look at the 1970s, a period I’ve written about extensively, as the most valuable historical precedent for inflation and associated investment returns.

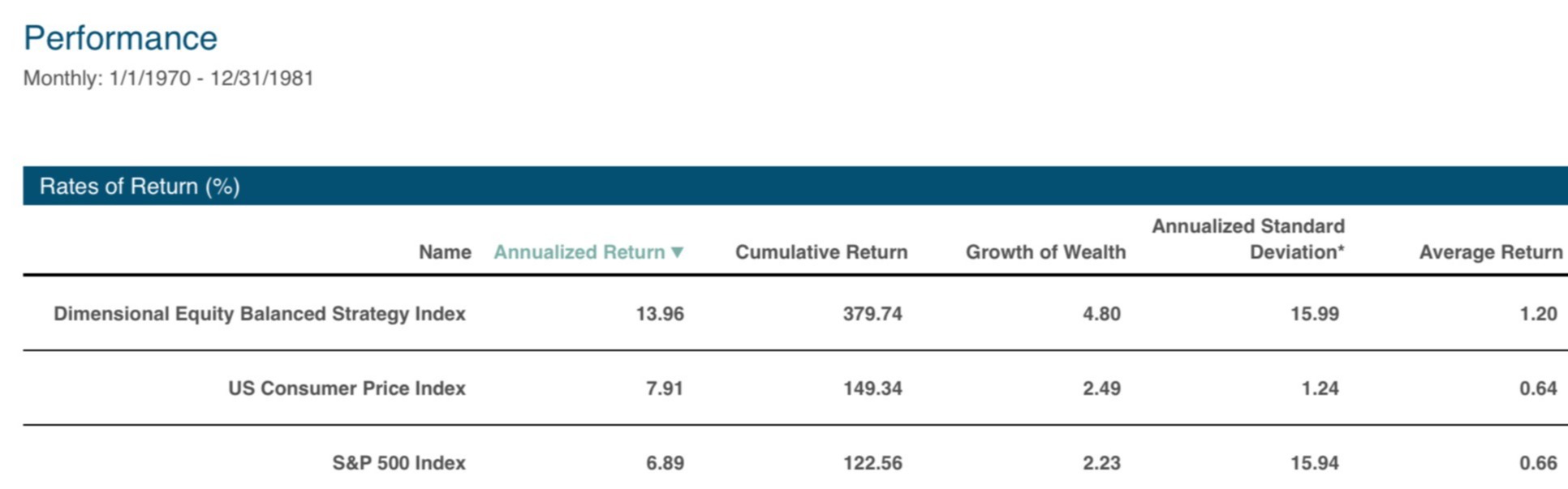

From 1970 through 1981, inflation—the Consumer Price Index (CPI)—rose at a rate of 7.9% per year; it cost $2.91 in 1981 to buy what cost just $1.00 in 1970. Breaking this period into different segments helps us to develop realistic expectations.

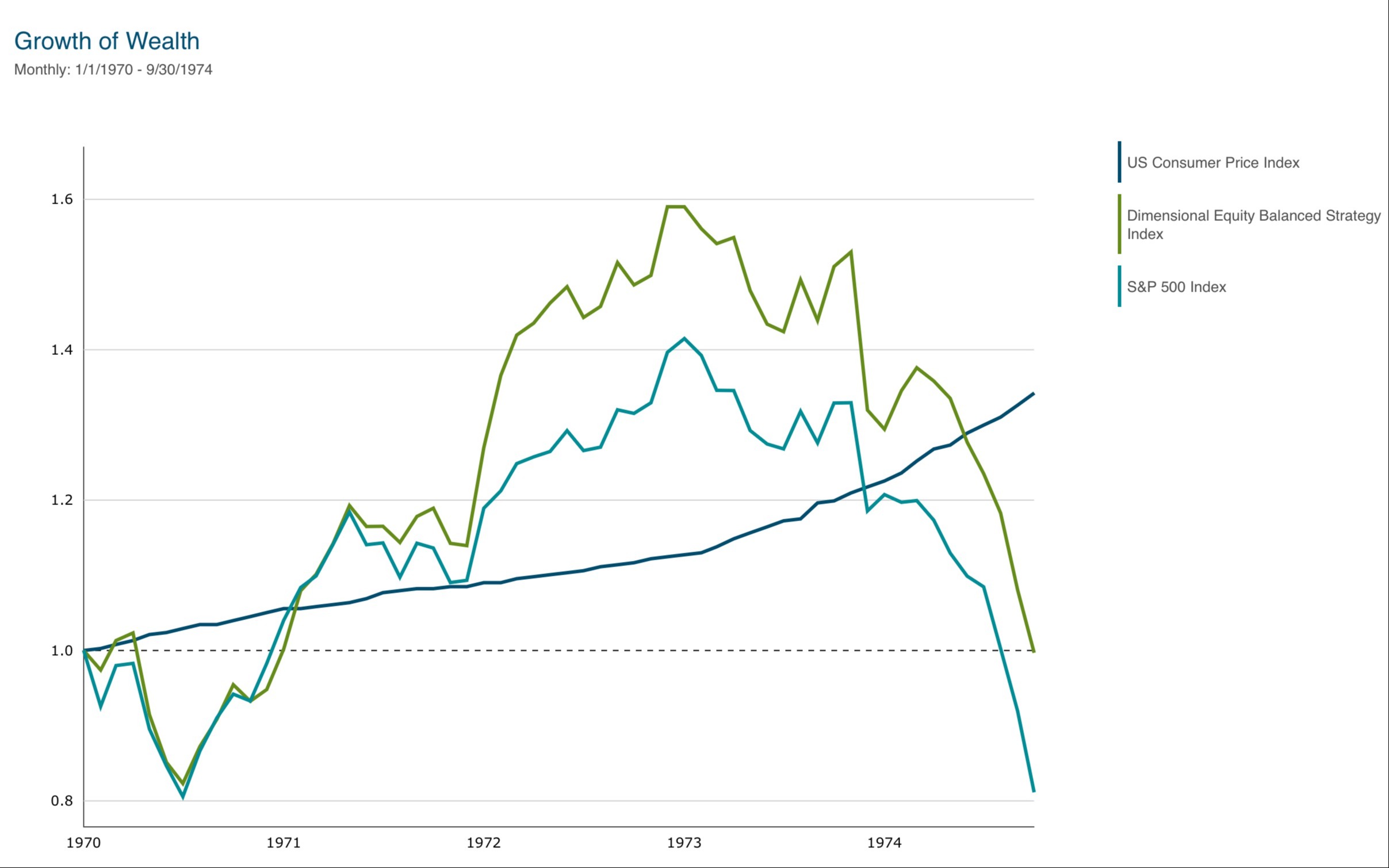

Inflation was 5.6% in 1970, settling back to 3.3% and 3.4% in 1971 and 1972, only to take off and grow at 8.7% and 12.3% in 1973 and 1974. These years are eerily similar to 2021 and 2022.

After a +12.3%/yr return for the S&P 500 from 1970 to 1972 and a +16.7%/yr return for the globally diversified, small/value-tilted Dimensional Equity Balanced Strategy Index, the bottom fell out, and all asset classes headed lower. From January 1973 through September 1974, the S&P 500 lost 42.6%, and the Dimensional Equity Balanced Strategy Index declined 37.3%. This was the most severe decline for stocks at the time since the 1930s Great Depression. By September 1974, the S&P 500 was 20% below where it started in 1970 and the Dimensional Equity Balanced Strategy Index was back to even, having given up it’s entire advance.

The decline was not, however, a permanent setback. Stocks began to recover in late 1974 and earned well-above-average returns through the remainder of the 1970s. The Consumer Price Index didn’t dip below 4% until 1982, but from October 1974 through December 1981, while inflation averaged 8.9% per year, the S&P 500 Index had a significant gain of +14.9% annually, and the Dimensional Equity Balanced Strategy Index gained 24.2% per year. These are extraordinarily high returns; most likely far higher than we would have seen without the 1973-1974 bear market.

Realize also that inflation didn’t have to break, nor did the economy need to heal, for equity prices to recover. If you’re waiting for things to “get better,” you’ll almost always miss the boat.

Over the entire 1970-1981 period, including one of the worst declines in the last century, a diversified stock portfolio effectively overcame inflation and delivered a significant positive real return to investors. The Dimensional Equity Balanced Strategy Index over these 12 years gained +14%/yr, 6.1% per year more than inflation. The S&P 500 Index did not fare as well. It earned just +6.9% per year, a decent return on a nominal basis, but 1% per year less than inflation.

Consider what these differences amounted to in practical terms.

A hypothetical investor with $100,000 saving for retirement in the Dimensional Equity Balanced Strategy Index in 1970 would have seen their portfolio grow four-fold, to $479,000, by 1981. This was significant appreciation, even net of inflation—their $100k was worth over $226,000 after inflation, more than doubling their real wealth.

A retiree with $100,000 in 1970 who needed $5,000 per year (5% of their first-year value), adjusted annually for inflation, would have ended with over $264,000 net of withdrawals in 1981 in the Dimensional Equity Balanced Strategy Index, despite drawing out over $88,000 in 12 years.

In the S&P 500 Index, results weren’t nearly as rewarding. Net of inflation, $100,000 invested in the S&P 500 in 1970 was worth only $88,000 by 1981, 12% less overall and almost 3x less than the Dimensional Equity Balanced Strategy Index ending balance. The retiree invested in the S&P 500 Index needing $5,000 per year plus inflation from their $100,000 would be down to $87,000 in principal by 1981; their withdrawal rate would have doubled from 5% to 10% of the portfolio. Yikes.

These examples are a warning to investors who have all their equity investments in a single asset class or have a strong bias in general to the large US growth stocks that dominate the S&P 500. Higher inflationary periods tend to favor smaller and lower-priced value stocks, not large cap growth companies. We see this in the recent data, too. From January 2021 through September 2022, while inflation has averaged over 8%/yr, the iShares Russell 1000 Growth ETF has lost 6.9%/yr, the Vanguard S&P 500 Fund Index lost 1.2% annually, while the DFA US Small Value Fund has gained 10.4% per year.

History doesn’t repeat, but it rhymes.

It can be a rocky road to earning a positive “real” (net of inflation) return on your stock portfolio, as the 1970s teaches us and as we’ve experienced in the last year. Higher inflation doesn’t lead to higher stock returns every year. But investors who can stay patient and disciplined tend to be rewarded with greater wealth, more income to live on, or both. It’s not that they don’t experience setbacks, but that these are temporary declines on the path to permanent positive intermediate and long-term returns.

If you hold a well-balanced equity portfolio, including global diversification and an emphasis on small cap and value asset classes, you’re on the right path; don’t allow your emotions to veer you off course and into a ditch in pursuit of a smoother ride. As the chart above shows, the lifetime rewards of investing well and staying disciplined can be extraordinary.

If you don’t have a plan to address higher inflation, or if you don’t have a well-diversified portfolio and are struggling to figure out how to design and implement one, you can schedule a few minutes here to chat with me to see if I can help improve your situation.

Dimensional Equity Balanced Strategy Index holdings available upon request.

Past performance is not a guarantee of future results. Index and mutual fund performance includes reinvestment of dividends and other earnings but does not reflect the deduction of investment advisory fees or additional expenses except where noted. This content is informational and should not be considered an offer, solicitation, recommendation, or endorsement of any particular security, product, or service.