I stopped filling out a March Madness bracket a few years ago. I don't watch as much regular season college basketball anymore, so when it comes to tournament time, I have no idea what's happening with most teams. Now, for some people, this is part of the fun—everyone knows a story of someone winning their bracket pool simply by picking the higher seeds or their favorite mascots. And I admit that predicting a huge upset (while ignoring how many other upsets you picked that didn't pan out) is fun and worth bragging about. I'm just not into guessing; any success I'd have, I know, would be due to luck, which, for me, spoils the fun.

But I watch the opening two weeks of the tournament; that much I still enjoy. When we reach the Final Four, I have a better idea of what's going on. I've seen all four teams play at least once and have picked out my favorite players and matchups to watch. For me, the Final Four is the best part of the tournament. We've got underdogs (NC State!?!), runaway favorites (UConn), surprise stars (have you seen DJ Burns?), and the team with the consensus Player of the Year (Zack Eddy at Purdue). These games really matter because these teams are so close to the ultimate goal of winning it all.

Successful investing is a lot like the Final Four. There were 351 different Division I schools that began the year competing to make the Final Four, and it can seem like there are almost as many different investment products, philosophies, research, and insights on which you might use or choose to base your financial decisions. But just as most college basketball teams won't make it to the final weekend, most of these financial products and viewpoints won't matter much. They won't move the needle in terms of enhancing your long-term wealth.

What does matter? The truth is, when we look across the field of investing theory, four main principles emerge.

#1–It doesn't make sense to try and outguess the market.

Some people think the way to make money investing is to pick the right stocks or time to be in and out of the market. It's not. Outguessing the stock and bond markets and trying to find mispriced or undervalued stocks or bonds doesn't work well. Individual investors are terrible at it, and even the professionals who manage stock and bond portfolios for a living don't do very well. Let's look at the evidence.

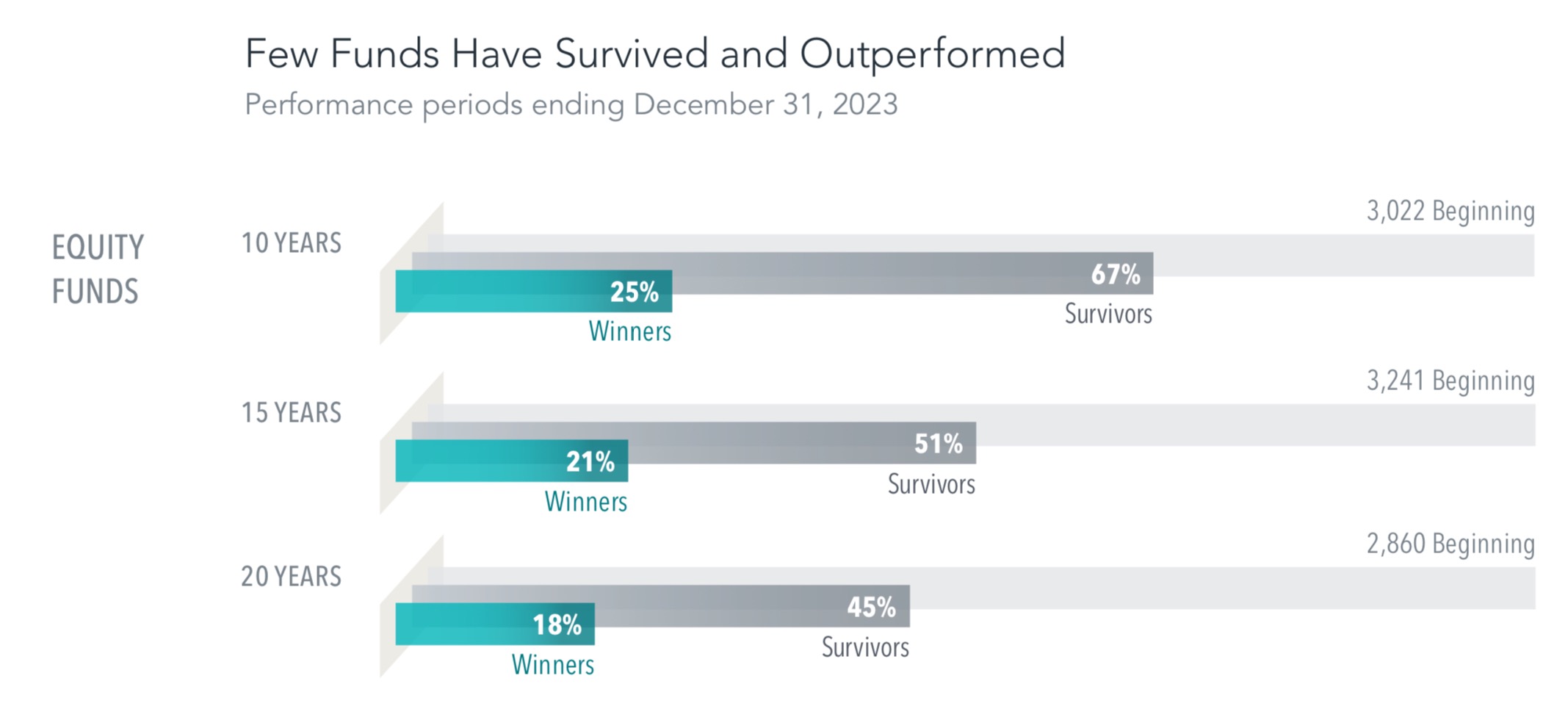

The chart below shows the results of all of the professionally managed mutual funds that existed 10, 15, and 20 years ago and how they have faired relative to their index (mutual funds that pick large stocks are compared to the S&P 500 Index, small companies to the Small Cap Index, etc.). This is not what success looks like. Over the last 20 years, for example, only 45% of the professionally managed funds survived! The majority—55%—had returns so bad they went out of business. Only 18% managed to survive and outperform their index. More than four out of five failed.

When it comes to investing, start with the belief that you're better off buying and holding a low-cost, well-diversified portfolio of stocks and bonds appropriate for your goals and only changing it when your circumstances change. Trying to pick just a few winners or a hot fund manager or trading your portfolio to avoid the inevitable declines is almost certain to cost you.

#2–Risk and return are related

Everyone would love to earn a high return on their investments without taking risk. This is one of the reasons why con artists and Ponzi schemes persist to this day, despite countless stories of people being fleeced for trying to get something for nothing. Unfortunately, there's no investing axiom more accurate than the notion of "no pain, no gain." Generally, the more risky and volatile your investments, the more you are likely to earn in the long run.

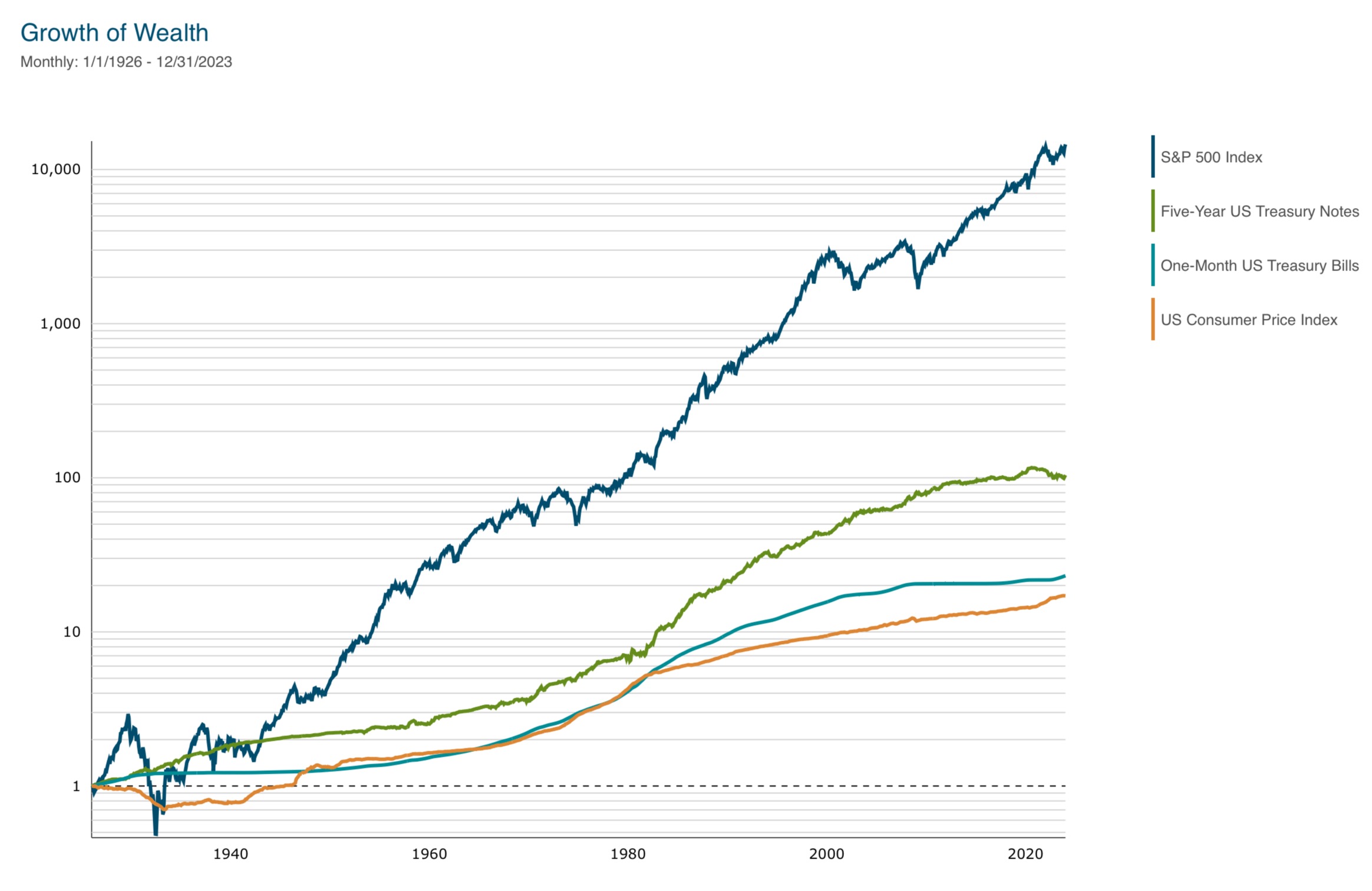

Look at the graph below, which reports the growth of $1 in cash, bonds, stocks, and inflation. You'll notice that the most stable returns come from cash—One-Month Treasury Bills. These are often referred to as "risk free," but after accounting for the rising inflation costs—the Consumer Price Index—they're also return free; inflation and T-bills have averaged about +3% per year over time. You don't have to face any uncertainty and get nothing back in return. Bonds—Five-Year Treasury Notes—are a little more volatile and uncertain and have rewarded you with a little more in returns, about +5% per year. However, you've had to accept a lot of short-term uncertainty to get the highest overall potential return that many people need to achieve their long-term goals. Stocks—the S&P 500—have averaged about +10% per year but have had highly volatile short-term returns.

The bad news is that you have to take an investment risk to achieve your financial goals; the good news is, as we see from almost a century of data, you've been handsomely rewarded over time for accepting this fact.

#3–Not all stocks and bonds have the same expected returns

We've seen that stocks and bonds have very different long-term returns. Still, most investors don't know that there are also differences in returns within stocks and bonds. You can use this information to design a more diversified portfolio with a better chance of achieving your goals.

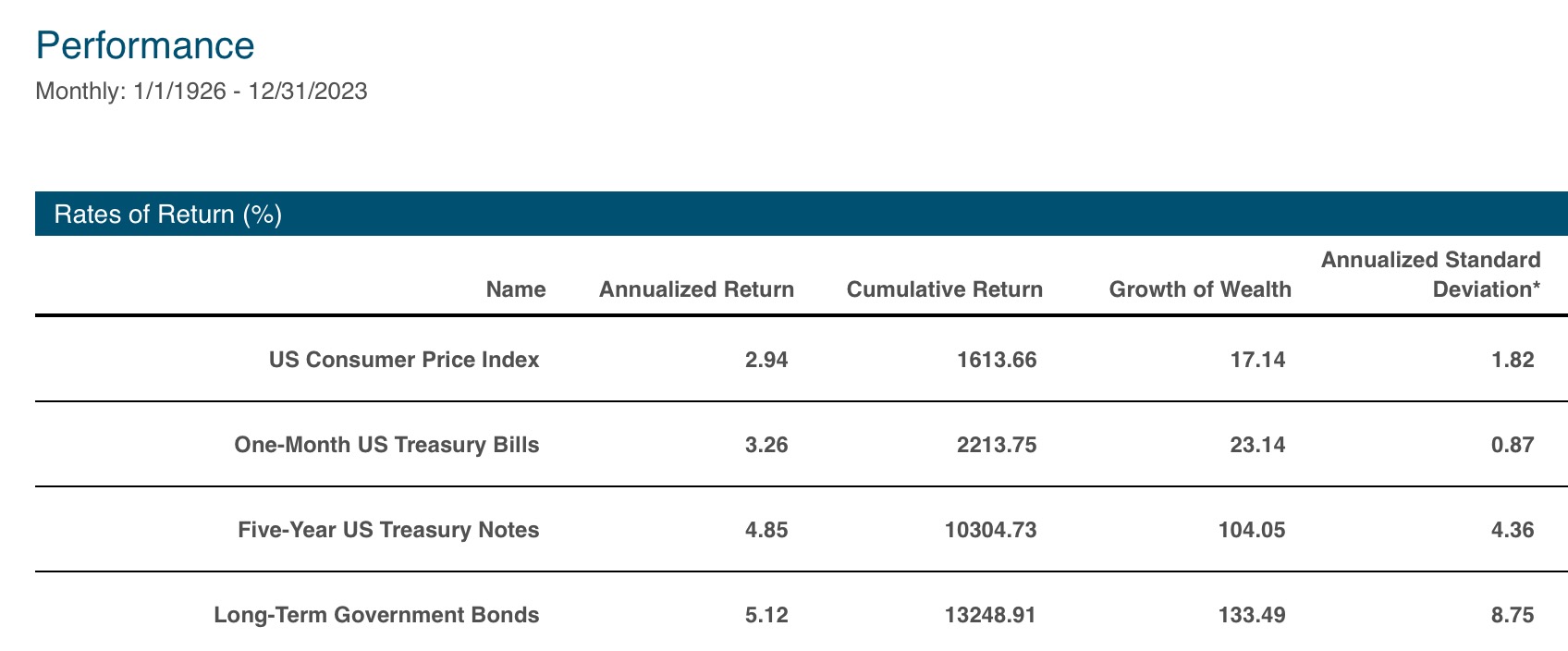

Let's start with bonds. In the graph above, we saw that extending the maturity of your fixed income matters. Five-year bonds did better than one-month T-bills. But this only works up to a point. The table below shows that going out even longer, to 20 years (see Long-Term Government Bonds), has not resulted in any additional return over five-year maturities. Long-term bonds do, however, have much greater risk and volatility as measured by standard deviation. If you're going to own bonds, it makes the most sense to stick to maturities of five years or less, and not take the added risk of longer-term bonds.

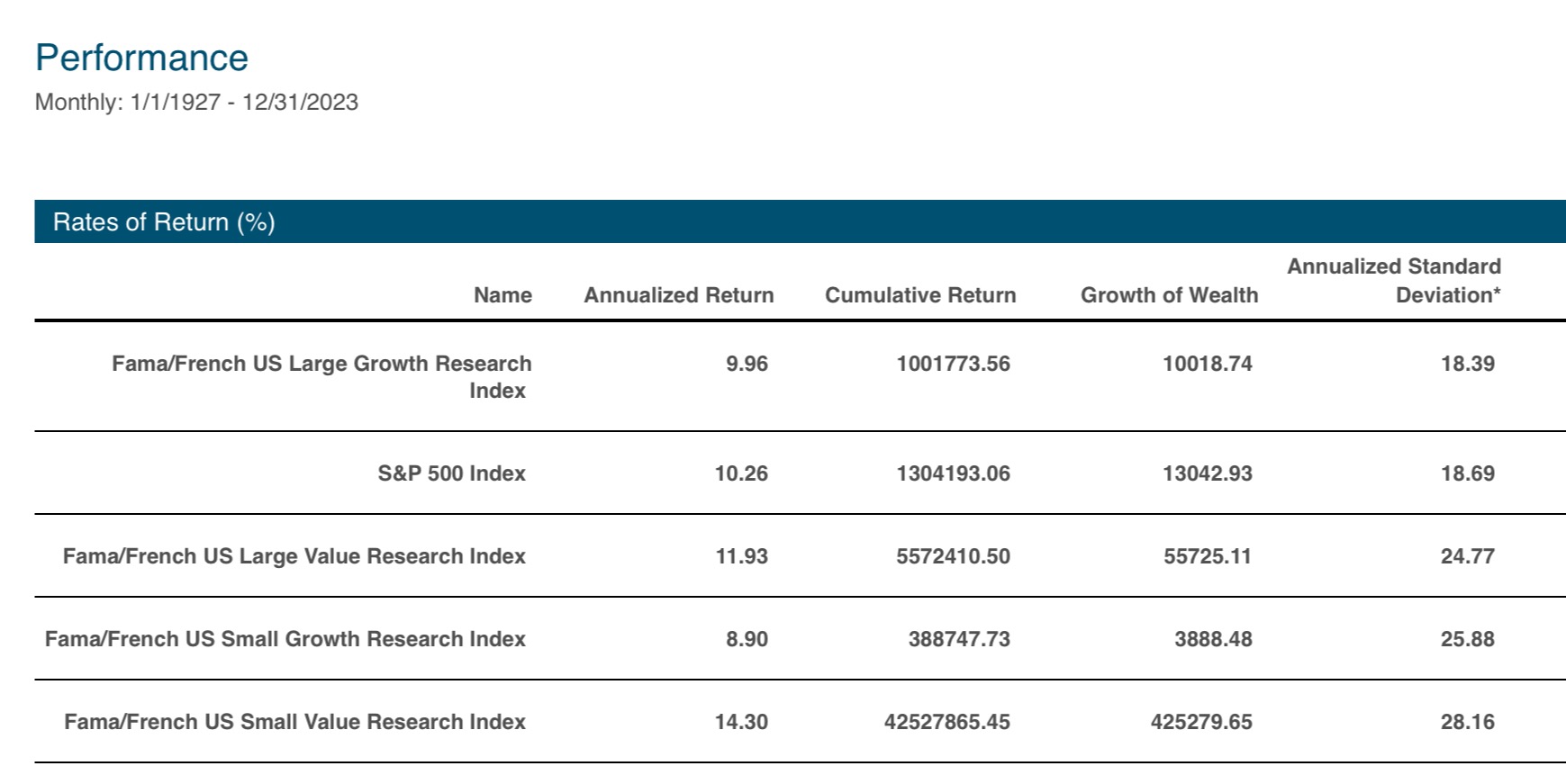

There are also considerable differences in the expected returns of various groups of stocks. A clear pattern emerges if we look at the difference between higher-priced "growth" stocks and lower-priced "value" stocks in the table below. Even though growth companies tend to be well-run and well-known businesses, they have low relative returns. Their high prices act like a lead weight around their future returns. Instead, lower-priced, beaten-down value stocks, especially small value stocks, have produced the highest long-term returns.

The hard part for investors to grasp is that value companies don't tend to be as profitable or glamorous as growth companies; why would they do better? Because their relative prices are lower, they have more potential upside returns. Glamorous growth companies also have difficulty staying on top—Apple and Microsoft have been the exception and not the rule. Most growth companies lose their competitive advantage, and their stock price underperforms. Do you even remember AOL or Sun Microsystems? Former tech stalwart and growth-stock darling Intel trades at a price today below where it was in the late 1990s!

So, for most investors, a well-diversified large cap or broad market fund, represented below by the S&P 500 Index, is a good starting point. But ending with the S&P 500 might cost you lower long-term returns and less diversification, as everything you own is in the biggest and highest-priced companies. Adding large value and small value stocks through a structured asset class mutual fund or exchange-traded fund can result in a better portfolio. Further diversifying into international stocks, combining large and small value funds, can improve your portfolio's prospects and lead to higher expected returns and a smoother ride.

The trend in investing today is to just put everything into an index fund like the S&P 500—as the evidence shows, there are better ways to invest. Hold a more diversified stock portfolio that includes US and international large and small value stock asset classes. If you're in retirement and need to withdraw from your portfolio, keeping a small allocation to short-term bonds can also make sense for you.

#4–Managing your investments means rebalancing and staying disciplined.

Here’s a secret that most investors hate to admit: They’re not very good at managing their investments.

Even if you know how to invest and can design a sensible portfolio, sticking with it over time is difficult. Almost all investors make a few common but costly mistakes. They chase the performance of investments that have done very well that they didn't own or own enough of, panic during bad times and bail out of their portfolios to avoid experiencing more significant losses, and exhibit overconfidence in their decisions—they think they're better able to forecast future investment returns or the role that financial conditions will have on the markets.

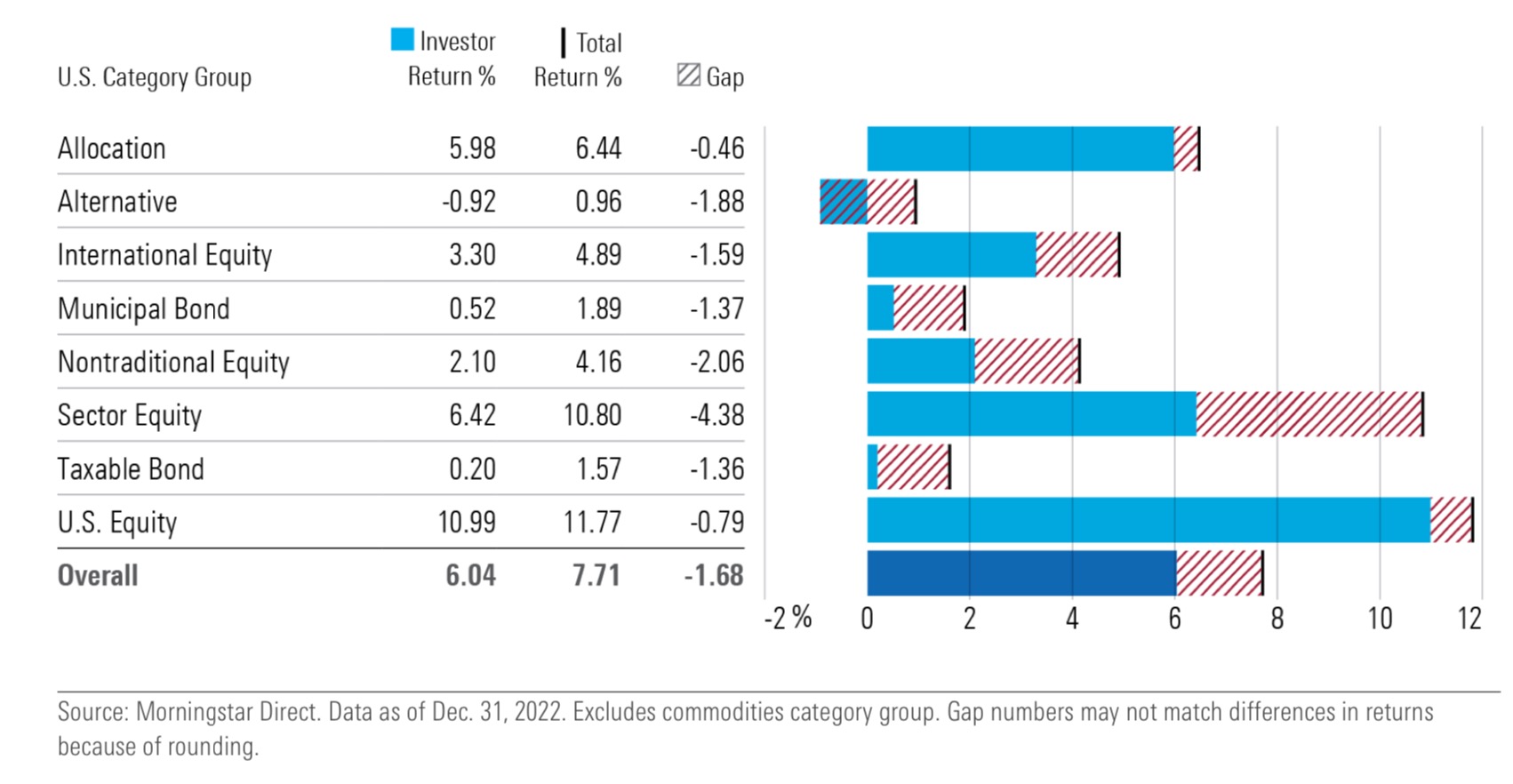

The result is that investors earn a far lower return in their portfolios than the returns of their investments. My favorite example of this comes from a study by mutual fund rating and research company Morningstar, listed below. When they looked at how mutual investors fared over the decade ended in 2022, they found that while the average fund gained +7.7% per year, investors in those funds earned only 6% a year! There was a 1.7% %-a-year difference that came about because most people repeatedly made the mistakes I listed above. Doing the wrong thing with your investments at the wrong time can be extremely costly!

What we’ve seen in this article is that understanding what matters and how to invest can help you earn considerably higher returns. Buying and holding a portfolio with more stocks than bonds, and more value and small cap stocks, has historically netted you several percent a year in better results compared to bond-heavy, large growth stock-oriented portfolios, especially one that is concentrated and tries to outguess the market.

However, knowing how to manage your investments can also help improve your returns. Instead of chasing performance, panicking, or making portfolio tweaks based on forecasted interest rates, stock valuations, or tax policy, you're better off sticking to your set allocation and "rebalancing" it back to its target periodically. This means having a pre-set allocation and directing periodic dividends and interest payments to the part of the portfolio that's most underweighted or further selling some of the most appreciated holdings to buy more of what's appreciated less or even declined. This "buy lower, sell higher" approach to investing can lead to better long-term returns but also provide you greater confidence, discipline, and peace of mind—you're no longer forced to make regular judgments about what to buy and sell and whether it's a good time to do it. Rebalancing is a pre-planned and mechanical approach that takes the emotions out of investing and increases your odds of success.

Taken together, the “Final Four of Investing” I outlined in this article can have a considerable lifetime impact on your savings and wealth:

- Don’t try to outguess the market,

- Accept that risk and return are related,

- Understand that there are differences in returns within stocks and bonds, and

- Manage your investments by rebalancing and staying disciplined

If you’re a new or long-time blog reader and know you need help with your investments, or if you’re a Servo client and want to discuss any of this, don’t hesitate to schedule an appointment using the link at the top of the page (Servo clients are also free to call or email me if they prefer).

_________________________________________

Past performance is not a guarantee of future results. Index and mutual fund performance includes reinvestment of dividends and other earnings but does not reflect the deduction of investment advisory fees or additional expenses except where noted. Indexes and mutual funds shown are for illustrative purposes only and may not be the only or any of the funds that Servo clients hold. Servo was not managing client portfolios over the entirety of the periods shown. This content is informational and should not be considered an offer, solicitation, recommendation, or endorsement of any particular security, product, or service.