Imagine owning an investment portfolio worth $7.2 billion. Now imagine you've allocated it so badly that this year—in the middle of a bull market and all-time highs for stocks—you have to borrow $800 million, outside of the portfolio, to meet ongoing funding needs.

This is a true story.

Am I talking about the worst investor in the world? Not even close. One of the most sophisticated. I'm referring to Brown University and its endowment, staffed by dozens of experienced, full-time investment managers and financial analysts.

Brown is not alone in their troubles. Northwestern has a $14.3 billion endowment and has had to borrow $500 million. Harvard, with $53.2 billion, has one of the largest endowments, yet it borrowed $750 million in April.

What happened?

This spring, when the Trump administration threatened to cut off federal funding to universities, their endowments once again realized that, despite managing billions of dollars, they cannot access most of it in a timely fashion. College endowments and state pension funds went through a similar experience during the financial crisis in 2008-2009, proving that even for smart and experienced investors, once bitten doesn't mean twice shy.

The inability to access your money probably doesn't make sense to you as an individual investor with stock and bond mutual funds and exchange-traded funds. But college endowments and state pension funds don't invest like you. They think they can do better. Whether they can is debatable. What they can do is make investing a lot more complicated.

According to a Wall Street Journal article last month, educational endowments with more than $5 billion in assets hold just 2% in cash, 6% in bonds, and 24% in stocks (8% in the US and 16% in international companies). Where's the other 68%? In private funds and other non-traditional assets, "that can't be readily turned into cash." Very fancy. But according to the article, "universities are slashing budgets, freezing their hiring and scrambling to raise money any way they can." What good is keeping your valuables in a safe if you don't have the combination?

A solid asset allocation policy is essential for all investors—big and small—it aligns your long-term savings with the most appropriate asset classes and overall portfolio for those goals, considering the growth objectives and liquidity constraints, including the potential need for cash when you least expect it. Think of it like your GPS when you're driving in an unfamiliar area, guiding you safely and efficiently to your destination..

Few colleges saw the emerging government funding threat ahead of time, but that doesn't make them unique. Everyday investors, including Servo clients who are saving for retirement or spending in retirement, often face surprises as well, or opportunities they didn't expect. We are just better prepared.

How?

We don't own portfolios full of complex investments that are hard to understand and often even harder to sell. Our investment policies and portfolios are simple. They're binary.

Our contrast with endowment investing starts with our first decision.

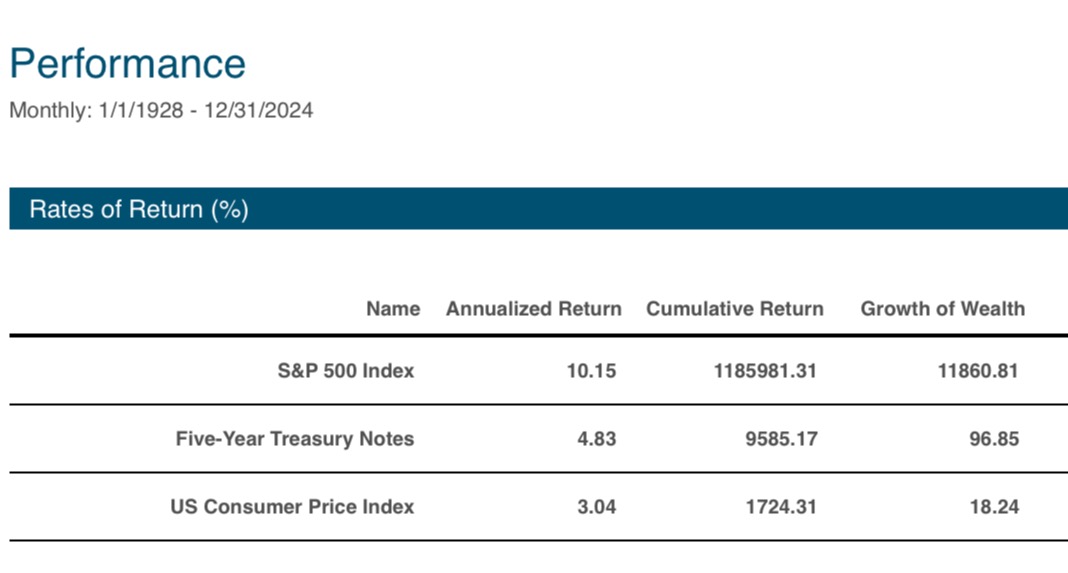

The two major asset classes we consider are public stocks and bonds. As long-term investors trying to earn returns significantly above inflation to fund our retirement, income, and inheritance goals, we find stocks to be the obviously superior starting point and, unlike endowments, worthy of the majority of our wealth. Since 1928, the S&P 500 has returned +10.2% per year compared to just +4.8% per year for 5-Year Treasury Notes (bonds) and 3% for inflation. Owning stocks is, without a doubt, the best way to create and grow real wealth.

Unlike endowments, we don't look to alternative asset classes or private markets for higher returns or added diversification.

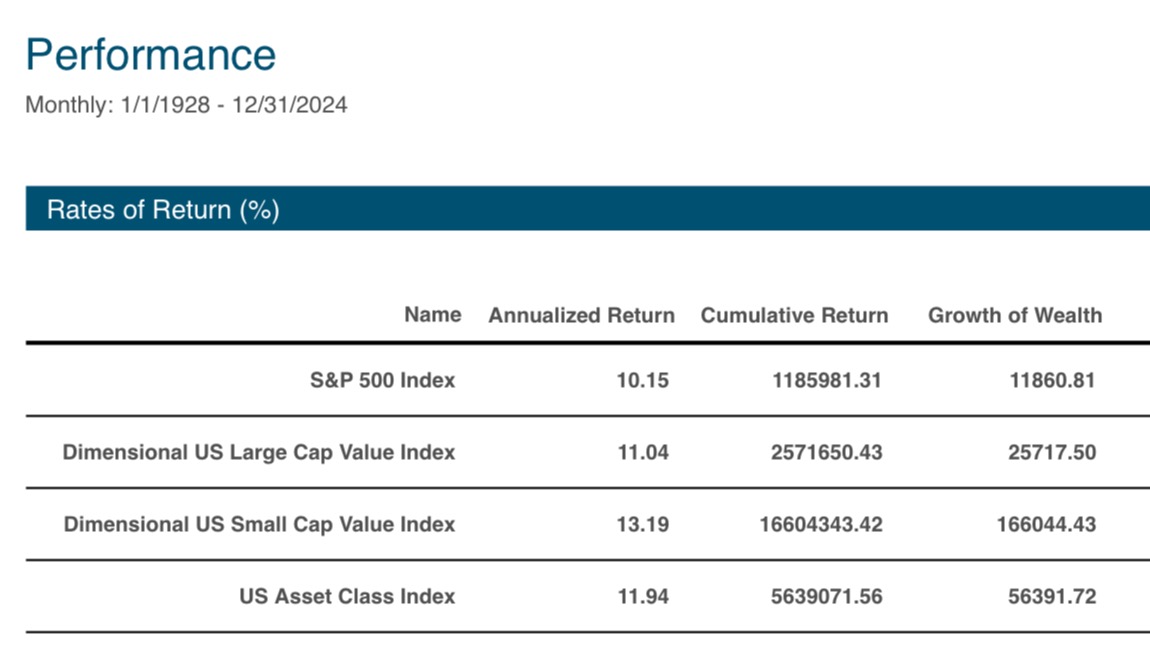

Why not? We've already found those things in different asset classes within the stock market. Large and small stocks with lower prices—"value stocks"—have had higher long-term returns compared to the S&P 500, which tends to emphasize the biggest stocks with the highest overall prices ("growth stocks"). Over the same period, the Dimensional US Large Value Index returned +11% per year, and the Dimensional US Small Value Index returned over +13% per year. A balanced allocation of 30% S&P 500, 30% Large Value, and 40% Small Value (“US Asset Class Index”) returned +11.9% per year, almost 2% annually more than the S&P 500.

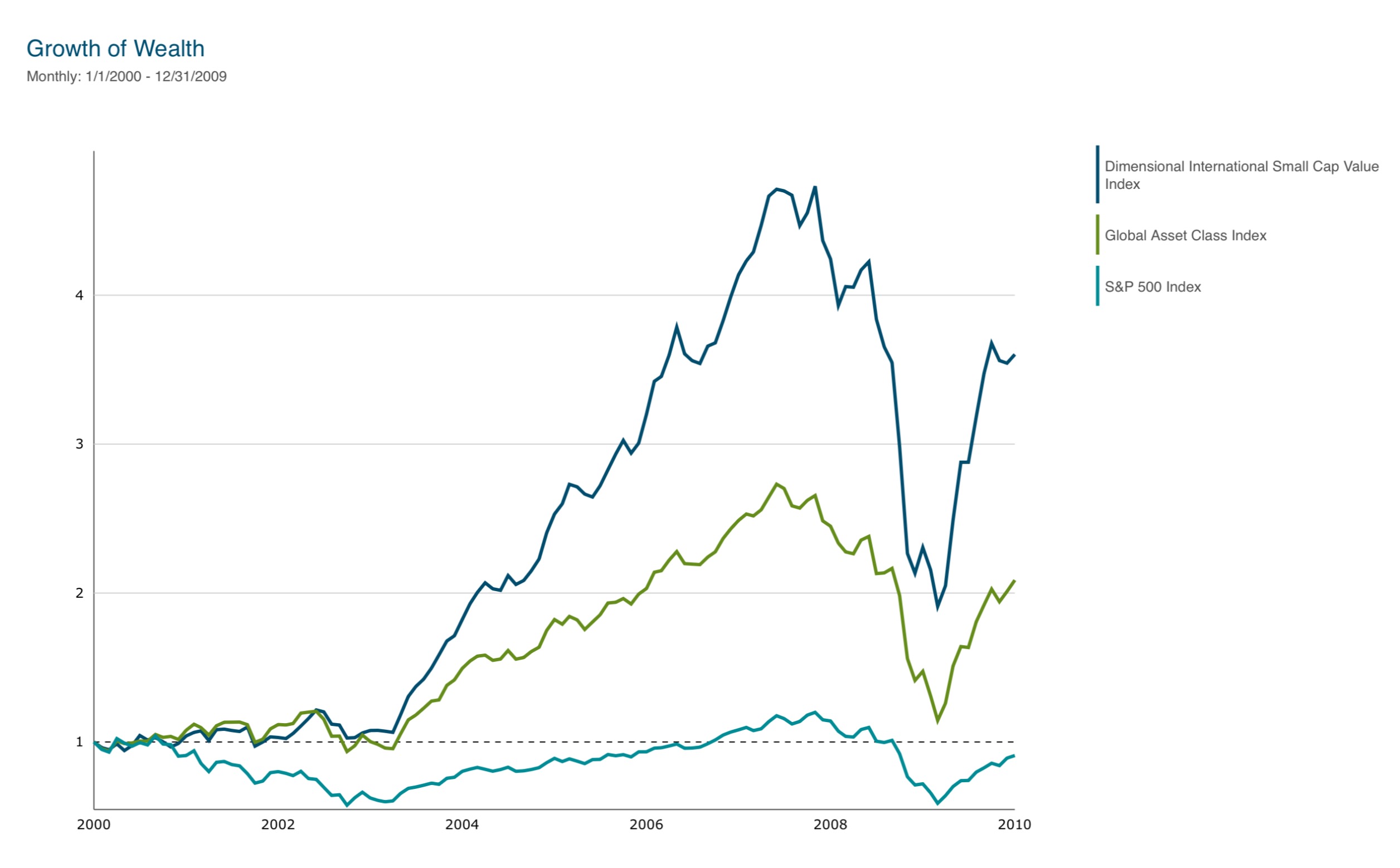

Holding different stock asset classes, and not just US large companies, has also improved diversification, especially when we extend our portfolios further into non-US developed country markets, including international large and small value stocks. The most challenging period in recent investing history was the decade from 2000 to 2009, during which the S&P 500 Index had a cumulative return of -9%, including dividends. But a globally diversified asset class stock index*, which includes US and international large and small value stock asset classes, and replaces the S&P 500 with a more refined US large cap high profitability stock index, returned +7.6% per year and over +108% cumulatively. International small value stocks were most beneficial, gaining +13.7% per year, almost 15% more per year than the S&P 500 over this stretch.

Once we've built our core stock asset class portfolio, we return to bonds.

This time, we reconsider them for the one thing they're actually good at: Preserving principal, even in bad times. In the 97 years since 1928, the S&P 500 has declined on an annual basis 26 times, averaging a loss of -13.4%. Average bond returns (5-Year Treasury Note Index) in these 26 years were the same as their long-term average, +4.9% annually. Said differently, the main benefit of bonds is that they are often unfazed by bear markets.

We also invest in bonds differently from endowments.

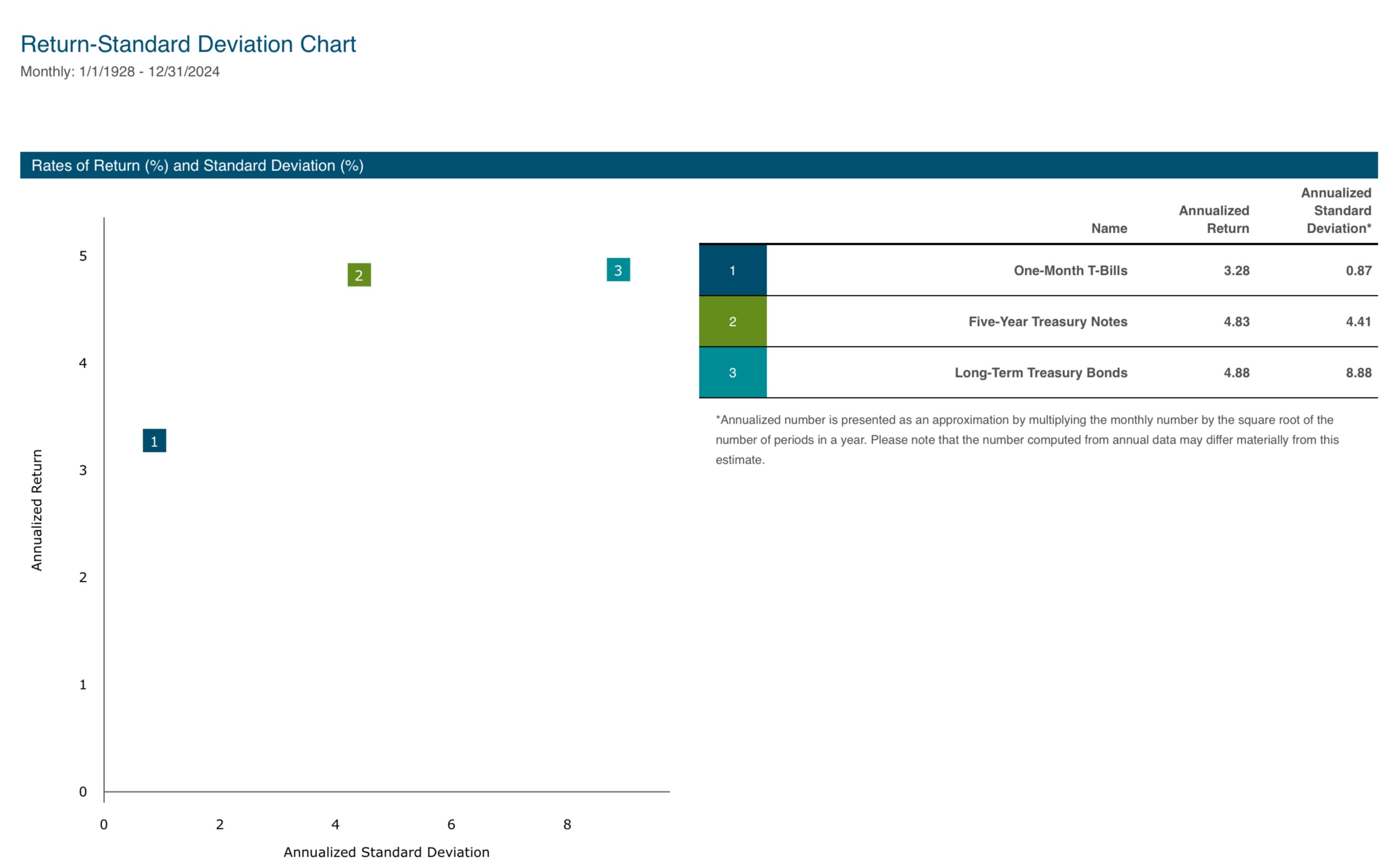

In terms of maturity, they favor long-term bonds for their perceived diversification benefits and higher expected returns. We know better. There has been no long-term benefit to extending bond maturities beyond shorter-term, five-year maturities. 20-Year Treasury Bonds have earned only 0.1% greater returns since 1928, but have come with double the volatility (“standard deviation”) and much greater inflation risk. For what is supposed to be the relatively stable part of a diversified portfolio, we know that accepting greater risk for no additional return isn't a smart move.

Longer-term bonds also don't add more diversification; in the 26 negative years for the S&P 500, 20-Year Treasury Bonds averaged +4.3% (0.6% per year less than 5-Year Treasury Notes), and lost value in seven of those years, compared to just three for shorter-term 5-Year Treasury Notes. In 2022, 20-Year Treasury Notes lost -26.1%, 8% more than the -18.1% loss for the S&P 500! That's de-worse-ification.

We base our portfolio allocations on our long-term growth and return goals and short-term spending needs.

The critical question in deciding the stock/bond split is: How much are you spending, and how many years of that to put in bonds? If you're still saving, or at least don't need any withdrawals? Bonds aren't necessary; an all-stock allocation makes the most sense. However, for an investor in withdrawal mode, such as someone with $1 million who spends $50,000 per year, they may decide that three years is enough; others may find five years more comforting. A few might want seven years. This decision cements their investment policy—85% stocks and 15% bonds in the first example, 75/25 in the second, 65/35 in the third. That's the asset allocation we stick with and rebalance back to until the spending needs or overall goals change.

We also have a different spending strategy.

In good years, our portfolio spending comes from selling shares of stock funds that have risen in price, selling more of what's done the best. In bad years, which we readily acknowledge happen every so often, we take withdrawals from the bond side of the portfolio, which we expect to hold up reasonably well, even when stocks and the economy are in crisis. For us, there's never a bad time to take money out of our portfolios if we have a good use for it. We don't get caught off guard by surprise income needs.

Admittedly, our simple, binary investment approach isn't nearly as exciting, nor does it seem as sophisticated as the endowment strategy. We don't have any star managers (soon to be former star managers), and we don't own exotic strategies that entertain friends at parties. The tradeoff is that our approach is intuitive, based on common sense, easy to remember, and actually works.

In other words, if it's a surprise party and we're the ones hosting, we'll have no problem paying for it from our portfolios, even at the very last minute.

_____________________________________

Source of index returns = Dimensional Returns Web

Global Stock Asset Class Index = 21% Dimensional US Large Cap High Profitability Index, 21% Dimensional US Large Value Index, 28% Dimensional US Small Value Index, 18% Dimensional International Value Index, 12% Dimensional International Small Value Index, rebalanced annually.

Past performance is not a guarantee of future results. Index and mutual fund performance includes reinvestment of dividends and other earnings but does not reflect the deduction of investment advisory fees or additional expenses except where noted. Indexes and mutual funds shown are for illustrative purposes only and may not be the only or any of the funds that Servo clients hold. Servo was not managing client portfolios over the entirety of the periods shown. This content is informational and should not be considered an offer, solicitation, recommendation, or endorsement of any particular security, product, or service.