“Everyone I talk to has lost a ton of money this year; what’s going on?”

I’ve heard this question several times from clients and potential clients in the last few months. Surprisingly, 2022 looks like it will be the exact opposite of the Covid lockdown-related bear market in 2020. Look at the table below to remind you of what happened a few years ago.

Stocks collapsed in Q1 of 2020, with the S&P 500 declining almost 20%. Large technology-oriented stocks that dominate the NASDAQ Index were also down, but they held up relatively better, losing just 14%. Smaller and more value-oriented stocks got hit the hardest; the DFA US Large Value Fund dropped 31.5%, and the DFA US Small Value Fund declined a whopping 39%. These declines rivaled the total-year losses for small and value stocks in 2008! The international stocks of Europe and Asia (MSCI EAFE Index) fell more than US stocks, and non-US small cap and value stocks mirrored their US counterparts in losing even more.

To make matters worse, 2020 was just the latest bear market in recent years to see small cap and value stocks decline more than the market (S&P 500 Index). We previously saw sharp stock declines in Q4 2018, the summer of 2011, and of course 2007-2009, all of which entailed small cap and value stocks losing the most. The expectation for large and small cap value stocks—to generate higher long-term returns and provide added diversification benefits—appeared to have disappeared.

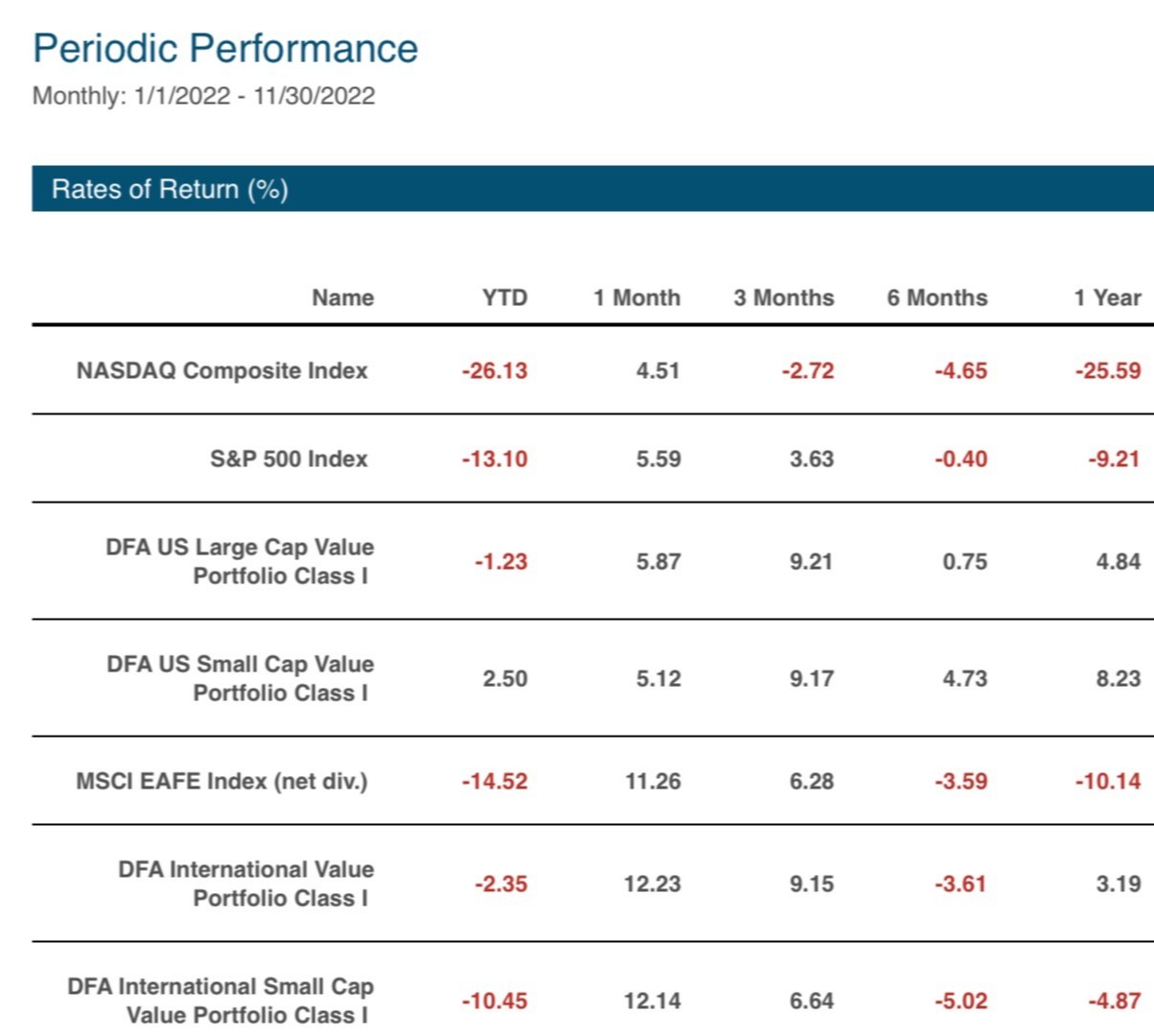

But 2022 has been different. Rising inflation and interest rates have hit large cap and growth stocks much harder, while smaller and more value-oriented stocks have barely budged; the table below tells the story.

Through November of this year, the NASDAQ Index is down over 26%, double its decline in Q1 2020. The S&P 500 Index is down over 13%. Many investors had shifted much of their portfolio to large cap US growth and technology stocks in recent years after an unexpectedly good run, and are typically down 20% or more this year. Not so for value asset class investors. The DFA US Large Value Fund is down just 1%, and the DFA US Small Value Fund has gained 2.5%. International developed country (MSCI EAFE Index) stocks are down about the same as the S&P 500, but we also see much better returns for large and small value stocks.

Over the last year, while the NASDAQ, S&P 500, and MSCI EAFE Indexes are all down 9% to 25%, three value stock asset classes in developed markets—the DFA US Large Value Fund, DFA US Small Value Fund, and DFA International Value Fund—are all up. The lone loser, DFA International Small Value, is down less than 5%.

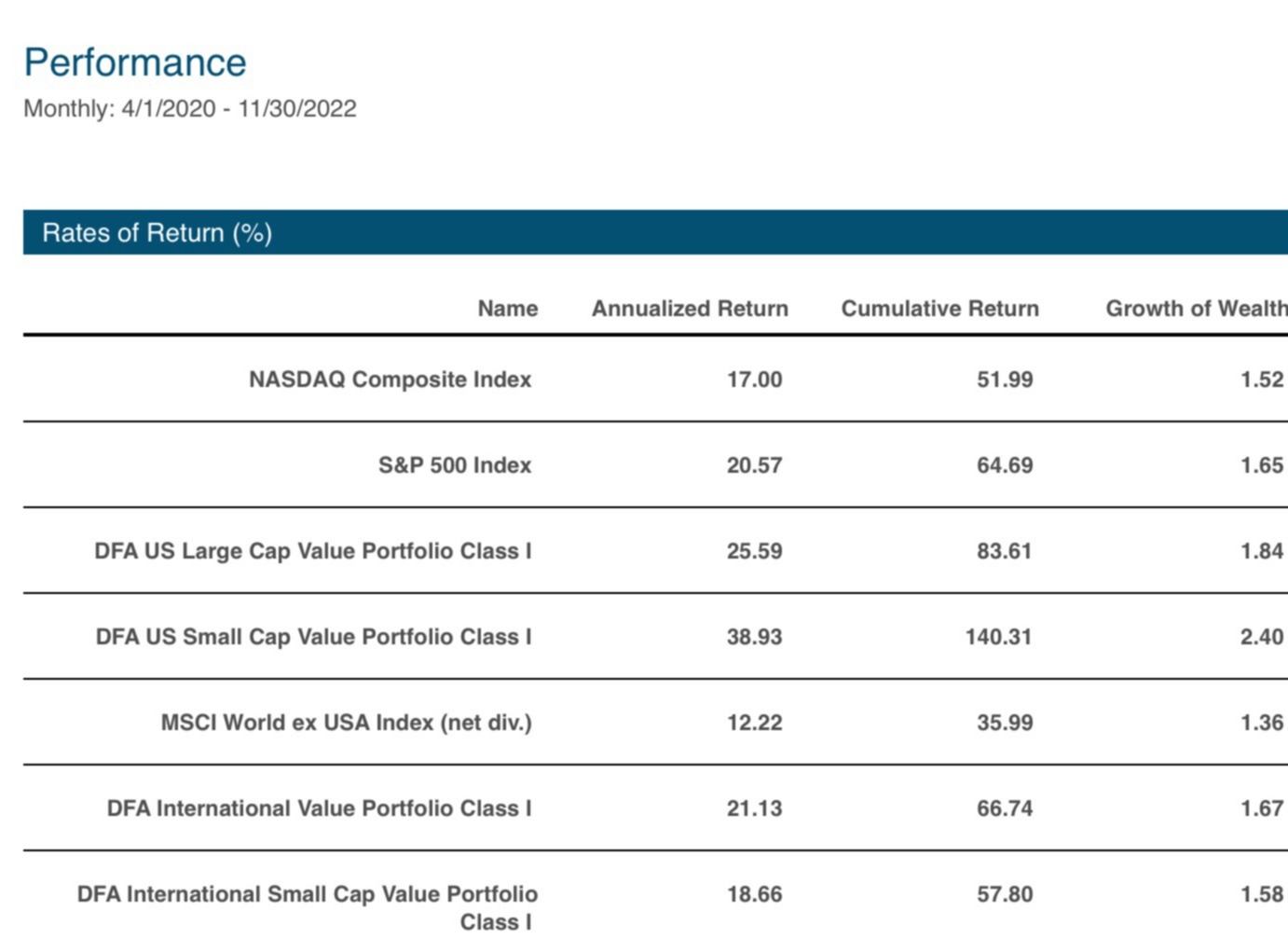

If we look at asset class returns following the brutal stock collapse in 2020, we see the ones that lost the most in the Covid decline have since recovered the fastest. Ultimately, asset-class investors who stuck to their diversified portfolios and maintained a cool head have been rewarded, not just in terms of losing less in 2022. Look at the table below.

From April 2020 through November 2022, the NASDAQ and S&P 500 Indexes are up 52% and 64%, but the DFA US Large Value and DFA US Small Value Funds have come back much faster, with gains of 83% and 140%. While international stocks have continued to trail US stocks, the DFA International Value and Small Value Funds have bounced back more than the MSCI EAFE Index, with 66% and 57% gains compared to just +36% for the index.

So, why is everyone losing so much more in stocks recently? My answer: the market is finally reverting to more normal behavior.

What’s normal?

- We should expect that smaller and lower-priced value stocks will have higher returns than their larger and higher-priced growth stock counterparts or basic index funds like the S&P 500 or Vanguard Total Stock Market Index Fund. Not every year, of course, but on average over time.

- We should also expect that in some bear markets—especially those with rising inflation and higher interest rates (such as 1973-1974 and 2022)—small cap and value stock asset classes could hold up better, too. This was not the case for much of the 2010s, which saw lower returns and more significant declines for small cap and value stock asset classes. As previously mentioned, in response many investors, and even some financial advisors moved their assets to large US growth stocks, and have since paid the price.

Thankfully, there’s a better way to invest, one that Servo implements and manages for clients:

- We start by defining and quantifying your long-term financial goals—too many investors in our experience don’t take the time to figure out what they are investing for.

- Then we design and manage a goals-based, globally-diversified investment portfolio that emphasizes smaller and lower-priced value stock asset classes using the mutual funds and ETFs from Dimensional Fund Advisors (DFA).

- For clients—often in retirement—who are drawing income from their accounts, we also keep a few years of spending in a Dimensional short-term bond fund to weather bear market declines and to help buffer short-term unpredictability.

- Finally, we rebalance your portfolio back to its target weights (as tax efficiently as possible in taxable accounts) to ensure it maintains the desired risk and return profile; this results in a natural “buy low” and “sell high” discipline without trying to guess future market moves.

But these actions aren’t enough. To fully experience the advantages of the Servo approach, you’ve also got to stick with it. The benefits of keeping a cool head aren’t just the expectation of greater wealth, either. You should also have greater peace of mind, worry less about how your investments are performing, how you’re “doing,” or if someone else or some other strategy is “doing better.”

In fact, financial serenity might be the biggest benefit of all.

Past performance is not a guarantee of future results. Index and mutual fund performance includes reinvestment of dividends and other earnings but does not reflect the deduction of investment advisory fees or additional expenses except where noted. This content is informational and should not be considered an offer, solicitation, recommendation, or endorsement of any particular security, product, or service.