You’ve probably heard that Silicon Valley Bank (SVB) folded last week, the 16th largest bank failure in history. Stock prices since have been predictably volatile—down for a few days but up significantly today. First, the practical. A few clients have emailed or texted wondering if we held a lot of SVB stock, if our bonds were ok, and even if they should be worried about their money market accounts. No, yes, and no.

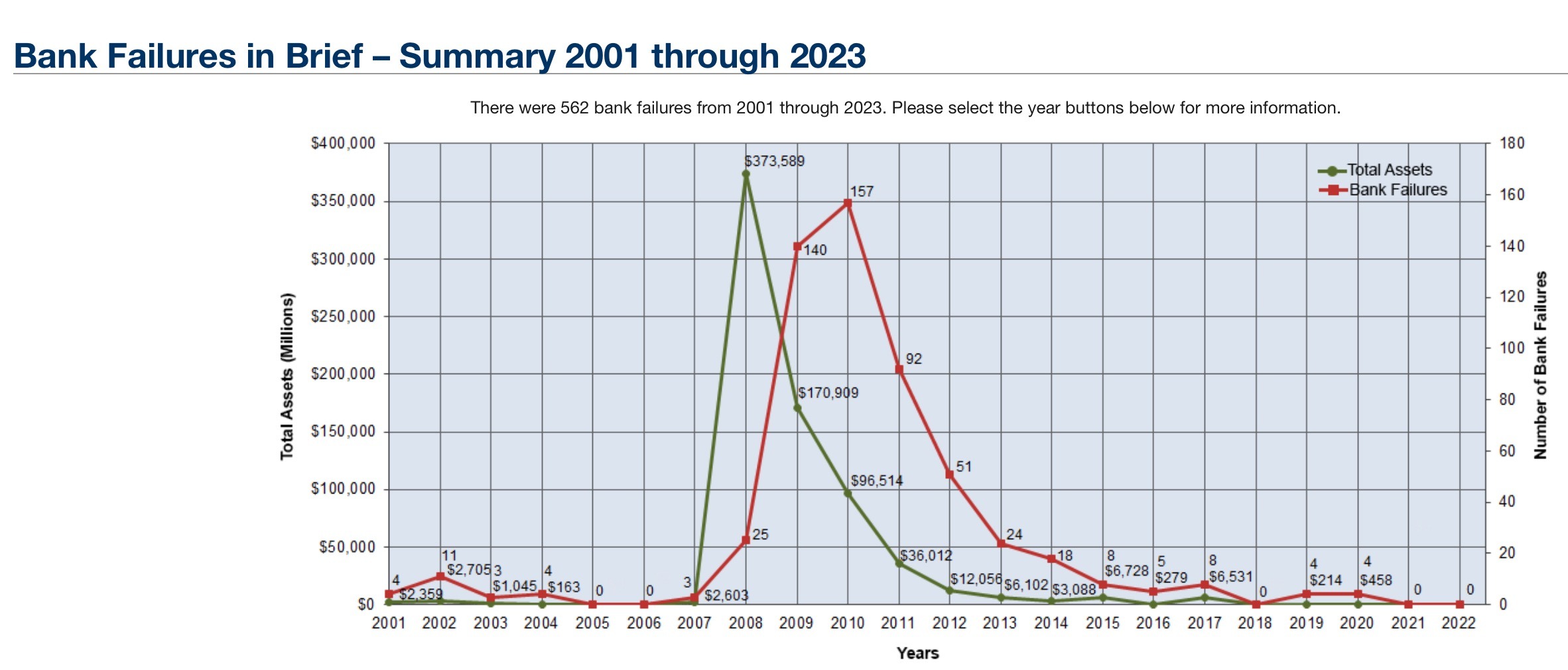

The reality of the SVB situation is that some banks fail almost every year—2021 and 2022, which saw no bank failures, were the exception and not the rule; four of the five years ended in 2020 saw an average of a half-dozen banks fail. When we think of bank failures, our minds immediately return to 2008 and 2009, when 25 and 140 banks failed in the aftermath of The Great Recession. The peak year for bank failures was 2010, when 157 were shuttered. But mentions of 2008 remind us of the worst annual decline (-37%) for stocks since 1931 (-43.4%). Not a fun memory.

Returning to SVB, it’s doubtful we will see anything resembling another 2008 episode of widespread banking panic and a stock market plunge. But that doesn’t mean we should ignore the situation. As I read over the weekend about what happened to a once-thriving bank to send it spiraling, I came across several surprising mistakes SVB made that we can learn from as investors saving for our long-term retirement and legacy goals.

MISTAKE #1–They Took Unnecessary Investment Risk

According to the Wall Street Journal, SVB had just $55B in customer deposits in 2020. But thanks to the vibrance of the tech sector in recent years and specifically the success of countless tech startup customers that the bank catered to, the amount of deposits had more than tripled to $186B at year-end 2022. In other words, they took in a lot of money in a short amount of time.

Normally a bank would lend out some or even most of the new deposit assets they took in, but near-zero interest rates and rising stock prices diminished demand for loans. SVB’s solution? They took these deposits—funds that might be needed for short-term purposes such as withdrawals—and invested them.

When I talk to new and existing clients, and discuss their goals and needs for money, I always separate their long-term needs (let’s say an annual retirement income withdrawal or a goal of X% growth over the following decade) from their near-term obligations. I spoke to a client this morning who asked what she should do with funds she had set aside that might be needed to help her ailing father-in-law over the coming months; my answer was to keep them in the savings account until she needed them or could reassign them to her longer-term savings goals. Sure, the savings account interest rate was pathetic. But the money would be there if needed, which was the most important thing.

Remember: Don’t take risks with money you can’t afford to lose (i.e., short-term funds).

MISTAKE #2–Reaching For Yield

But it was the investments SVB bought that were the problem. Not satisfied with the paltry 0.25% yields on appropriate short-term Treasury securities over the past few years, SVB opted instead for longer-term bonds with higher yield-to-maturities. For example, the WSJ reports that SVB bought over $80B in 10-year mortgage-backed bonds and many longer-term Treasury Bonds as well. Why? Their average yield to maturity was higher, in the case of the mortgage bonds, about 1.5%, or six times the yield on shorter-term debt. Instead of settling for a paltry but safe return that would have matched their near-term liabilities, SVB broke the cardinal rule against “reaching for yield.”

We learn from history that we don’t learn from history.

About 15 years ago, Bear Stearns, Washington Mutual, and Lehman Brothers went under because they had held excessive amounts of bonds with too much credit risk (despite having AAA ratings from the agencies); SVB had gotten in trouble from overexposure to the other bond risk–extending maturities, also known as “term” risk.

Typically, longer-term bond maturities and bonds with lower credit qualities carry higher yields and returns. If your goal is to make the most return possible on bonds and have no concern for near-term accessibility, then longer-term and lower-quality bonds are your best bet (actually, stocks are better, but that’s another topic…)

But if you look at a bond portfolio as a vehicle to reduce the volatility of stocks, or as a lower-risk pool of funds from which you can draw from during stock market downturns, or simply an emergency reserve from which you hope to make a little return, then you don’t have the luxury of holding longer-term maturities or lower-quality issuers. You should stick to short-term and high-quality bonds. Why? Because when interest rates go up, as they sometimes do, bond prices drop, and the longer the maturity, the more significant the decline.

For example, in 2022, when interest rates rose by an unprecedented amount, the Bloomberg Long-Term Treasury Bond Index lost -29.3%, while the shorter-term DFA Five-Year Global Fund lost -6.6%, and the DFA One-Year Fixed Income Fund declined just -1.2%. SVB tried to goose profits by earning excess returns on their investments in longer-term bonds and hoped that interest rates wouldn’t rise and offset the yields. But they got caught with their hand in the cookie jar as some of their returns mirrored the Bloomberg Index’s decline.

Servo clients don’t take the same risks as SVB. Our portfolios divided between stocks and bonds typically favor shorter-term bonds for their added safety and stability. Their lower overall expected returns are simply a fact of life that we address by holding a higher percentage of our long-term savings overall in stocks in general and small cap and value stocks in particular. In more market-like “Core Equity” allocations, it can make sense to hold intermediate-maturity, investment grade bonds, but we will not extend out to longer-term bonds. Unlike SVB, we’ve always known the added maturity risk isn’t worth the potential reward.

MISTAKE #3–Not Admitting Your Errors

Customer withdrawals ultimately forced SVB to sell $21B of their bonds that were underwater, resulting in a staggering loss of $1.8B. This was when the sharks started to circle. SVB had to have known this day was coming. The depreciated value of these bonds had sat on their balance sheet for months; they weren’t a surprise. Or maybe they were; amazingly the WSJ reported that the bank went without a Chief Risk Officer for eight months last year. In effect, the bank was operating as a do-it-yourself investor who had been locked out of online access to their accounts!

But there was still time to fix the situation. SVB could have sold shares of their stock to raise funds and plug the hole created by the bond losses. It was reported that private equity firm General Atlantic offered to buy $500M of the bank’s common stock. But SVB refused to sell.

Unfortunately, a number of prospective clients that I talk to make the same decision. Years ago, I was engaged with a couple who had made tens of millions in technology stocks in the years between 2012 and 2020; I figured that they had a portfolio about $5M greater than if they’d only invested in the S&P 500 Index over the preceding decade (and greater still if they had been globally diversified and tilted to small and value companies). They rode the wave of FAANG stocks to heights they never thought possible in such a short amount of time. My simple advice: count your blessings, sell out and lock in your extraordinary gains at favorable long-term capital gains rates, and redeploy your proceeds into a globally diversified portfolio. They declined.

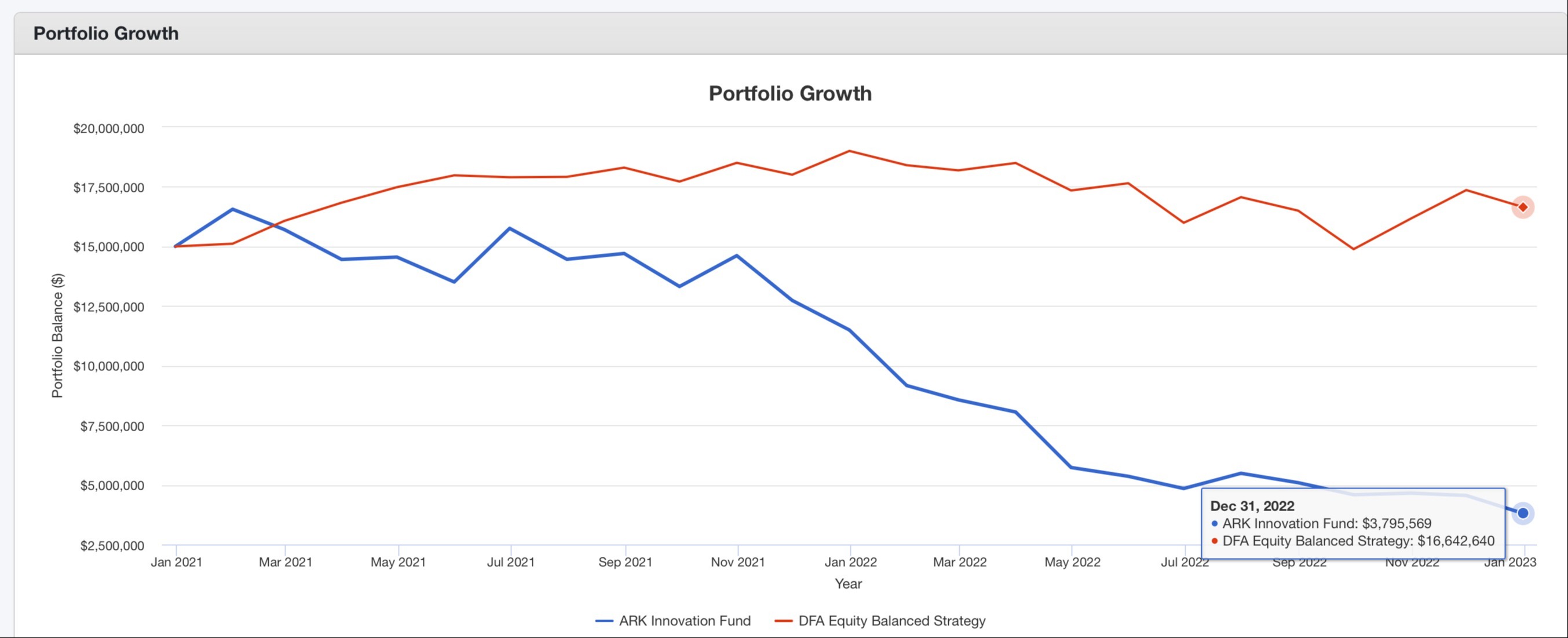

Only two years later, we can look at the likely results these folks experienced from not selling out of their tech-laden portfolio and diversifying. I estimate that their portfolio looked a lot like the ARK Innovation ETF that famously holds all of the well-known tech companies so we can compare the results of $15M invested in ARKK in 2021 to that same amount of money redirected to the well-diversified Dimensional Equity Balanced Strategy, net of an annual advisory fee. What was the difference in ending wealth? About $13M.

From a $16M investment portfolio, you can reasonably expect to withdraw $800,000 annually to live on. Not bad. From $4M? Just $200,000 per year. Those are extraordinarily different lifestyles, and the possibility came down to a simple decision: sell or not to sell.

I tell prospective clients and remind existing clients consistently that successful investing is simple but not easy.

Understand and quantify your long-term goals in a plan.

Adopt an investment portfolio that is appropriate for that plan.

Know that you have to take risk to earn an expected return, but at the same time, don’t take unnecessary risks.

Finally, stick to your plan and your portfolio until your circumstances change.

Where does SVB’s practice of “Investing your emergency reserves in long-term assets to try to eke out a few extra tenths of a percent in gains” factor into this equation? Of course, it doesn’t.

There will be times when sensible, traditional advice will seem out of step or less profitable compared to other approaches. Maybe our stock returns aren’t as high in a NASDAQ bubble. Perhaps our bond funds aren’t earning the excess returns of longer-term or lower-quality bonds in a steeply declining interest rate environment. But that is because this advice is designed not to get you into trouble when you can least afford it.

You don’t need extraordinary returns to achieve your long-term goals; you need to avoid catastrophic mistakes from which you can’t recover from. The lesson from SVB is not to mistake the allure of outsized short-term investment gains for long-term sustainability. As this former Wall Street darling reminds us, it’s easier said than done.

Past performance is not a guarantee of future results. Index and mutual fund performance includes reinvestment of dividends and other earnings but does not reflect the deduction of investment advisory fees or additional expenses except where noted. This content is informational and should not be considered an offer, solicitation, recommendation, or endorsement of any particular security, product, or service.