Happy New Year, and welcome to 2025! After a bumpy December but otherwise good year, it's time to reflect on 2024 for investment markets and our asset class portfolios.

Let me start by asking: What do you expect for 2025? What do you hope will happen to your investments? Let's think about this for a minute.

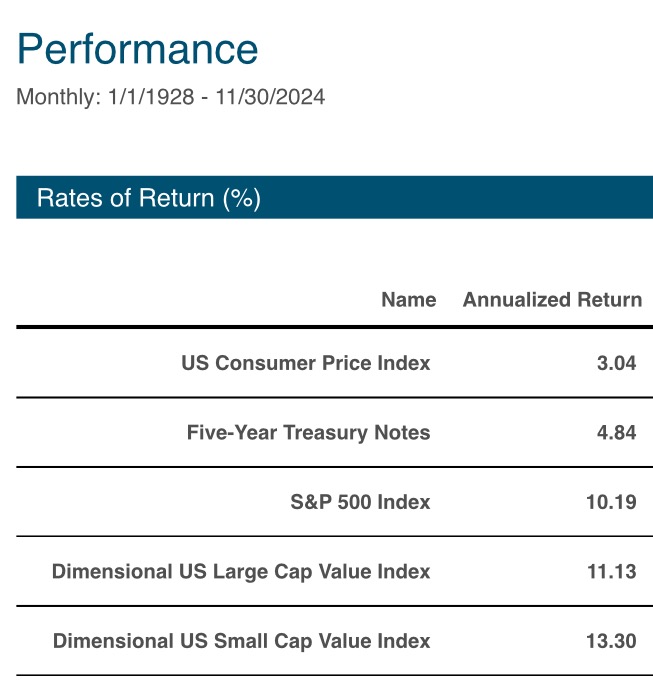

We know over the last 99 years, since 1926, that US stocks (S&P 500 Index) gained slightly over +10% per year. Core bonds, Five-Year Treasury Notes, returned just under +5% yearly. Unfortunately, the range of annual results was all over the map. The worst year for the S&P 500 was -44% in 1931; the best was +54% just two years later. Even bonds had significant high/low spreads. In 2022, Five-Year Treasury Notes lost almost -10%, and in 1982 gained over +29%! So, +10% and +5% are reasonable expectations, but we rarely hit those marks in a given year. These are, in other words, uncommon averages.

If, in 2025, you get a +11.9% return on an all-stock allocation or +10.3% return from a 75% stock and 25% short-term bond allocation (both before Servo Advisory fees of 1%), would you be pleased? Probably, right? +11.9% is almost 2% more than the 10% long-term gain on stocks, and +10.3% is over 1% more than the simple 75/25 stock and bond average of +8.8%. Not great, but good. Especially considering that you avoided losing money, which has historically happened about once every four years (in the last 99 years, the S&P 500 has been negative 26 times and positive 73 times) and occurred as recently as 2022 and before 2018.

Unfortunately, we can't accurately predict what 2025 returns will be, but the numbers cited above are what happened in 2024. So we must admit, last year was good, not great.

Can good be good enough? The most appropriate way to evaluate these returns, always on the portfolio level first, is in relation to your goals. The way we invest, as opposed to so many other investors and advisors, is to rely and plan on historical long-term returns of markets in general and core stock and bond asset classes in particular because that's what we own. In a complex and ever-changing world, we avoid unnecessary added complexity—active management, marketing timing, and opaque alternative strategies that few understand, and even fewer know what to expect. We employ simple (not simplistic), transparent, and focused portfolios. Why? Core developed country stock and short-term bond asset classes have been more than sufficient to fund reasonable long-term goals without all the known and unknown risks that come with other investing approaches.

Returning to the point about evaluating returns, if you're saving for retirement, your long-term return goal from an all-stock portfolio, and what we plan around, is about +10%. We expect 1-2% more from our small cap and value tilts but leave that out of planning estimates. If you're in retirement and spending 4-5% per year and hold a balanced, 75% stock, 25% bond (aka "five years of spending in bonds") portfolio, you'd like to see +7-8% over time with a ride slightly less bumpy than an all-stock mix. Getting an annual return of +1-2% higher than these planning estimates is more than what you need and will only move you closer to achieving and exceeding your goals. Or give you some wiggle room in future years when returns inevitably disappoint. In that sense, and most importantly, everyone begins 2025 better off than we expected to be in 2024.

However, many investors, including some Servo clients, are fixated on individual relative asset class returns. Fair enough. Here, we have less to crow about this year. Maybe subconsciously, I hoped you wouldn't make it to page two.

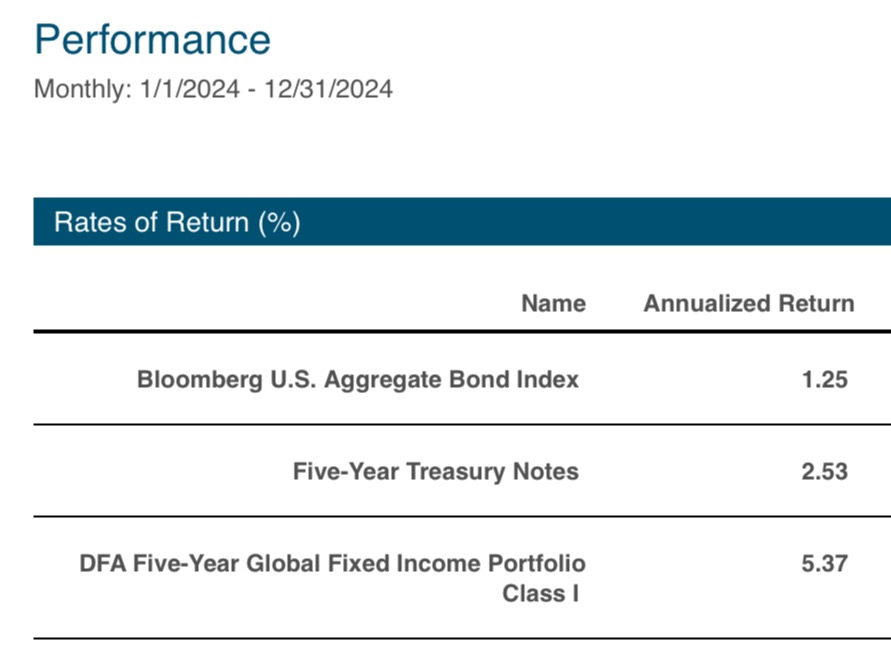

Bonds, as intended, were the boring part of the story. The DFA Five-Year Global Fund came as close as possible to matching the long-term average of Five-Year Treasury Notes, gaining +5.4%. This was a much better relative result than the +1.3% return on the Bloomberg US Bond Index. The fund maintained a very short average maturity of one month, where yields were higher than longer-term maturities, and avoided the dent from rising interest rates that hit intermediate and longer-term bonds harder. As of the end of the year, the fund yields 4.6%, which is very close to the long-term average Five-Year Treasury Note rate (currently 4%). Suppose short/intermediate bond yields continue to rise anywhere in developed country bond markets. In that case, the fund will reinvest back into these longer-maturity bonds (not to exceed five years) if the expected return is worth the additional maturity risk.

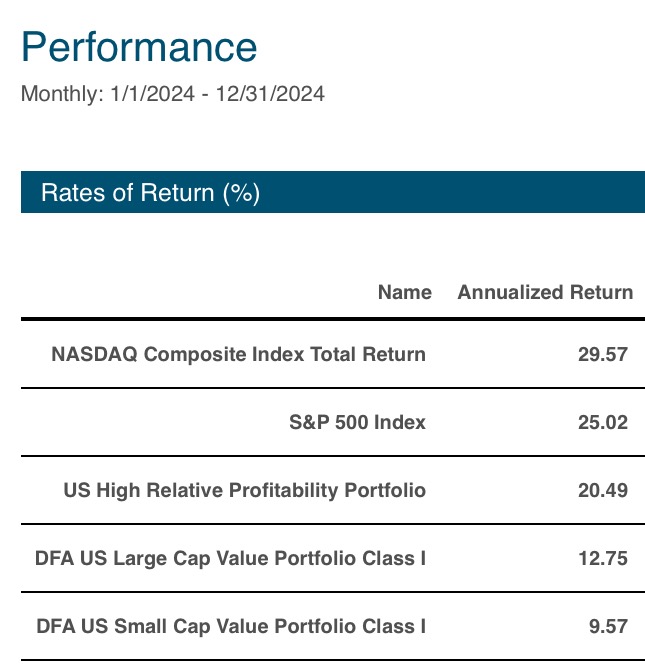

How about stocks? Compared to the technology-dominated Nasdaq Index's +29.7% return, our returns didn't look hot. We lagged even compared to the only slightly-less-technology dominated S&P 500's +25% return. What gives? I blame diversification. The Nasdaq has 55% of its entire index in just seven companies, the Magnificent Seven—Nvidia, Apple, Meta (Facebook), Amazon, Microsoft, Tesla, and Alphabet (Google). The S&P 500 had less in these names, but 34% is still a lot—the S&P 500, by some measures, has never been so top-heavy! These seven companies did exceptionally well last year, returning on average over +60%, while the other 493 names in the S&P 500 averaged returns of "just" +12.8%. So, for most companies, last year was much closer to the long-term average of +10%; these seven tech stocks shot the lights out, and we owned relatively less of them because we're more diversified.

In the long run, diversification should help. Last year, it didn't. Despite 30% of S&P 500 companies losing money in 2024, we had no losers in our asset class lineup. Diversification means you'll never have the absolute best performance, but you'll also avoid the worst returns.

We own the Magnificent Seven, and many of these stocks are top holdings in the DFA US High Profitability Fund, which helped it gain +20.5% for the year. However, none reside in the large or small cap "value" part of the market, given their sky-high prices (compared to their earnings and profits), which hurt our associated funds in these categories. The DFA US Large Value Fund had a completely average +12.8% gain, while the DFA US Small Value Fund had a decent but mildly disappointing +9.6% return.

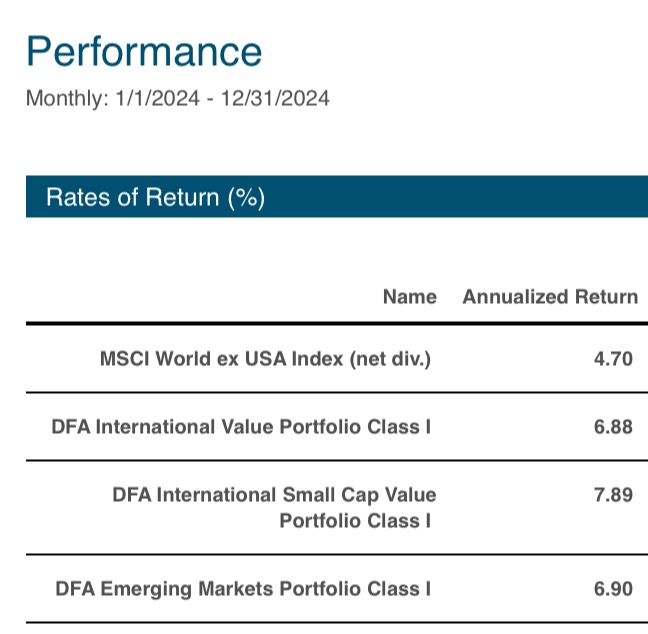

But the real challenge last year came from outside the US. The MSCI World ex-USA Index, the international developed country version of the S&P 500, returned just +4.7%. The companies did better, but because we hold international companies in their overseas currencies (Euros, Yen, etc.) for added diversification, and these currencies depreciated relative to the Dollar in 2024 (even as everyone continues to worry about a crash in the Dollar), international investment returns were lower for Americans. If you held 30% of your stock portfolio in non-US stocks, as we do, it was a noticeable drag on returns.

One interesting observation from international markets was that the growth-stock mania gripping our market is absent overseas. The MSCI World ex-USA Growth Index, full of non-US high-tech stocks and many AI contributors, gained just +2.8% last year. Although not a great total return, on a relative basis, the +6.9% return on the DFA International Value Fund and +7.9% return from the DFA International Small Value Fund was much better and outpaced their MSCI World ex-USA Value and Small Value Indexes. Emerging markets bounced around, as always, but ended just 6.9% higher than they started.

If you're getting frustrated with owning international stocks, I understand. But try to remember—during a period where US stock returns have been well above average, we haven't needed help from foreign stocks. I looked back at all 10-year periods since 1975 when the S&P 500 returned less than +4% per year, and the MSCI World ex-USA Index outperformed the S&P 500 in every single period. International investing has paid off when diversification was needed most. During these periods, international value and small-cap indexes performed significantly better than the general index. I'm not predicting that US stocks will have a bad decade ahead, but I do think we're well prepared with our international allocations if they do.

If you've read this far, you probably hope for some thoughts on the upcoming year. I won't insult your intelligence with a predicted return, prognostications on interest rates, the market's response to the proposed tariffs (that everyone and their brother is already expecting), or any of President Trump's other policies. Those aren't worth the paper we used to print things on.

The best way to prepare for the year is to hope for the best, expect a reasonably good and positive return, and prepare for a temporarily bad result.

You have to expect that sometime in 2025, we'll see a 15% or so decline; it could be a little less or slightly more. Why? That's been the average intra-year decline in every year since 1980 despite a +11% annual return for the S&P 500. It happens all the time. A 15% drop will be normal, with nothing to worry about and nothing to act upon. There is a chance, approximately 25%, that we could see a more significant decline. We see losses of -25% or more (that average almost -30% from peak to trough) once every four to five years. We're two years from the last one, so in no way "overdue," but you can't set your watch to market returns or gains and losses; they're noisy and erratic in the short run. We certainly can't predict or time these declines. Holding on for the eventual recovery is our best option, and take comfort in the fact that they're relatively rare and short-lived.

What will we do if we see a sharp decline? In the spirit of Mike Tyson, who said everyone has a plan till they get punched in the face, we need to plan and prepare to act. If you're saving for retirement, you'll want to dig deep to find more money to add to your portfolio to take advantage of the temporary sale. Tell your friends to start investing or invest more and contact Servo to help if need be (but they don't have to wait for a bear market to call). These are the opportunities that build great long-term returns. If you're in retirement and spending from your portfolio, first, don't panic. You'll be fine. I might stop selling stock fund shares and switch to selling bonds for a while, or if you have a significant cash cushion at the bank that I generally advise against, well, for this narrow swath of time, you were right. So let's use it and turn off portfolio withdrawals, let stock dividends reinvest, and buy more shares at cheaper prices. During this spell, somebody may realize that their goals have changed, and we need to revisit the portfolio and the allocation. More often than not, these suggestions are fear masquerading as planning, so I'll urge you to hold the line unless a meaningful shift is warranted.

This year, I'll keep up on the academic financial research, continue to look for new opportunities (that, unfortunately, don't come around very often), and regularly evaluate our existing holdings. I'll keep your portfolio in balance as we've agreed, and we'll chat occasionally about your progress or anything else on your mind. Expect a new Smarter Investing article about every month and encourage friends to sign up for the email notifications on simplysmarterinvesting.com (aka servowealth.com but easier to remember and spell).

Thank you to the growing group of Servo clients. I continue to appreciate your confidence and trust, and I am thrilled with the strides you and your families have made in the last five and ten years—and, for some of you, twenty years! I expect more of the same in the year and years ahead!

_________________________________________

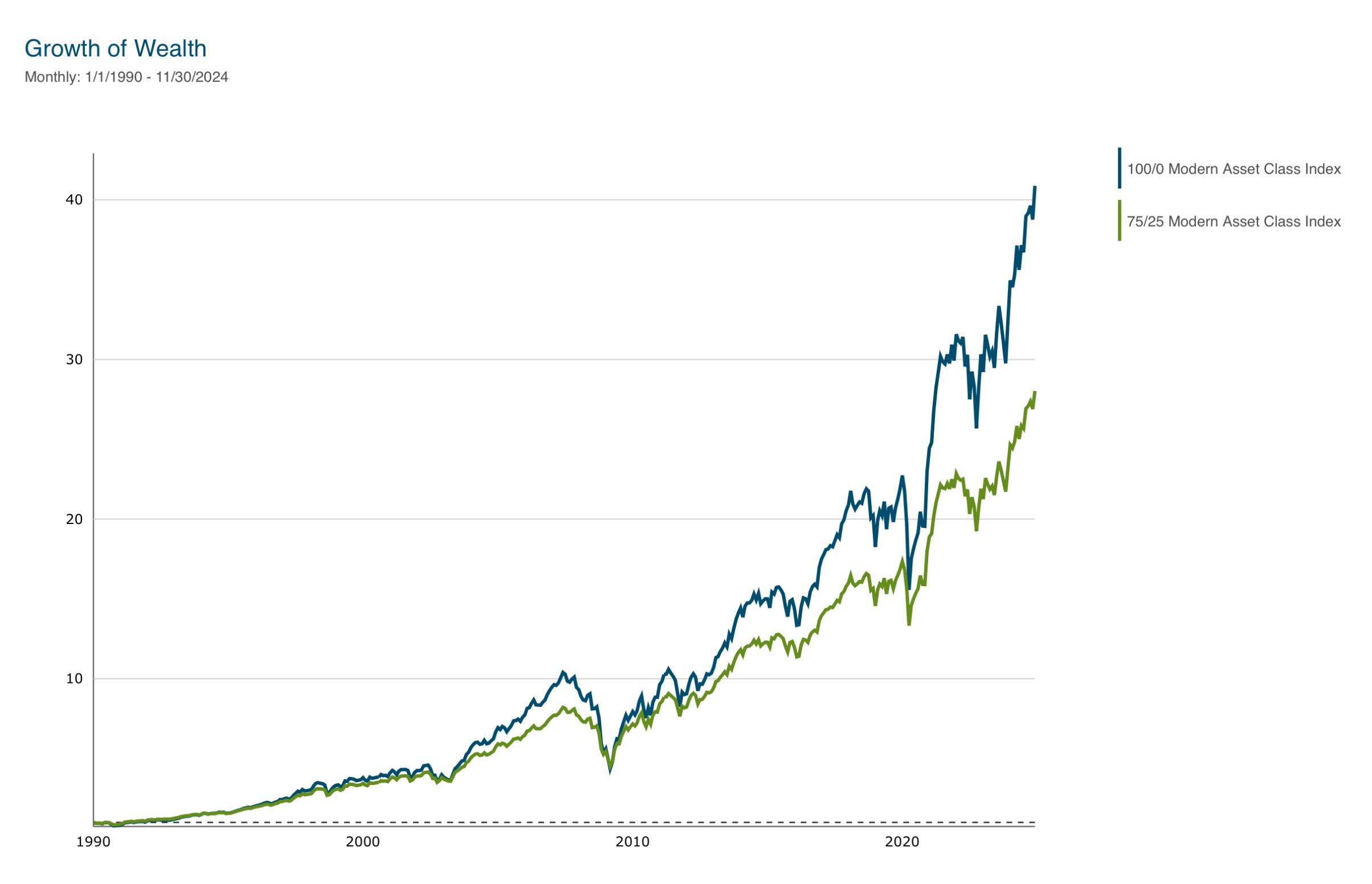

100/0 Modern Asset Class Index = 100% stock, 0% bond allocation consisting of: 21% Dimensional US Large Cap High Profitability Index, 21% Dimensional US Large Cap Value Index, 21% Dimensional US Small Cap Value Index, 18% Dimensional International Large Value Index, 12% Dimensional International Small Value Index, rebalanced quarterly.

75/25 Modern Asset Class Index = 75% stock and 25% bond allocation consisting of: 75% in 100/0 Modern Asset Class Index, 25% in Dimensional Global Short-Term Government Variable Maturity Bond Index, rebalanced quarterly.

Past performance is not a guarantee of future results. Index and mutual fund performance includes reinvestment of dividends and other earnings but does not reflect the deduction of investment advisory fees or additional expenses except where noted. Indexes and mutual funds shown are for illustrative purposes only and may not be the only or any of the funds that Servo clients hold. Servo was not managing client portfolios over the entirety of the periods shown. This content is informational and should not be considered an offer, solicitation, recommendation, or endorsement of any particular security, product, or service.