Have you seen the returns on core stock asset classes over the last 15 years? If not, I have some good news. They've been outstanding.

Since March 2009, higher-priced US large "growth" stocks have soared, thanks partly to a rebound in the technology sector. The S&P 500 Index has gained +16% per year. Lower-priced, large and small US "value" stocks have also done well, albeit slightly worse than the S&P 500, returning almost +15% annually.

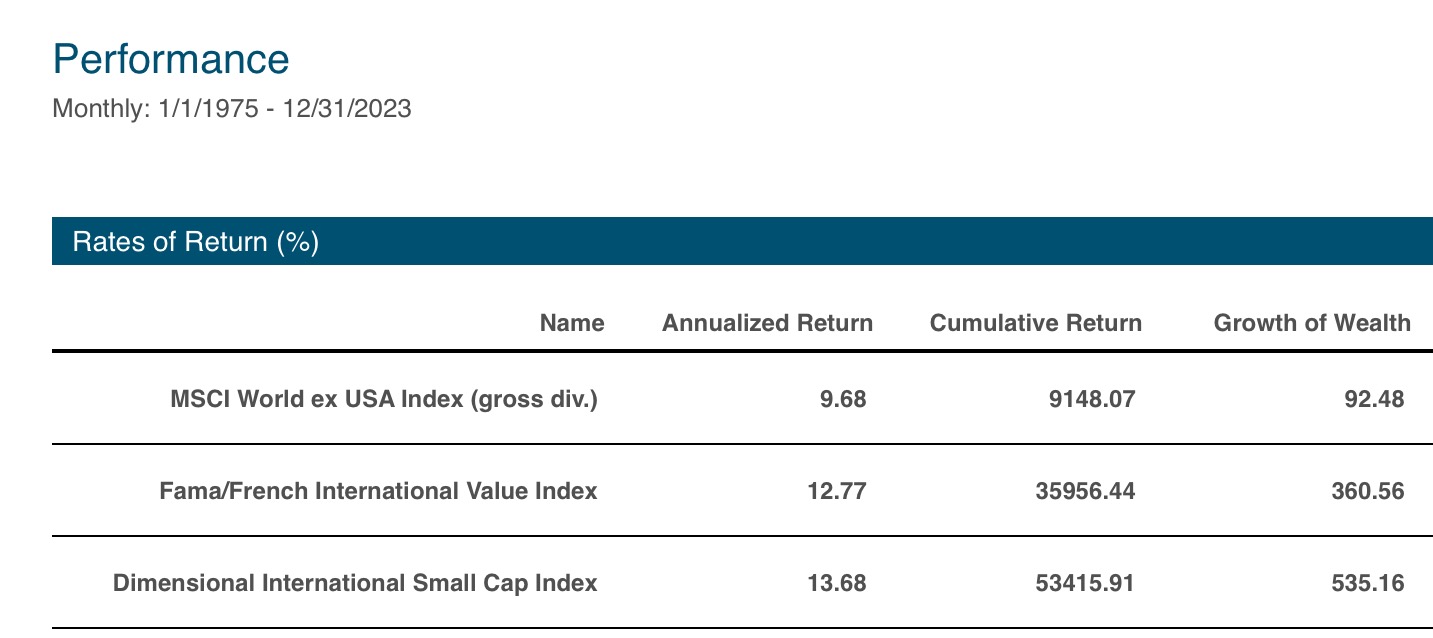

International stocks have been the laggard, but even these returns have been good. The non-US equivalent to the S&P 500, the MSCI World ex-USA Index, returned +8.6% per year, while large and small international value stocks gained +9% to +10% annually.

A hypothetical globally diversified portfolio, the "All-Stock Asset Class Mix," which includes the S&P 500 Index as well as US and international large/small value stock asset classes, returned almost +14% per year. Every dollar invested 15 years ago, excluding advisory fees, is worth close to $7 today. If you've owned stocks and stayed disciplined over the last decade and a half, you're a hell of a lot richer than you were. There's no other way to say it.

Now, I’m sure you’re thinking, let’s hope these good times continue. And that expression gets to the point of my article. Don’t assume we’ll continue to see returns at this rate because it’s unlikely from where we are today. Why?

The last 15 years started at the very bottom of the worst stock decline since the Great Depression. Even as bad as 1973-1974 was, it wasn't 2008-level bad. From mid-2007 through early 2009, all stocks collapsed. For every $ you had invested in stocks in the summer of 2007, you had only $0.45 to $0.50 left by early 2009. More than a few clients still have PTSD from that experience. It's understandable.

Do not ignore the fact that we did recover—just as we did after the Great Depression, the high inflation 1973-1974 bear market, the 23% one-day crash in 1987, and the 2000-2002 tech collapse. We have always recovered—and not by a little bit—recovery returns have been well above average. But we either don't know this or tend to forget it.

The mistake people make during a downturn is to say, ugh, this is really bad, and at average (8-10%) returns, it will take me forever to return to whole. But that's faulty logic. Returns have been "average" only over entire periods, over complete market cycles (a boom, bust, and recovery). During the good times, returns are above average. And immediately after declines, returns tend to be well above average.

Let’s look at this reality through the lens of the periods leading up to and following the 2007-2009 meltdown.

From 1995 (the farthest back we can go with live DFA value mutual fund data) through mid-2007, core stock asset class returns were as good as they've been over the last 15 years. Small cap, value, and international stocks were even better. The S&P 500 Index averaged +12% per year, US large and small value stocks returned a whopping +15% to +17% per year, and international large and small value stocks returned close to +12%. The All-Stock Asset Class Mix returned +14.7% per year, turning $1 into almost $6 before advisory fees.

Next, let's look at just the first five years following the decline from 2007 to 2009. It's another example of what I said above—returns in the aftermath of a significant decline, especially immediately after, are often extraordinarily good, not just average.

You would have been happy with the worst core stock asset class, international large cap (MSCI World ex-USA Index), which returned +17.5% per year. But everything else did better. There was a noticeable small cap and value premium in non-US stocks; large value returned +19.9%, and small value returned +23.3% annually. The S&P 500 also did +23% a year, while US large and small value stocks were unbelievably good—+27.7% and +30.2% annually (no small part of the difficult 2014-2020 period for small cap and value was to make up for this well above average five-year stretch). Finally, the All-Stock Asset Class Mix gained over +25% per year. Every $1 invested in early 2009 became worth over $3 just five years later, before advisory fees.

What about today? Realizing we aren't at the tail end of a bear market, let's close with realistic future expectations. What could you earn on a diversified stock portfolio going forward? The results of the last 15 years? No way. You may get them but don't expect them.

The longest period of historical data is the best estimate of the returns you could see over your investing lifetime. History doesn't repeat, but it tends to rhyme. Or, as Winston Churchill said, "the farther back you look, the farther ahead you can see."

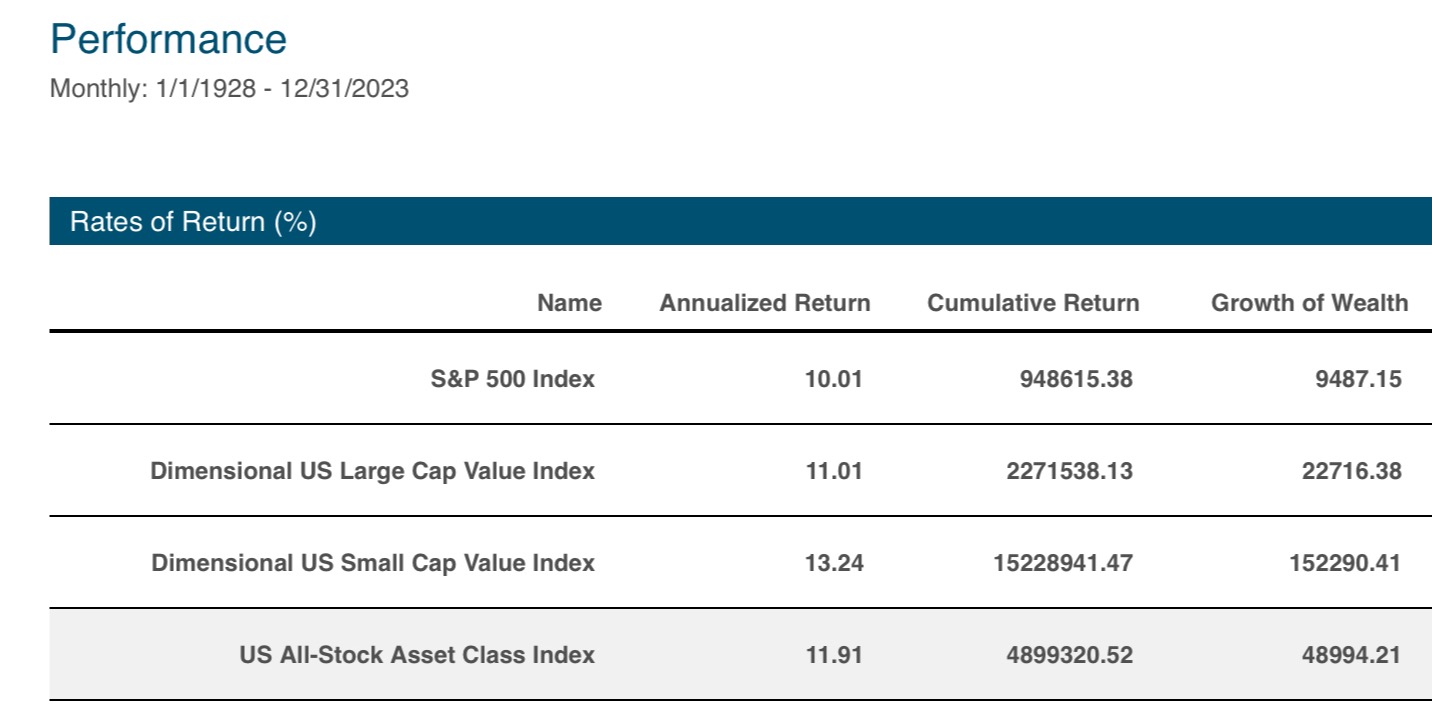

From 1928-2023, returns for stocks (S&P 500 Index) were +10% per year. For large and small value stocks, they were +11% to +13% per year, and a diversified asset class index allocation that includes a balance of all three asset classes did +12% per year. So +10% to +12%, depending on your asset allocation, seems reasonable (historical international stock index returns are listed at the bottom of the article, they’re very similar to US stock index returns).

If you're more pessimistic or worried that US large growth stock valuations are above average and future returns will be lower, use +8% to +10% instead. I might counter that pessimism has rarely been profitable, and international stocks, especially large & small value asset classes, are so cheap today that they could completely offset lower US large growth stock returns. Average historical returns might still be possible when one asset class is richly valued as long as you're properly diversified.

More importantly, you should expect to see shorter periods that are well below +10%. The average intra-year decline for stocks is -15%. That's the price you pay to expect a good longer-term return. About one year in four, -15% could turn into -20% to -25%, and once a decade, you could lose one-third of your stock portfolio temporarily, -35% or more. Finally, once a generation, the wheels come off the investing bus. Losses of -50% or more have happened three times: in the 1930s, 1970s, and in 2007-2009. You may not see another one of these if you're well into retirement. If you're still saving for retirement or newly retired, plan to experience a meltdown that halves your stock portfolio at least one more time.

But be careful reading a -50% decline into every scary, dramatic fall. We all remember March of 2020; talk about falling off a cliff. A -34% decline in 33 days! And then, unexpectedly, stocks turned on a dime. The best 30-day stretch for stocks in decades came in April 2020. Where are we four years later? From the prior top, March 2020 through Feb 2024, stock returns have been excellent. The +14.7% per year return on the All-Stock Asset Class Mix is identical to its return from 1995 through May 2007. This should be a reminder that you can have a good investment return even if the ride isn't always smooth or if it doesn't start off so hot (newer Servo clients, I'm talking to you!).

In summary, remember what got us here. Good long-term returns don't come out of thin air. Above-average returns almost always come from prior periods of below-average returns and painful losses. It's part of investing. It's also why you want to stay the course even when things don't look good—it should get better, but only if you are around to see it. With my help, I believe your odds of pulling this off and having a good long-term investment experience are dramatically higher.

Are you worried you're not investing correctly for your long-term goals, or are you an existing client with questions you want to discuss? Use the "schedule a call" button at the top of this page to set up a time to chat with me.

_______________________________________________

Source of Asset Class Mix and Index available upon request.

Past performance is not a guarantee of future results. Index and mutual fund performance includes reinvestment of dividends and other earnings but does not reflect the deduction of investment advisory fees or additional expenses except where noted. Indexes and mutual funds shown are for illustrative purposes only and may not be the only or any of the funds that Servo clients hold. Servo was not managing client portfolios over the entirety of the periods shown. This content is informational and should not be considered an offer, solicitation, recommendation, or endorsement of any particular security, product, or service.

International stock index data since 1975 inception: