How could I say no?

A group of fellow soccer parents wanted to field an adult, co-ed indoor soccer team. I wasn’t at the get-together when they decided who would play, so I was automatically added as the goalie–a position I played until high school (more on this shortly). I probably wouldn’t have opted in if I was there and had a say, but as behavioral economists and marketers have known for years, it’s as hard to opt out of something that we’ve been auto-enrolled in as it is to sign up for something new.

My wife Caroline thought it was a terrible idea. She was positive that I’d get hurt. She calls me a delicate flower, for good reason; I tend to get injured, a lot. You could say I’m a disaster waiting to happen.

I’ve been running through Achilles tendonitis recently–first the right leg, now the left. Calf strains, backaches, piriformis, I’ve had several ailments over the last few years. In fact, the day before our wedding recently, I was running on the treadmill at the gym, stepped off to get a wipe, and heading back, I walked right into the medal bar of a lateral-raise shoulder machine that a guy had just at that moment begun using. It hit me square in the face, knocked me silly, and I wound up with a huge open gash over my left eye. Not the ideal look for wedding photos.

But none of these, fortunately, compared to the injury I had as a kid, the last time I played soccer.

In ninth grade, I was playing in an indoor tournament and faced a point-blank shot; it came so fast that I only got my hands raised halfway to block it. My index finger took the full brunt of the blast from a kid who would go on to play D1 soccer at Syracuse. Immediately I knew something was wrong; I had seemingly jammed my finger and couldn’t feel or bend it. I tried to press it against the wall, but it wouldn’t move. When blood started to puddle in the palm of my thick white goalie gloves, I knew, as Apollo 13 command pilot Jack Swigert did, that I had a problem. Taking off my glove revealed an open dislocation, a mangled finger three times the size of a normal digit with the upper finger bone sticking out of the index joint with much of the inner finger exposed. My game was over, as was my career. I was off to emergency surgery that night, and a focus on basketball for the rest of my high school and college careers.

So I knew if I were going to play soccer again, something I’d smartly avoided for over three decades, I would have to be careful. I had to watch my fingers and hands, I thought. And, of course, I didn’t want to tear my Achilles or do something to my knees, so I had to watch my legs too. Just for good measure, I didn’t want any more head injuries, so I wouldn’t be participating in any collisions. I was going to protect everything important and that I had ever injured. But it’s never the stuff you’re thinking about that gets you. It’s always the unknowns.

POP.

Almost an hour into a scrimmage I was playing in on Memorial Day, I tried to throw an outlet pass to a teammate halfway up the field, but my bicep had other ideas. I was still playing, but my distal bicep tendon (the one that attaches your bicep to your elbow) had had enough stress for one day. It ruptured and tore clear off the elbow during the throw. I heard that awful sound you hear when you tear a ligament or tendon. I looked down at my right arm, and saw that my bicep muscle had shot up and was bunched in my upper arm and armpit. Not a pretty sight. They call it Popeye arm.

A bicep tear? What. The. Hell. I’d barely heard of such a thing, but now I was living it? It didn’t matter how much I had been prepared and tried to avoid an injury in all the areas I was concerned about. Caroline was right; I’d done it again. But my injury was one I never could have predicted. I’d made that throw thousands of times. Only this time, it did me in.

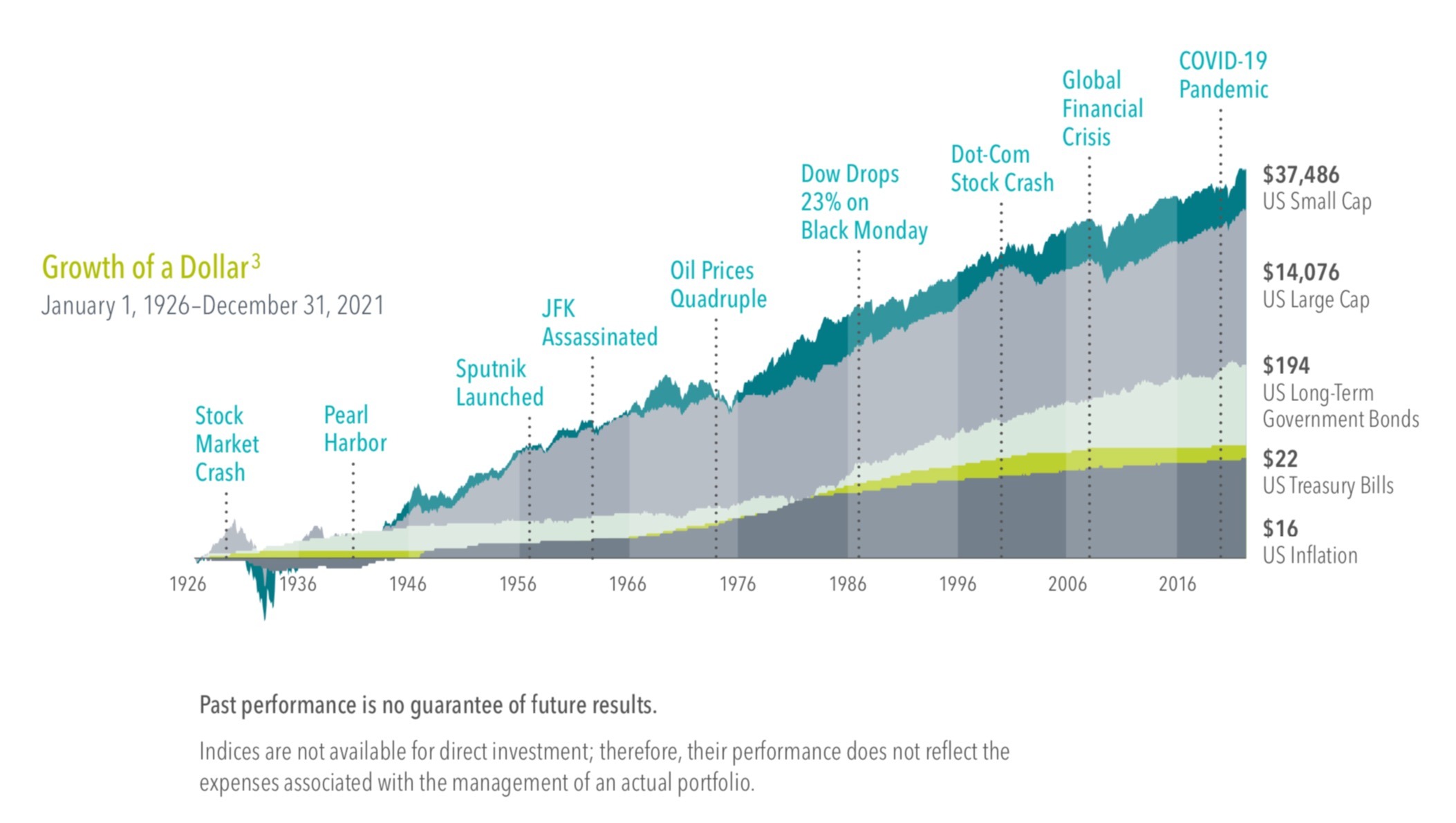

As I’ve been thinking about these events the last two weeks, reminded as I am by the constant drum beat of “I told you so” by you-know-who, I’ve been reflecting on our investment journeys and how much this experience mirrors what we live through. In my last article, I highlighted several difficult and scary experiences from the previous few years: Covid, soaring inflation, the war in Ukraine, etc. All had negative short-term impacts on our portfolios and are things we would have liked to have avoided impacting us financially. But I’ve always told you, we’re never going to be able to predict these situations in advance. One of the most challenging parts of successful long-term investing is coping with the known unknowns: the unforeseeable but inevitable issues that arise and cause us to lose money. In other words, we know that these things happen; we just don’t know what they will be or when they will hit.

Here’s a small sample of known unknowns over the last 100 years. Investment returns have been significant in spite of them.

These known unknowns are bad enough by themselves, but they are often made far worse because we react badly to them. We decide to sell some or all of our stocks before we lose more money and have to wait for what seems like forever to make it back. This turns a temporary setback into a permanent loss. Most of the time, sales are made very close to or at the absolute bottom.

I’m dealing with my bicep tear; I have surgery on Monday and begin rehabilitation later in the month. The hope is that I will have full strength back in time to lift heavy Christmas presents. But the long-term plan is this: I’m officially retired from organized sports. No more soccer games, no more basketball games. Run, lift, walk the dogs, and coach Payton and Tyler’s basketball teams; that will be the extent of my future athletic pursuits. This should go a long way towards preventing my sports unknown knowns.

Unfortunately, you don’t have the same option as an investor. You can’t retire and sit on the sidelines. Even with higher interest rates today, avoiding investing by sitting in cash will cause you to eventually lose all of your wealth to withdrawals, taxes, and inflation. You have to keep playing the investing game to give your wealth the best shot to continue to grow faster than the rate at which Uncle Sam and a rising cost of living confiscate it.

So how should you deal with the unknowns of investing?

First, recognize they exist. Stop thinking that you or someone you can find or hire will be able to predict the future. Enough people are forecasting that in every crisis we learn about someone who was “correctly” warning us. The problem is they typically had been making that warning for many years (and were too early to profit from it), and there’s no evidence that those who forecast one crisis presciently predict future calamities. There is an entire cottage industry of doomsayers, preying on the fact that we are naturally risk averse and we’re more attuned to bad news than good news. The media has for some time operated around the notion that “if it bleeds, it leads.” Don’t play this game.

Next, prepare for the unexpected. How?

Number one: Assume you will need every bit as much, or more, money in the future to maintain your lifestyle than you’ve planned for, and don’t stop trying to grow your wealth. Owning a well-diversified stock portfolio, including large and small, growth and value stocks in US and non-US markets, is the ideal way. We don’t know for sure which asset class will ultimately do best (my money’s on small cap value, of course), but they should all do relatively well over time and help ensure that your long-term growth exceeds the spending, taxes, and inflation hurdles you’ll face.

Number two: Keep aside a sufficient amount of stable investments (such as a money market fund or a short-term bond fund) so that when unpredictable bad things happen, you have the funds to cover your lifestyle until the situation passes. For clients who are still saving for retirement but whose employment is uncertain, or when there is the likelihood of a large future expense, I suggest holding extra cash or as much as 15% in a short-term bond fund. For retirees who are living off their investments, having a few years of spending, sometimes as much as a half decade–which can be 20% to 30%, in a bond fund can give us another bucket to withdraw from when your stock portfolio has dropped by 20% or more.

By preparing for a future where everything is more expensive than you thought it would be, but also for short-term setbacks or emergencies that inevitably arise, you don’t have to be able to predict what will happen. You have the flexibility to adapt to most things when they happen. You won’t avoid the future unknowns; none of us can. But you can ensure that they likely won’t cause permanent harm. As is my hope with my surgically repaired bicep, you might even discover that you emerge from these unfortunate experiences even stronger and wiser than before. On the latter result, I know Caroline sure hopes so.

Past performance is not a guarantee of future results. Index and mutual fund performance includes reinvestment of dividends and other earnings but does not reflect the deduction of investment advisory fees or additional expenses except where noted. This content is informational and should not be considered an offer, solicitation, recommendation, or endorsement of any particular security, product, or service.