2025 was another good year for stocks and diversified portfolios. So you must be wondering what's in store for 2026. Further advances, or are we due for a setback? What's my prediction? What do the analysts think?

Before we go down this rabbit hole any further, let's pause for a reminder: forecasting what will happen to financial markets this year simply isn't possible. You can't do it. I can't do it. Nor can other financial advisors or financial analysts. Why ask a question that we can't answer?

The evidence for my industry's lack of predictive power is obvious when you recall a statistic I cite in many of my monthly articles: "active" (mutual fund) managers don't beat the market. They try to pick stocks and/or time the market, but it doesn't work. What does this have to do with forecasting? Think about it; if the pros knew what was going to happen to stocks and bonds ahead of time, wouldn't they be able to get in and out of the market, or into the right stocks and out of the wrong ones, and significantly outperform a standard index like the S&P 500 that buys and holds a subset of the stock market at all times? I would think so. And yet the vast majority of professional managers don't beat the market or their relevant index (a small cap index for small managers, a value index for contrarian managers, etc.); the index beats them. They fail at forecasting.

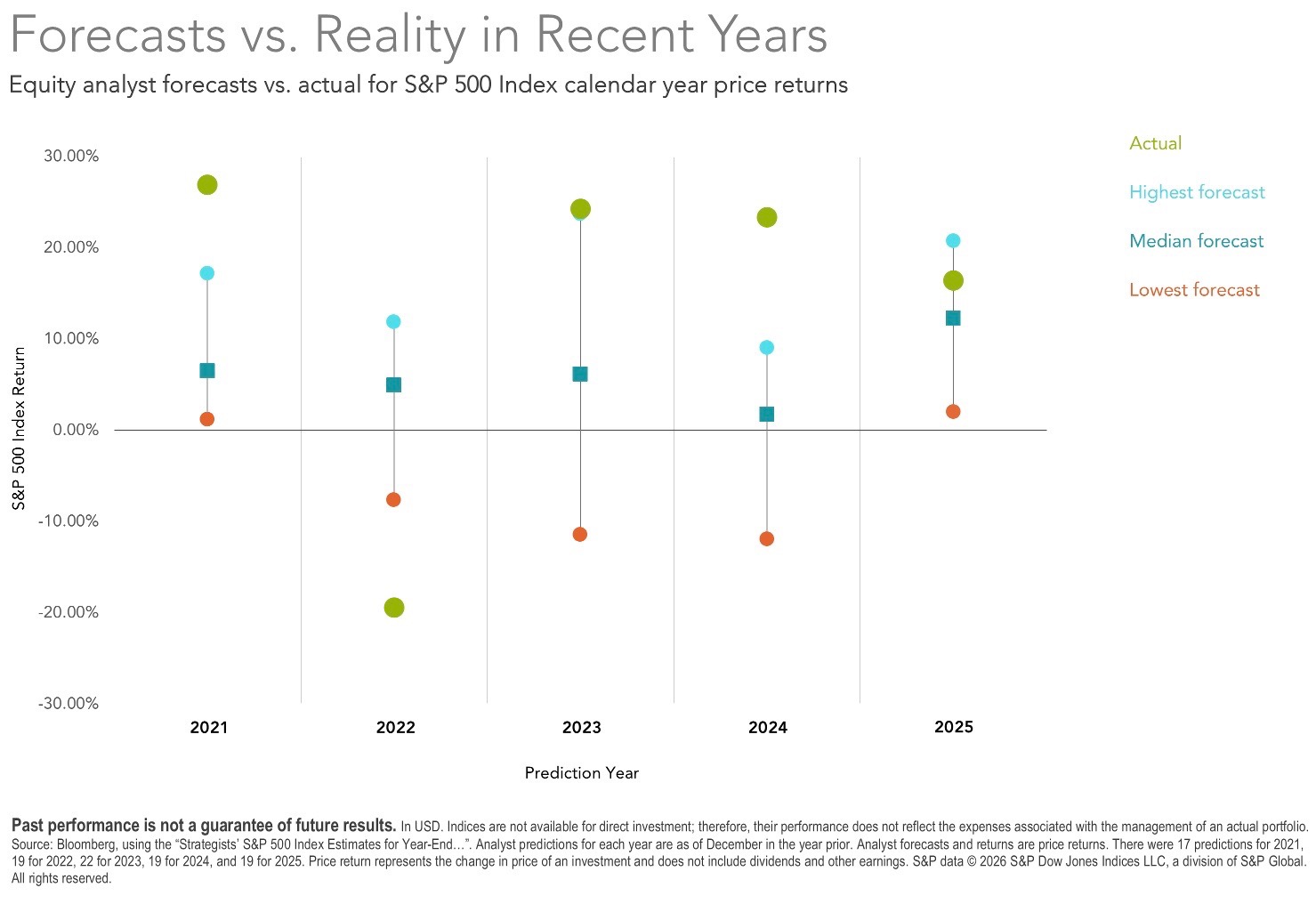

If this evidence isn't enough—although it should be—let me include one more example. Bloomberg tracks published Wall Street market strategist predictions for the S&P 500 every year. Looking at the five years from 2021 to 2025, they found that only once in four positive years did a single strategist predict how well the S&P 500 would perform, and in the single down year (2022), no one predicted how poorly it would perform. Just guessing that the index would earn its average annual return of +12.3% every single year—blind extrapolation—beat the experts in three out of the five years. This stretch, like so many others, found that historical average returns didn't repeat. But the long-term average was closer to what actually happened than everyone's guess about how they'd differ. Historical results are to investing what climate is to weather expectations.

If we can't predict what will happen in 2026, does that mean we should stick our heads in the sand? There are worse approaches, for sure, as long as you have a good portfolio that aligns with your goals. But there is one better approach. You could develop a reasonable, rational range of expectations for what could happen, based on the long-term evidence of what has happened—the investment version of climate.

Setting investment expectations lacks the precision and prescience of a forecast, which is why the approach isn't more common. But when results deviate from what we hope will happen, knowing that we've seen extreme periods before and that this time isn't different can help you stay calm and disciplined and avoid an irrational response to an uncomfortable market—keeping a level head when investing is the key to earning the long-term returns you need.

What, then, should our expectations be for 2026?

Expectation #1—Anything But Ordinary

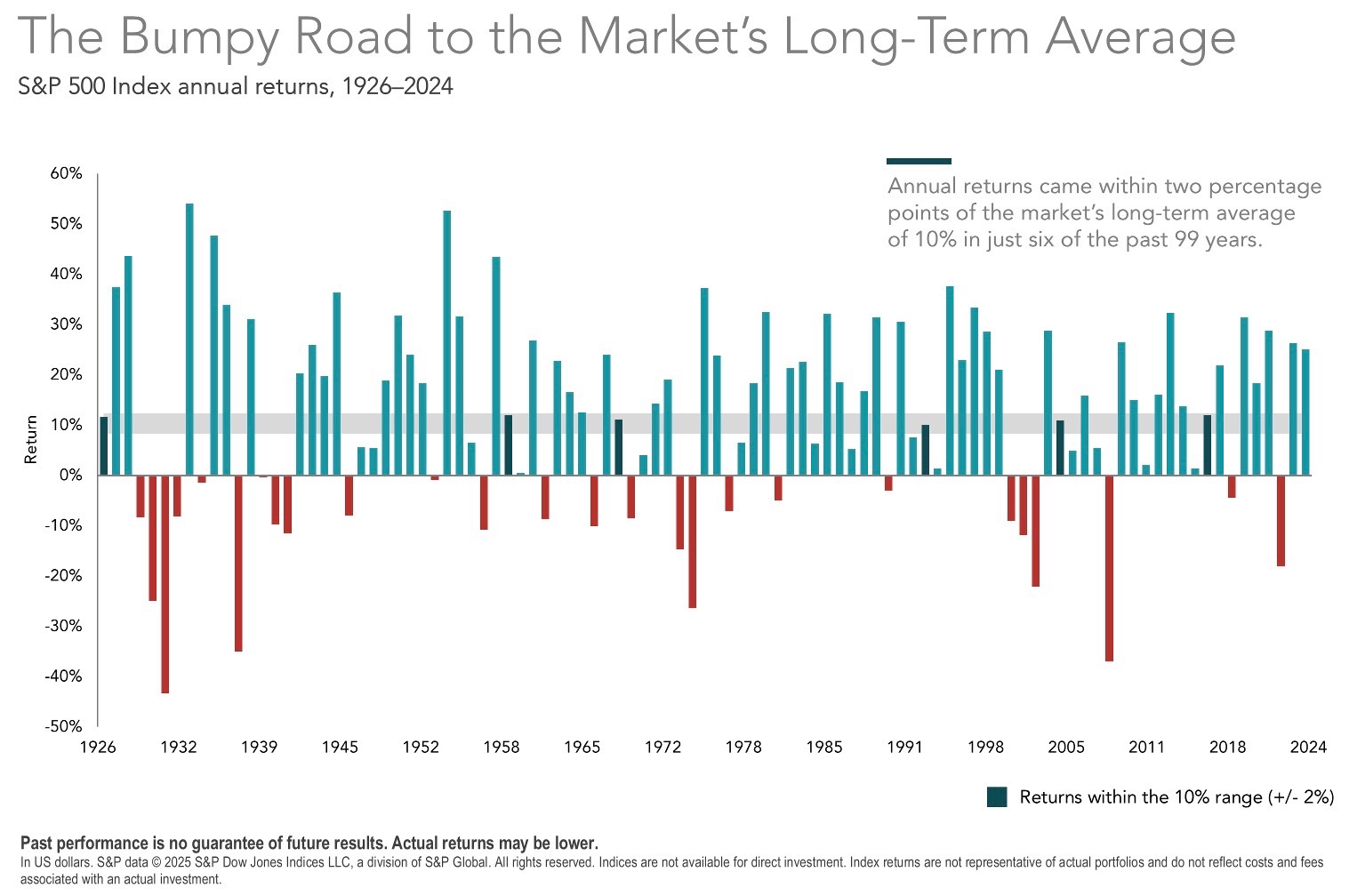

Over time, large cap US stocks have averaged 10% per year (and bonds about 5% per year). US large and small value stocks earned even higher returns, about +11% and +13% per year, respectively. Those are good long-term targets for your portfolio. But rarely do stocks return their average return in any given year. From 1926 to 2025, the S&P 500 Index was within +/- 2% of its long-term average only 6 times! The other 94 times, it was meaningfully above or below its average. The best year was a 54% gain, the worst year was a 43% loss. Don't expect ordinary, be prepared for extraordinary.

Expectation #2—Turbulence Is Typical

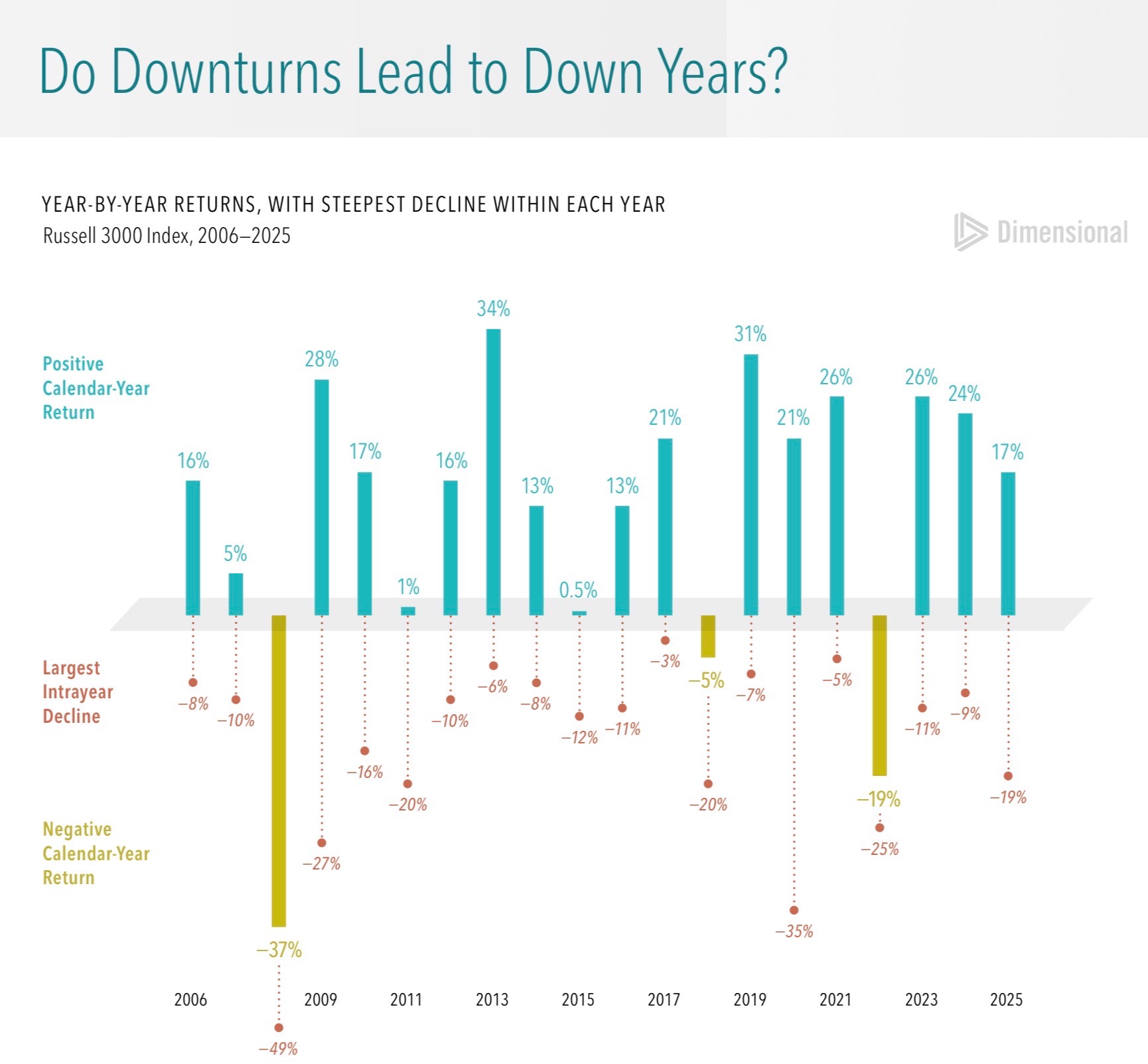

The majority of years are positive for stocks. From 1926-2025, the S&P 500 earned a positive return 75 times and a negative return just 25 times. Three-quarters of the years were positive, just a quarter was negative. But that doesn't mean stock returns are always positive throughout the year.

The average intra-year decline for the S&P 500 since 1980 has been almost -15%. Double-digit declines at some point in the year are not just possible; we should expect them.

But significant intra-year declines don't guarantee a negative year. In the chart below, for example, we see a temporary 19% decline in 2025, but stocks finished up +17% for the year. In 2018, we saw a -20% decline, but the year was -5%. 2022 experienced a -25% intra-year decline and finished down -19%, 2020 had a -35% intra-year decline but was +21% for the year. What happens during the year doesn't correlate with how things turn out.

Stocks will experience a sizable drop at some point in 2026; you can bet on it. We don't know when, how far up we are when it hits, or how long it will last. That's why we don't want to react to the declines, except to add more funds to your portfolio if they're available, and rebalance from bonds to stocks if you own fixed income and the decline is deep enough.

Expectation #3—Higher Expected Returns Don't Always Happen

I've primarily been referring to the S&P 500 Index in my examples above. But we hold other stocks beyond US large cap growth companies—such as large and small cap value stocks—for added diversification and higher expected returns. However, just because we expect higher returns doesn't mean we always get them.

From 1928 through 2024, the S&P 500 Index compounded at +10.2% per year, while the Dimensional US Small Value Index compounded at +13.1% per year. That's a sizable spread, so you might be surprised to learn that small value stocks underperformed the S&P 500 in 43 of the 97 years, or 44% of the time. On a year-to-year basis, the odds that our small value stocks outperform the market are only a little better than a coin flip.

Short-term small value performance can be discouraging, so also realize that the reason you want to stick with your small cap value allocation is that the good years tend to be really good, while the bad years are only marginally bad. There have been four years when the S&P 500 outperformed small value stocks by more than 20%, but 21 years when small value stocks outperformed the S&P 500 by more than 20%.

Whatever happens between large cap and small value stocks next year, don't expect their relative performance to be close. In 58 of the 97 years (about 60% of the time), their returns were at least 10% apart. That's diversification working, whether you like it or not.

Diversification doesn't always help the overall portfolio, either.

We know that an asset class portfolio that holds US and international developed market stocks, across large and small, (profitable) growth and value stocks, has a different profile than the large cap domestic companies in the S&P 500. But we sometimes forget that this will naturally lead to different short-term returns, even if it's a far better approach in the long run.

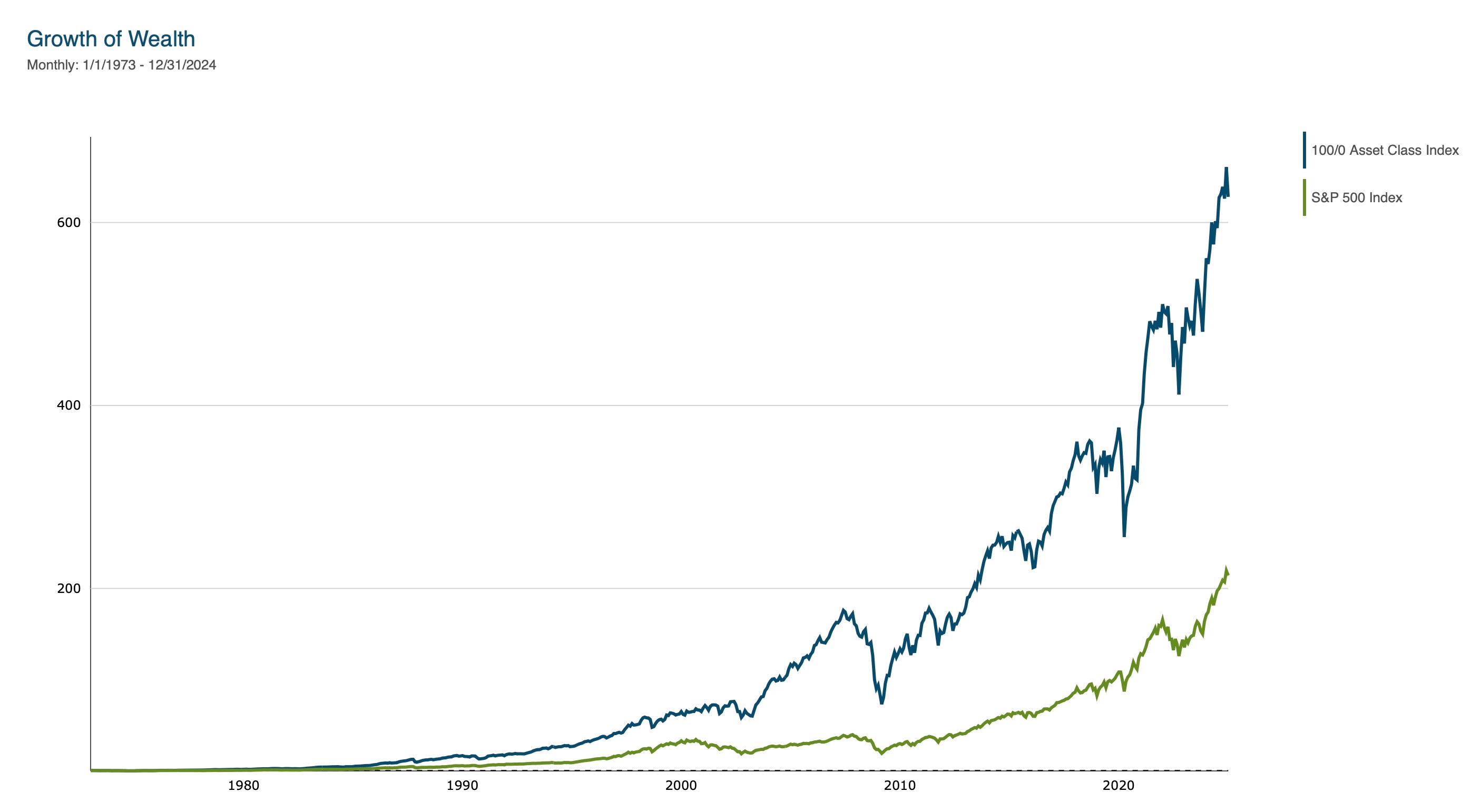

International stock data extends back to the early 1970s; we can compare a globally diversified, all-stock asset class index to the S&P 500 from 1973-2024. Over this period, the Asset Class Index returned +13.2% per year compared to +10.9% for the S&P 500 Index (+10.4% for a 70/30 mix of the S&P 500 Index and MSCI EAFE Index).

But the Asset Class Index underperformed the S&P 500 in 22 of the 52 years (42% of the time). Double-digit differences in returns between US large cap stocks and a balanced, globally-diversified portfolio are common—the S&P 500 outperformed the Asset Class Index by more than 10% in a year five times, and the Asset Class Index outperformed the S&P 500 Index by more than 10% on 13 occasions.

Shifting Your Money Mindset

What should we expect for 2026? Even if our stock portfolios earn +10% or +12%, as our asset class indexes have done for almost 100 years, the odds of getting that return this year are small; it will either be much better or significantly worse. And whether we're up or down, we'll definitely see a sizeable temporary decline along the way, likely at least -15% at some point. Finally, our approach might not outperform the S&P 500 Index. We own different types of companies, and while their long-term justification is sound, their short-term results aren't always pleasing.

But remember this as the year progresses--you're not going to reach your goals in 2026. However, you might compromise them if you make the wrong decisions. Achieving your savings targets, or enough retirement income to last the rest of your life, takes years and decades of discipline and good investing decisions. But one or two mistakes in any year could cost you substantial missed returns, leaving you short. The ruthless reality of long-term financial success is this: It takes years for effective compounding to work, but only a few seconds of mistakes to devastate you.

Don't let 2026 be the year that trips you up. The best expectation you can have, and the best goal for the year, is that your portfolio on December 31st looks exactly like it did on January 1st, continuously held, in the same proportions the whole time. Whether you made progress or not, achieving this goal will ensure you're still on the right long-term track. Make it your goal this year not to interrupt the compounding.

___________________________________________

Asset Class Index = 21% S&P 500 Index, 21% Dimensional US Large Value Index, 28% Dimensional US Small Value Index, 18% Dimensional International Value Index, 12% Dimensional International Small Value Index, rebalanced annually.

Past performance is not a guarantee of future results. Index and mutual fund performance include reinvestment of dividends and other earnings but do not reflect the deduction of investment advisory fees or other expenses, except where noted. Indexes and mutual funds shown are for illustrative purposes only and may not be the only or any of the funds that Servo clients hold. Servo did not manage client portfolios for the entire period shown. This content is informational and should not be considered an offer, solicitation, recommendation, or endorsement of any particular security, product, or service.