When I first started using DFA mutual funds to invest client portfolios over 20 years ago, it was with a specific purpose. After giving up on trying to pick stocks and time the market (“active management”) in the early years of my career, I discovered the “Three-Factor Model” of investing—which was unheard of at Wall Street brokerage firms but was the gold standard of investing theory inside the halls of academia—and I wanted to use it to manage client portfolios.

The Three-Factor Model says that the long-term return of an investment portfolio is related to its overall stock/bond split, as well as its allocation to small stocks versus large stocks and lower-priced “value” versus higher-priced “growth” stocks. No market timing, just three major asset allocation decisions coupled with disciplined rebalancing.

The only question I had was which funds I should use. There were index funds from Vanguard and Charles Schwab that allowed me to invest in small cap and value stocks, but mainly in the US market (non-US options were and still are sorely lacking). I also noticed that traditional small cap and value index funds didn’t own the smallest or cheapest stocks, where expected returns were highest. These style-based index funds were watered down, holding too much in mid cap stocks and “blend” (between growth and value) companies. If I was going to use the Three-Factor Model, I wanted to do it right.

This is where DFA came in. I had learned about the company in my research on investing and was intrigued that the original academics who published the Three-Factor Model—Eugene Fama at the University of Chicago and Ken French at Dartmouth—were consultants at a mutual fund company called Dimensional Fund Advisors. One of Fama’s former students, David Booth, had co-founded Dimensional as an investment management company that would apply the findings from academic research to the management of real-world portfolios. Dimensional was the only firm in the industry offering products to implement the Three-Factor Model.

DFA funds weren’t watered down. If anything, they were high octane—they went right at the market’s small cap and value segments and delivered a full dose of their returns. When small cap and value stocks outperformed the market, as they usually do, DFA funds had much higher returns than actively-managed funds and even index funds with similar-sounding names (ie, small cap or value). This is exactly what I wanted—style-pure funds allowing me to design portfolios with the utmost precision.

But this focus that DFA offered came with a potential drawback. What would happen during the inevitable (but unpredictable) periods where small cap and value stocks underperformed? Would DFA funds do far worse than their indexes? And would clients stick around through the underperformance, or would they follow the well-trodden path of selling lower and buying higher elsewhere? If DFA were a one-trick pony, only doing well when small cap and value stocks outperformed, a more moderate approach with lower but more consistent returns would be better for clients.

Fortunately, these concerns about DFA funds were unwarranted.

The table below reports the last 20 years of returns for serveral of DFA’s oldest stock mutual funds compared to their most appropriate index. The previous two decades are noteworthy because while stocks have done reasonably well despite numerous setbacks, we have not seen overwhelming small cap and value return premiums. Yet DFA funds have almost all outperformed their specific indexes and the broad market indexes. In other words—no premiums, no problem. DFA funds still managed significant outperformance, and the impact on the hypothetical growth of $100,000 was sometimes enormous.

Let’s look a little closer at the data. The returns for the S&P 500 Index (US large growth), the Russell 1000 Value (US large value), and Russell 2000 and 2000 Value Indexes (US small cap and small value) are listed first. The S&P 500 Index outperformed every other index, meaning large cap and growth stocks had the best returns; small cap and value the worst. And yet the DFA US Large Value Fund, US Small Cap, US Micro Cap, US Targeted Value, and US Small Value Funds ALL outperformed their indexes and the S&P 500 (except DFLVX, which was just 0.2% behind) as well. Who says you can’t get blood from a stone?

In international markets, the MSCI World ex-USA Small Cap Index beat the World ex-USA Index, but the value versions of the large and small cap indexes only matched or underperformed. So small beat large but value did not beat growth. No matter—every single DFA international fund beat its index and the MSCI World ex-US Index, and the DFA international value funds even outperformed their own blend funds (DFIVX beat DFALX and DISVX beat DFISX).

Finally, emerging markets. The MSCI Emerging Markets Index (large cap) had the same return as the EM Value Index (no value “premium”), while (not shown) the MSCI Emerging Markets Small Cap Index did a bit better than the large cap index, returning +10.0% per year. Each DFA fund did far better. Of note, the DFA Emerging Markets Value Fund returned +10.5%—a significant amount of value outperformance where none seemed to exist according to MSCI, and the DFA Emerging Markets Small Cap Fund beat the MSCI EM Small Cap Index by +1.5%, and the large cap index by +3% per year.

Even DFA’s Real Estate Fund outperformed the DJ REIT Index despite holding virtually identical companies.

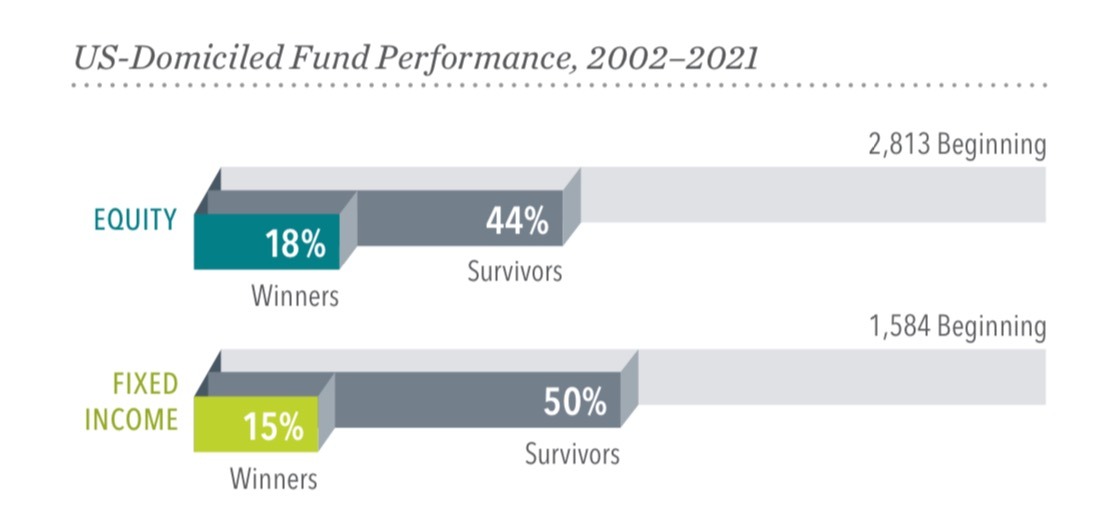

I will compare these results to the overall mutual fund industry to understand how astonishing these results are. Over the 20 years from 2002 to 2021, only 44% of all US stock mutual funds available to invest in survived the entire two decades. Over 50% of them did so badly that they were closed down. And of that 44%, less than 20% outperformed their index. Compare that to the Dimensional table above—of the 14 funds listed, two tied their index (they are indexes), and the other 12 outperformed. That’s 100% survival, 86% outperformance, and 14% ties.

Wow.

So DFA funds are anything but one-dimensional; exceptional is a far better description.

While DFA’s funds tend to capture more of the small cap and value premium returns when those stocks perform best, that’s not the whole story. The benefit of owning DFA funds goes beyond intelligent construction. Their funds are updated periodically as the research on investment returns evolves—most recently, the addition of profitability as a (fourth) factor has made a big difference. And unlike index funds, whose holdings are only refreshed once or twice a year, Dimensional manages their funds and rebalances them (usually with cash inflows or outflows from the portfolios) every single day so that they stay consistently focused on the subset of the market that they are designed to own. DFA’s performance relative to the rest of the mutual fund and exchange-traded fund industry has been extraordinary. I know of no other firm that comes close.

I talked with a long-time client last week and showed him this report. His family has invested with me this entire time. I felt pride in the fact that, two decades ago, I had proposed this approach to him even though it was relatively unknown and he and his family were unfamiliar with it. Like other clients I had and still have today, he trusted me to do the right thing for his family. And I trusted Dimensional to do what they said they would do: Stay focused, stay disciplined, and deliver the expected returns we thought were possible.

Two decades later, Dimensional has more than lived up to my expectations, and we have more wealth because of it. 100% of my personal and family money is invested in DFA funds, which is why I recommend the same for you.

Past performance is not a guarantee of future results. Index and mutual fund performance includes reinvestment of dividends and other earnings but does not reflect the deduction of investment advisory fees or additional expenses except where noted. This content is informational and should not be considered an offer, solicitation, recommendation, or endorsement of any particular security, product, or service.