The last ten years have not exactly been a walk in the park.

You might remember some of what’s happened, but probably not the whole story. We’ve seen several stock declines, the highest inflation rate since the 1970s, and a significant increase in interest rates. Suppose I had told you a decade ago what we were in store for. I bet you might have considered making significant investment changes, especially if you were about to retire and start living off your portfolio.

Let’s start by reviewing some of the challenges over the last decade.

First, the declines.

A diversified stock asset class portfolio like the one we own has had three negative years since 2015. Looking more closely on a month-to-month basis—as clients often do—stocks fell by more than 10% on four different occasions. They dropped -31% in the first quarter of 2020, -18.7% from January through September 2022, -17.4% from February to December 2018 (capped off by the worst decline on Christmas Eve in history), and fell -15% from June 2015 to February 2016. Of course, we recovered each time, and it never took more than nine months to return to all-time highs.

It wasn’t just the setbacks that made the last decade a challenge for equities. It’s also been a lopsided stock market, favoring big US companies with higher prices. The S&P 500 is up over 13% per year for the decade through September, 30% more than its long-term average of +10% per year. Cheaper US large and small value stocks have done OK but underperformed the S&P 500. The DFA US Large Value and Small Value Funds returned +9.1% and +9.4% per year, below the long-term asset class averages of +11% and +13%. International stocks have been more disappointing—the MSCI World ex-US Index gained just +6% while the DFA International (Large) Value and Small Value Funds returned +5.7% and +6.2%. Beyond the frustration of diversified portfolio underperformance, it’s hard to imagine getting ahead with such muted, mostly single-digit gains in core stock asset classes.

Next comes inflation and interest rates.

After a decade of consumer price increases of just 1.7% per year—below the long-term trend of +3%—we saw inflation rise by 7% in 2021 and another 6.5% in 2022. In fact, for the 12 months ended June 2022, inflation rose by 9.1%, almost a double-digit increase. Things were getting noticeably more expensive by the month, and even as the rate of inflation has slowed, the growth is now on top of much higher levels than just a few years ago.

When inflation spikes, we can expect interest rates to follow. And they have. Starting from historically low levels in 2020, the yield on a Five-Year Treasury Bond rose from just 0.27% in September 2020 to 4.56% by April. Remembering that bond prices go down when rates go up, how bad was it for bonds? Even our short-term DFA Five-Year Global Bond Fund declined -9.2% from August 2021 through September 2022 (but has fully recovered). This temporary loss far exceeded its prior record decline of -7% in 1994. But the real bond carnage happened in longer-term bonds, which we smartly avoided. The Vanguard Long-Term Treasury Bond Fund declined a whopping -45.3% from August 2020 through October 2023 (through September 2024, the fund is still down over 33% from its August 2020 level). How bad is this loss for long-term bonds? Consider that the worst stock bear market of our lifetime, 2007-2009, saw the S&P 500 Index fall -51%. Who would have thought you could lose as much in bonds as in stocks?

Is your financial plan screwed?

Having read this, if you’re still saving for retirement, you might think all of this has worked in your favor. Stock volatility allows you to put some of your systematic savings in at temporarily lower levels, increasing your long-term returns when prices recover. Higher bond yields will eventually help you in retirement. You’d be right on both counts.

But what if you retired ten years ago? Are you in trouble? What if you’re retiring today and you’re worried about a repeat of the last ten years? Would it be better to hold off on retiring for a few years?

Hypothetical time.

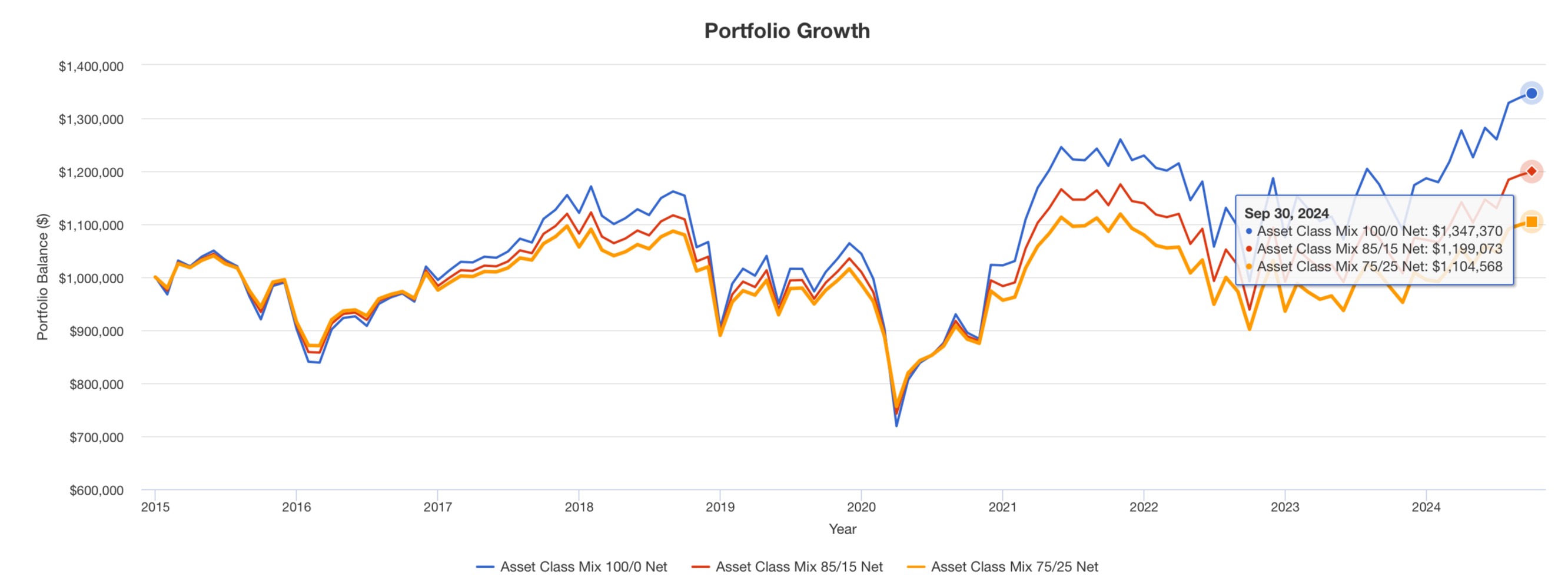

Let’s assume you retired ten years ago with a $1,000,000 investment portfolio. Your goal was to withdraw 5% ($50,000) per year, and increase it every year by the rate of inflation so your portfolio paycheck purchased the same amount of things over time, even as they got increasingly more expensive. Was this possible? Given all of the challenges of the last decade, did you have to significantly dip into principal to make this happen? If you invested the right way, not even close.

- If you were looking for maximum growth and invested in a diversified, 100% stock portfolio, net of withdrawals, you have over $1.3M today.

- If you set aside three years of spending in a short-term bond fund (15% of the portfolio) and the remaining 85% in the diversified stock portfolio, net of withdrawals, you have almost $1.2M today.

- If you wanted a larger reserve cushion and allocated five years of spending to the short-term bond fund (25% of the portfolio), with the remaining 75% in the stock portfolio, you would have $1.1M left.

In each case, you have more money than you started with in retirement despite over $500,000 of withdrawals! The portfolio balances also reflect a 1% annual advisory fee, which paid for the portfolio's management and the ongoing advice to keep our hypothetical investor disciplined and on course.

Suppose you decided to play it safe.

Maybe, you're thinking, the hypothetical retiree should have been more "conservative" with their investments and avoided the roller-coaster of ups and downs. If you went to Vanguard for retirement planning advice, they might have recommended you invest in their Lifestrategy "Conservative" Growth Fund (40% stocks/60% bonds) or their Lifestrategy "Income" Fund (20% stocks/80% bonds). Both strategies attempt to limit short-term losses, helping you to be "conservative with your money" and provide ongoing income. Unfortunately, playing it safe meant you're now playing catch-up.

In the same scenario as above, excluding an advisory fee, you only have $979,626 left over in their Conservative Growth Fund and $799,925 in their Income Fund. After a decade, you’ve gone backward, and ever-growing withdrawals now consume more and more of your principal. You may have lost less in the beginning, but you’re losing a lot more now. And your opportunity cost is massive—in the stock-oriented asset class examples above, there are hundreds of thousands of dollars more in principal left, above what you started with, for additional spending or a larger inheritance.

Don’t make investing harder than it has to be.

The investing waters are rarely smooth sailing. Everything seldom goes right, and predicting what will go wrong is impossible. While a rocky ride can be even scarier when you're no longer saving money, the bumps don't have to hurt. The last decade is an excellent example of this. Stock returns haven't been great, inflation has been challenging, and bond returns have been dismal. Yet an investor with reasonable spending goals, who owned a diversified, growth-oriented portfolio with (potentially) a few years set aside in a short-term bond fund, could survive the last decade and even thrive with more money today than ever.

Unfortunately, success is less likely to result from more cautious retirement plans and portfolios. If you want to maximize your potential future spending and give more away during and after retirement, conservative won't cut it.

____________________________________________

Diversified Stock Asset Class Portfolio = 21% DFA US High Profitability Fund (DFA US Large Company Fund prior to 6/2017 inception), 21% DFA US Large Value Fund, 28% DFA US Small Value Fund, 18% DFA Int’l Value Fund, 12% DFA Int’l Small Value Fund; rebalanced annually.

Short-Term Bond Fund = 100% DFA Five-Year Global Bond Fund

Past performance is not a guarantee of future results. Index and mutual fund performance includes reinvestment of dividends and other earnings but does not reflect the deduction of investment advisory fees or additional expenses except where noted. Indexes and mutual funds shown are for illustrative purposes only and may not be the only or any of the funds that Servo clients hold. Servo was not managing client portfolios over the entirety of the periods shown. This content is informational and should not be considered an offer, solicitation, recommendation, or endorsement of any particular security, product, or service.