With last year firmly in the rearview mirror and annual reports on their way out the door, I decided to look back on 2022 in financial markets and share some of the things that stood out to me and that we can learn from.

THE GOOD

We all know that stocks went down in 2022, and because interest rates rose at their fastest clip in modern history, bonds also sustained noticeable declines. But did you know that not all stocks went down the same amount?

The table below reports US stock returns broken down by large and small, as well as growth and value. See the difference? The 1000 largest growth stocks in the US lost -29.1% last year, and the next 2000 smaller growth stocks in the US lost -26.4%. The S&P 500 Index of large US stocks declined -18.1%. That’s the bad news.

The good news? Smaller and cheaper stocks. The DFA US Large Value Fund lost just -5.8% (outperforming large growth by over 23%), and the DFA US Small Value Fund lost -3.5% (almost 23% less than Small growth stocks). Even small cap stocks beat large stocks—the DFA US Microcap Fund outperformed the S&P 500 Index by nearly 6%.

Remember 2018 and 2020 when value unexpectedly underperformed growth by a lot? Those days are long gone. In 2021 value beat growth significantly in a positive year; last year, value stocks outperformed by losing far less.

Of course, we can’t talk about how well small cap and value stocks did in 2022 without looking at how Dimensional Funds did compared to their indexes. In a year like 2022, when value and small cap stocks outperform, DFA’s more targeted focus on these stocks should lead to better returns. What did we see?

Not just some DFA funds beat their indexes, or even most funds. All core component DFA funds beat their index.

The tables below list numerous DFA asset class funds followed by their closest comparable index with similar small cap and value characteristics (providing apples-to-apples comparisons).

DFA’s US asset class mutual funds dramatically outperformed their indexes. Some did so by an incredible amount—the DFA US Microcap Fund beat the Russell 2000 Index by 8%, and the DFA US Small Value Fund beat the Russell 2000 Value Index by 11%.

Of course, we can’t talk about how well small cap and value stocks did in 2022 without looking at how Dimensional Funds did compared to their indexes. In a year like 2022, when value and small cap stocks outperform, DFA’s more targeted focus on these stocks should lead to better returns. What did we see?

Not just some DFA funds beat their indexes, or even most funds. All core component DFA funds beat their index.

The tables below list numerous DFA asset class funds followed by their closest comparable index with similar small cap and value characteristics (providing apples-to-apples comparisons).

DFA’s US asset class mutual funds dramatically outperformed their indexes. Some did so by an incredible amount—the DFA US Microcap Fund beat the Russell 2000 Index by 8%, and the DFA US Small Value Fund beat the Russell 2000 Value Index by 11%.

To summarize—In an otherwise down year, portfolios that diversified into smaller and more value-oriented stocks were among the lone bright spots, and those that did so by owning DFA mutual funds and ETFs fared much better than those that owned basic index funds from the likes of iShares and Vanguard.

While the Vanguard US Total Stock Index Fund dropped -19.5% last year, and the Vanguard Total World Stock Index lost -18%, a small cap and value-tilted global portfolio like the DFA Equity Balanced Strategy lost only -12%.

THE BAD

As I mentioned, bonds did poorly last year as interest rates rose. For example, the yield to maturity on the DFA Five-Year Global Bond Fund entering the year was just over 1%. It closed the year yielding over 5%! Whether you see that as a 4% rise or a 400% increase, it’s significant, and increases in interest rates like this happened to all bonds, pushing prices down.

Rising interest rates punished longer-term bonds the most. The Ibbotson Long-Term Government Bond Index lost -26.1% last year, about an 8% greater decline than the S&P 500! Many investors loaded up on long-term bonds in recent years because they performed well in the bear markets of 2002 and 2008. But if they knew longer-term history, as we do, they would have seen the terrible returns of long-term bonds during the high inflation 1973-1974 bear market. And guess what? History does tend to repeat.

Other bond categories were also down, but not by nearly as much as long-term bonds. The Barclays Aggregate Bond Index lost -13% last year, its worst decline since its inception in 1976. The DFA Investment Grade Bond Fund lost a similar amount, down -12.9%. The oft-cited Ibbotson Five-Year Treasury Note Index lost -9.4%, while the shorter maturity profile of the DFA Five-Year Global Bond Fund helped it to lose “just” -6.6%.

Another mention of bad results is Treasury Inflation-Protected Securities or TIPS. These bonds have a lower interest rate (sometimes negative) compared to nominal bonds, but the Consumer Price Index (CPI) is credited to their principal periodically to provide them more sensitivity to inflation. You’d have expected TIPS to perform well in a year with the highest inflation rate in several decades. But they didn’t. The Bloomberg TIPS Index declined -11.9% last year, as their interest rates rose (and their prices fell) faster than their CPI credit added to returns. The result for TIPS in 2022 was surprisingly bad.

THE UGLY

Remember a few years ago when the latest spate of tech stocks was all the rage? Amazon, Netflix, Facebook (Meta), Apple, Microsoft, Tesla, Google (Alphabet), not to mention more up-and-coming companies like Zoom, Pelaton, Nvidia, Spotify, etc.? 2022 was a nightmare for these one-time high flyers. Instead of listing the returns of each company, let’s look at the most popular exchange-traded fund that is the poster child for these so-called disruptive companies—the Ark Innovation ETF (ARKK).

You thought the -26% loss on the US large growth index was bad in 2022, how would you feel about a -67% loss? That was the decline in the ARK ETF last year. Ouch.

As bad as this loss was, far eclipsing the worst calendar year decline for the S&P 500 in almost 100 years, it’s even worse if we pull in last year’s result as well.

I bring this period up because I spoke with several prospective clients in mid to late 2020 and early 2021 who had made a lot of money (or lost less) in the prior few years by concentrating their portfolios in these high-flying tech and “disrupter” stocks. My message? Get the hell out, pay taxes, and diversify globally and into smaller, more value-oriented stocks. Consider your windfall gains a gift from the market gods, and be glad you only have to pay a small fraction of them in long-term capital gains. But many people—including a few with portfolios well north of $10,000,000–chose to hang on for further upside or to avoid the tax consequences.

What’s happened to ARKK versus the DFA Small Cap Value Fund since 2021? $100,000 in the ARK ETF is now down -75%, a Great-Depression-like loss, while small cap value stocks have grown by over 34%! Now that’s ugly. And unfortunately, an all-too-common outcome.

Keeping 2022 In Perspective

Overall, as I said, 2022 was frustrating for investors because we ended the year with less money than when we started. But it could have been worse, and as the numbers show, that’s something to be happy about.

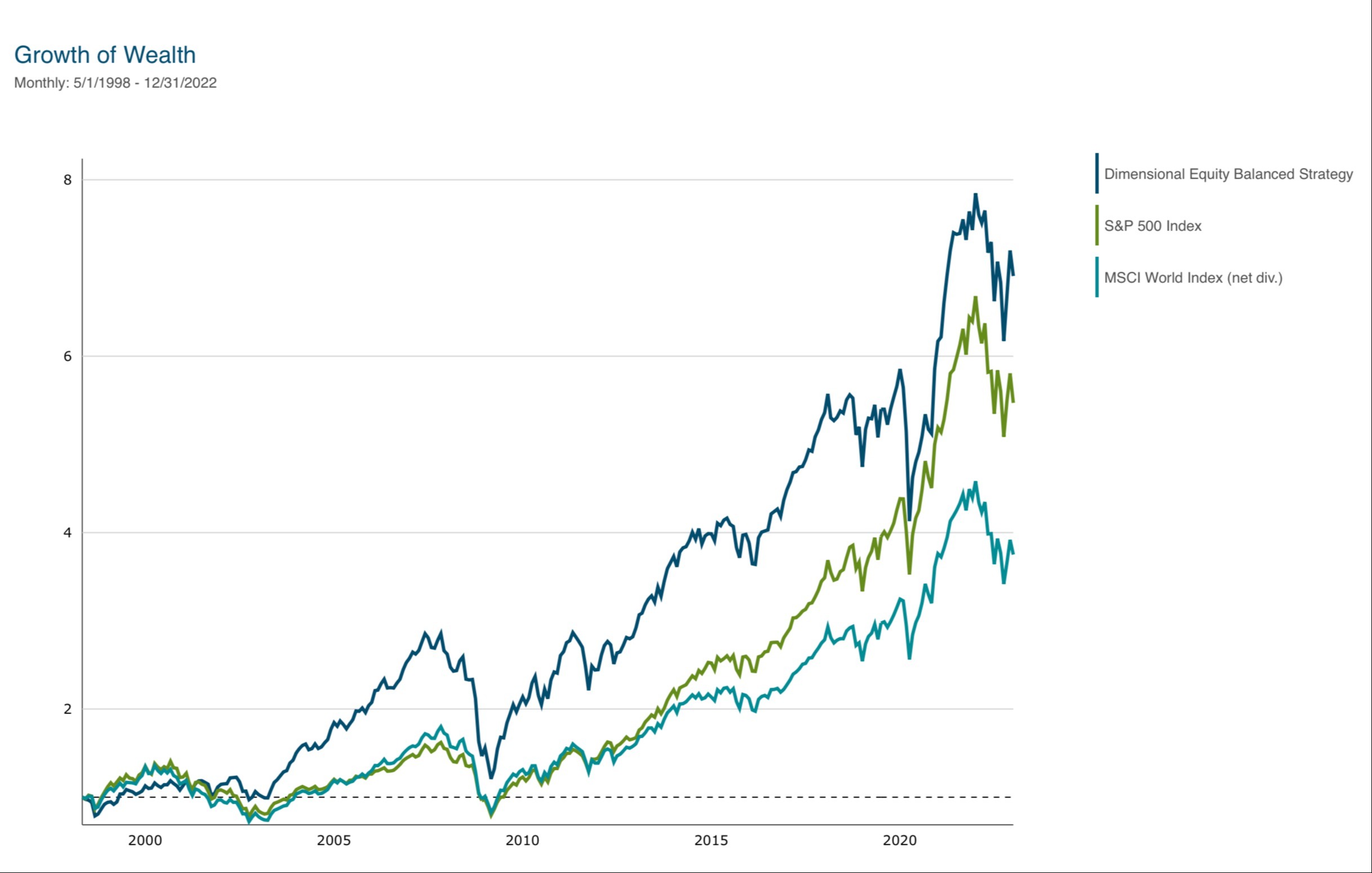

But good or bad, I want you to remember that 2022, like all others, was just a year, and long-term investors shouldn’t put much emphasis on short-term returns. Over time, individual years are a blip on an ever-increasing trend line. If you get diversified, stay diversified, and avoid reacting to yearly returns, your portfolio growth could someday look like the results shown in the chart below.

Happy 2023 to all Servo clients and Servo Blog readers! I look forward to catching up soon.

Past performance is not a guarantee of future results. Index and mutual fund performance includes reinvestment of dividends and other earnings but does not reflect the deduction of investment advisory fees or additional expenses except where noted. This content is informational and should not be considered an offer, solicitation, recommendation, or endorsement of any particular security, product, or service.